Potrebbero piacerti anche

- 7 NEW Charge Back Letter No 2Documento1 pagina7 NEW Charge Back Letter No 2party2494% (18)

- Cambridge International As and A Level Business Studies Revision GuideDocumento217 pagineCambridge International As and A Level Business Studies Revision GuideAlyan Hanif92% (12)

- Mystmt - 2022 11 09Documento5 pagineMystmt - 2022 11 09sylvia100% (2)

- Report of BSNLDocumento52 pagineReport of BSNLmishra_vivek1989Nessuna valutazione finora

- Performance Appraisal in BSNLDocumento61 paginePerformance Appraisal in BSNLVaishu Gs86% (7)

- BSNL Financial Overview of Telecom Sector in IndiaDocumento112 pagineBSNL Financial Overview of Telecom Sector in Indianaveenchaurasia50% (2)

- Vishnubsnl 110507124721 Phpapp01Documento113 pagineVishnubsnl 110507124721 Phpapp01smblacksmith11Nessuna valutazione finora

- Project On Performance Appraisal of Emplyees in BSNL TelecommunicationDocumento39 pagineProject On Performance Appraisal of Emplyees in BSNL TelecommunicationFiroz shaikhNessuna valutazione finora

- 3cet ReportDocumento27 pagine3cet Reportsaxenasai0% (1)

- Project Report On Performance Appraisal of BSNLDocumento71 pagineProject Report On Performance Appraisal of BSNLRashmi Ranjan Panigrahi100% (1)

- Bharat Sanchar Nigam LimitedDocumento17 pagineBharat Sanchar Nigam LimitedŠtÿłổ ÁtŤïtüdẽ Swati SharmaNessuna valutazione finora

- Financial Statement Analysis of BSNLDocumento58 pagineFinancial Statement Analysis of BSNLmss_singh_sikarwar75% (20)

- Comparative Statment Analysis of BSNLDocumento60 pagineComparative Statment Analysis of BSNLPreet Kaur80% (5)

- 360 Degree Performance Appraisal: A Project Report OnDocumento18 pagine360 Degree Performance Appraisal: A Project Report OnpriyataNessuna valutazione finora

- Performance Appraisal": Sherwood College of Professional ManagementDocumento77 paginePerformance Appraisal": Sherwood College of Professional ManagementAmritaSinghNessuna valutazione finora

- INTRODUCTIONDocumento19 pagineINTRODUCTIONNishant NamdeoNessuna valutazione finora

- BSNL Financial Overview of Telecom Sector in IndiaDocumento112 pagineBSNL Financial Overview of Telecom Sector in Indiavineet tiwariNessuna valutazione finora

- Project Report On BSNL VS VodafoneDocumento59 pagineProject Report On BSNL VS Vodafoneihateushashank0% (2)

- Bharat Sanchar Nigam LimitedDocumento11 pagineBharat Sanchar Nigam LimitedJay RathodNessuna valutazione finora

- BSNL Project ManagementDocumento41 pagineBSNL Project ManagementParas NainNessuna valutazione finora

- Project Report BSNL VodafoneDocumento59 pagineProject Report BSNL VodafoneskraajputNessuna valutazione finora

- Bharat Sanchar Nigam LimitedDocumento6 pagineBharat Sanchar Nigam LimitedpriyankavlNessuna valutazione finora

- Project Report On Performance Appraisal of BSNLDocumento20 pagineProject Report On Performance Appraisal of BSNLVasudha KulkarniNessuna valutazione finora

- BSNL Case Study SummaryDocumento6 pagineBSNL Case Study Summarysarat_maNessuