Potrebbero piacerti anche

- Calculate patient care costs and charges by severity levelDocumento3 pagineCalculate patient care costs and charges by severity levelKailash KumarNessuna valutazione finora

- Keys in Manacc Seatwork - BUDGETINGDocumento2 pagineKeys in Manacc Seatwork - BUDGETINGRoselie Barbin50% (2)

- Tata Motors SWOT TOWS CPM MatrixDocumento6 pagineTata Motors SWOT TOWS CPM MatrixPreetam Pandey33% (3)

- HWK 2Documento3 pagineHWK 2Ingrid Anaya MoralesNessuna valutazione finora

- Assigment 5.34Documento7 pagineAssigment 5.34Indahna SulfaNessuna valutazione finora

- Soal Latihan Sia 20192020 Dagang-JasaDocumento3 pagineSoal Latihan Sia 20192020 Dagang-JasaJhoni LimNessuna valutazione finora

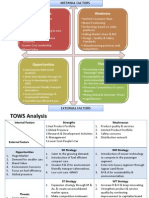

- Infosys Case AnalysisDocumento13 pagineInfosys Case AnalysisPatrick Bien De JoseNessuna valutazione finora

- SOAL 14 - 6: Prevention Appraisal Internal Failure External FailureDocumento6 pagineSOAL 14 - 6: Prevention Appraisal Internal Failure External FailureIndra YeniNessuna valutazione finora

- Tugas ObligasiDocumento15 pagineTugas Obligasiwahdah ulin nafisahNessuna valutazione finora

- CIPS Level 4 Effective NegotiationDocumento170 pagineCIPS Level 4 Effective NegotiationNga Bui100% (4)

- CHP 6 - Time Value of MoneyDocumento11 pagineCHP 6 - Time Value of MoneyShahnawaz KhanNessuna valutazione finora

- Tugas Untuk YunengDocumento9 pagineTugas Untuk YunengDinda ArdiyaniNessuna valutazione finora

- Problems Chapter 7Documento9 pagineProblems Chapter 7Trang Le0% (1)

- Latihan 7 PAK MaksiDocumento3 pagineLatihan 7 PAK MaksiDwi HandariniNessuna valutazione finora

- West Chemical Company ABC Costing AnalysisDocumento10 pagineWest Chemical Company ABC Costing Analysisrilakkuma6Nessuna valutazione finora

- PR Akmen 3Documento3 paginePR Akmen 3Achmad Faizal AzmiNessuna valutazione finora

- Week 1Documento5 pagineWeek 1Syakila AurayyanNessuna valutazione finora

- AIS Group 8 Report Chapter 17 Hand-OutDocumento8 pagineAIS Group 8 Report Chapter 17 Hand-OutPoy GuintoNessuna valutazione finora

- Jawaban Latihan KiesoDocumento4 pagineJawaban Latihan KiesoAmelia SembiringNessuna valutazione finora

- Act Part5Documento1 paginaAct Part5Moe ChannelNessuna valutazione finora

- Stephen King D D S Opened A Dental Practice On January 1 PDFDocumento1 paginaStephen King D D S Opened A Dental Practice On January 1 PDFAnbu jaromiaNessuna valutazione finora

- By - Product Problem Solving - AsifDocumento4 pagineBy - Product Problem Solving - AsifJafa AbnNessuna valutazione finora

- Intermediate: AccountingDocumento108 pagineIntermediate: AccountingDieu NguyenNessuna valutazione finora

- Corporate FinanceDocumento5 pagineCorporate FinancejahidkhanNessuna valutazione finora

- Resume SPM CompileDocumento53 pagineResume SPM Compilevita zoomNessuna valutazione finora

- Contingencies Presented Below Are Three Independent Situations PDFDocumento1 paginaContingencies Presented Below Are Three Independent Situations PDFAnbu jaromiaNessuna valutazione finora

- Audit Bab 9Documento12 pagineAudit Bab 9GusNessuna valutazione finora

- ch22 Beams12ge SMDocumento14 paginech22 Beams12ge SMJosua PranataNessuna valutazione finora

- CSA Application Analysis at PT. ABC InsuranceDocumento13 pagineCSA Application Analysis at PT. ABC InsuranceSilvi Eka PutriNessuna valutazione finora

- Kode Etik Akuntan Indonesia - SDWDocumento122 pagineKode Etik Akuntan Indonesia - SDWDiah Ayu YunitasariNessuna valutazione finora

- PV TablesDocumento7 paginePV Tablesaditi shuklaNessuna valutazione finora

- Cost Accounting Carter 14th Table of ContentsDocumento1 paginaCost Accounting Carter 14th Table of Contentsh3ll80y50% (2)

- Data Dosen PolsriDocumento29 pagineData Dosen PolsriKhusnul KhotimahNessuna valutazione finora

- CH 04Documento53 pagineCH 04SumiatiChumieNessuna valutazione finora

- Tug AsDocumento5 pagineTug Asihalalis5202100% (2)

- Accounting for Pensions and Postretirement Benefits ExpenseDocumento3 pagineAccounting for Pensions and Postretirement Benefits ExpensedwitaNessuna valutazione finora

- Jawaban Latihan Kasus KelasDocumento5 pagineJawaban Latihan Kasus KelasSHYAILA ANISHA DE LAVANDANessuna valutazione finora

- Latihans segmented reporting and absorption vs variable costingDocumento3 pagineLatihans segmented reporting and absorption vs variable costingPrisilia AudilaNessuna valutazione finora

- CH 12Documento2 pagineCH 12flrnciairn100% (1)

- SOAL DAN JAWABAN CH 10Documento29 pagineSOAL DAN JAWABAN CH 10Toni TriyuliantoNessuna valutazione finora

- Topic 5 - Tactical Decision MakingDocumento41 pagineTopic 5 - Tactical Decision MakingChoirul HudaNessuna valutazione finora

- 1995 - Dechow, Sloan, Sweeney - Jurnal - Detecting Earnings ManagementDocumento34 pagine1995 - Dechow, Sloan, Sweeney - Jurnal - Detecting Earnings ManagementTeguh Adiguna WeynandNessuna valutazione finora

- Modern Auditing: Assurance of Financial ReportingDocumento19 pagineModern Auditing: Assurance of Financial Reportingsegeri kecNessuna valutazione finora

- Implementasi Isa Di Indonesia: International Standards On Auditing (Isa)Documento22 pagineImplementasi Isa Di Indonesia: International Standards On Auditing (Isa)Muhammad Aliza ShofyNessuna valutazione finora

- Problem 14Documento3 pagineProblem 14monsinNessuna valutazione finora

- Akuntansi Manajemen Absoprtion CostingDocumento7 pagineAkuntansi Manajemen Absoprtion CostingMuhammad SyahNessuna valutazione finora

- Forum 6Documento1 paginaForum 6cecillia lissawatiNessuna valutazione finora

- Resume Swap Markets 15-1 Background: 15-1a Use of Swaps For HedgingDocumento9 pagineResume Swap Markets 15-1 Background: 15-1a Use of Swaps For HedgingAbdul Aziz FaqihNessuna valutazione finora

- Ujian Akhir Semester 2014/2015: Akuntansi InternasionalDocumento5 pagineUjian Akhir Semester 2014/2015: Akuntansi InternasionalRatnaKemalaRitongaNessuna valutazione finora

- Bab 9 AkmDocumento44 pagineBab 9 Akmcaesara geniza ghildaNessuna valutazione finora

- Pertemuan 2 An Understanding of The Client's Business and IndustryDocumento23 paginePertemuan 2 An Understanding of The Client's Business and IndustrybungaNessuna valutazione finora

- Ch22S ErrorsDocumento2 pagineCh22S ErrorsBismahMehdiNessuna valutazione finora

- AnnouncementDocumento28 pagineAnnouncementJuniarti Rosita100% (1)

- Determining Materiality and Audit Risk in Accordance with SA 320Documento8 pagineDetermining Materiality and Audit Risk in Accordance with SA 320Pankaj RungtaNessuna valutazione finora

- CH 23Documento81 pagineCH 23rara mirantiNessuna valutazione finora

- P12 2aDocumento4 pagineP12 2aMaria AngeliqueNessuna valutazione finora

- 2017 Annual Report - PT Graha Layar Prima TBK PDFDocumento220 pagine2017 Annual Report - PT Graha Layar Prima TBK PDFKevin D'ShōnenNessuna valutazione finora

- Final Exam December 2020Documento5 pagineFinal Exam December 2020Ikhwan RizkyNessuna valutazione finora

- Kode QDocumento11 pagineKode QatikaNessuna valutazione finora

- Evaluating Project Economics and Capital RationingDocumento46 pagineEvaluating Project Economics and Capital RationingNguyen Thanh Tung (K15 HL)Nessuna valutazione finora

- IFRS 15 Session4 Handout 1Documento2 pagineIFRS 15 Session4 Handout 1Simon YossefNessuna valutazione finora

- CH 14Documento6 pagineCH 14Aminul Haque RusselNessuna valutazione finora

- Nghiên C U KH-C5Documento29 pagineNghiên C U KH-C5Nga BuiNessuna valutazione finora

- Tham Dinh Mega CentreDocumento49 pagineTham Dinh Mega CentreNga BuiNessuna valutazione finora

- Sentence Correct AnswerDocumento5 pagineSentence Correct AnswerNga BuiNessuna valutazione finora

- Nghiên C U KH-C6Documento31 pagineNghiên C U KH-C6Nga BuiNessuna valutazione finora

- EC - Ch03 Key WordsDocumento5 pagineEC - Ch03 Key WordsNga BuiNessuna valutazione finora

- 884 Ch11ARQDocumento5 pagine884 Ch11ARQNga BuiNessuna valutazione finora

- Questions: Answers Answer To Q 14.1 Parts (A) and (B) Are Provided in The Excel File Titled "Q 14.1 Excel Solutions - XLS"Documento1 paginaQuestions: Answers Answer To Q 14.1 Parts (A) and (B) Are Provided in The Excel File Titled "Q 14.1 Excel Solutions - XLS"Nga BuiNessuna valutazione finora

- 900 Ch16ARQDocumento5 pagine900 Ch16ARQNga BuiNessuna valutazione finora

- 898 Ch15ARQDocumento2 pagine898 Ch15ARQNga BuiNessuna valutazione finora

- 856 Ch01ARQDocumento6 pagine856 Ch01ARQtania_afaz2800Nessuna valutazione finora

- Optimize hotel design and financing with LP modelDocumento7 pagineOptimize hotel design and financing with LP modelNga BuiNessuna valutazione finora

- Key EC Marketing Terms GuideDocumento10 pagineKey EC Marketing Terms GuideNga BuiNessuna valutazione finora

- Questions: Answers Answer To Q 13.1Documento2 pagineQuestions: Answers Answer To Q 13.1Nga BuiNessuna valutazione finora

- 883 Ch10ARQDocumento4 pagine883 Ch10ARQNga BuiNessuna valutazione finora

- 856 Ch01ARQDocumento6 pagine856 Ch01ARQtania_afaz2800Nessuna valutazione finora

- EC-Ch04 Key WordsDocumento5 pagineEC-Ch04 Key WordsNga BuiNessuna valutazione finora

- Final Exam Question No. 2Documento8 pagineFinal Exam Question No. 2Nga BuiNessuna valutazione finora

- Chapter 1 Memo From Esther NieldsDocumento3 pagineChapter 1 Memo From Esther NieldsNga BuiNessuna valutazione finora

- Final Exam Question No. 1Documento8 pagineFinal Exam Question No. 1Nga BuiNessuna valutazione finora

- EC - Ch02 Key WordsDocumento17 pagineEC - Ch02 Key WordsNga BuiNessuna valutazione finora

- Can Can Thanh ToanDocumento8 pagineCan Can Thanh ToanNga BuiNessuna valutazione finora

- SOA Exam MFE and CAS Exam 3 FE Solution to Derivatives MarketsDocumento25 pagineSOA Exam MFE and CAS Exam 3 FE Solution to Derivatives MarketsNga BuiNessuna valutazione finora

- MATH Summer2013 T1 SolutionsDocumento1 paginaMATH Summer2013 T1 SolutionsNga BuiNessuna valutazione finora

- Introduction To DerivativesDocumento6 pagineIntroduction To Derivativesgiangcoitp89Nessuna valutazione finora

- Chi-Square AloneDocumento1 paginaChi-Square AloneNga BuiNessuna valutazione finora

- Stat11t Chapter6Documento115 pagineStat11t Chapter6Nga BuiNessuna valutazione finora

- Informal Settlements Report Aug 2022Documento67 pagineInformal Settlements Report Aug 2022Micaela Alcalde100% (1)

- Literature ReviewDocumento28 pagineLiterature ReviewIshaan Banerjee50% (2)

- Impact of Covid 19 on E-marketing in Pharmaceutical IndustryDocumento4 pagineImpact of Covid 19 on E-marketing in Pharmaceutical Industryamit singhNessuna valutazione finora

- Marketing Plan Industry AnalysisDocumento14 pagineMarketing Plan Industry Analysisbakhtawar soniaNessuna valutazione finora

- Feasibility Study For Coffee and Flower ShopDocumento7 pagineFeasibility Study For Coffee and Flower ShopdsdsassaNessuna valutazione finora

- Marketing Midterm Quiz: Question Number 1Documento11 pagineMarketing Midterm Quiz: Question Number 1zlstevenNessuna valutazione finora

- Dyer2013 PDFDocumento574 pagineDyer2013 PDFMiguel Alejandro Diaz CastilloNessuna valutazione finora

- Airport Slots, Secondary Trading, and Congestion Pricing at An Airport With A Dominant Network AirlineDocumento14 pagineAirport Slots, Secondary Trading, and Congestion Pricing at An Airport With A Dominant Network AirlineSusheel Kumar SiramNessuna valutazione finora

- Construction Contract Revenue RecognitionDocumento2 pagineConstruction Contract Revenue RecognitionDevine Grace A. MaghinayNessuna valutazione finora

- Advertising Sales Proposal for HOME CASH OPTIONSDocumento4 pagineAdvertising Sales Proposal for HOME CASH OPTIONSAndrés AyalaNessuna valutazione finora

- 1 Markerting MixDocumento16 pagine1 Markerting MixAna Kristelle Grace SyNessuna valutazione finora

- Financial Instrument: What Are Financial Instruments?Documento9 pagineFinancial Instrument: What Are Financial Instruments?Ammara NawazNessuna valutazione finora

- Green MarketingDocumento2 pagineGreen Marketingzakirno19248Nessuna valutazione finora

- Market Identification and AnalysisDocumento29 pagineMarket Identification and AnalysisJerNessuna valutazione finora

- Assignment 1 (BBA & BBIS) SUB: OM Inventory Management: EOQ 200 Units & ROL 40 L, L Lead TimeDocumento3 pagineAssignment 1 (BBA & BBIS) SUB: OM Inventory Management: EOQ 200 Units & ROL 40 L, L Lead Timesajal koiralaNessuna valutazione finora

- FS of Wound Healing OilDocumento20 pagineFS of Wound Healing OilKhate Nicole NoNessuna valutazione finora

- Source of Regular Input VATDocumento1 paginaSource of Regular Input VATMarie Tes LocsinNessuna valutazione finora

- Q2: What Conflicts or Barriers Internal To Barilla DoesDocumento7 pagineQ2: What Conflicts or Barriers Internal To Barilla DoesNiharika JainNessuna valutazione finora

- Bracknell Cash Flow QuestionDocumento3 pagineBracknell Cash Flow Questionsanjay blakeNessuna valutazione finora

- OWNER OF GOODS IN TRANSITDocumento3 pagineOWNER OF GOODS IN TRANSITCzar RabayaNessuna valutazione finora

- Direct and Indirect SellingDocumento6 pagineDirect and Indirect SellingMelvineJSTempleNessuna valutazione finora

- Issues in Economics Today 8th Edition Guell Test BankDocumento25 pagineIssues in Economics Today 8th Edition Guell Test BankAndreFitzgeraldofrd100% (53)

- InvoiceDocumento1 paginaInvoicemanojkmorwal07Nessuna valutazione finora

- Relevance of The 4e Marketing Model To TheDocumento12 pagineRelevance of The 4e Marketing Model To Theankit palNessuna valutazione finora

- DropboxDocumento3 pagineDropboxmeriemNessuna valutazione finora

- Airborne Express Discussion QuestionsDocumento5 pagineAirborne Express Discussion QuestionsPeter LiedmanNessuna valutazione finora

- Short Quiz 8 Set B With AnswerDocumento3 pagineShort Quiz 8 Set B With AnswerJean Pierre IsipNessuna valutazione finora

- Market Research and AnalysisDocumento22 pagineMarket Research and AnalysisJimmy DuldulaoNessuna valutazione finora

- Terminal Value - Perpetuity Growth & Exit Multiple MethodDocumento11 pagineTerminal Value - Perpetuity Growth & Exit Multiple MethodFahmi HaritsNessuna valutazione finora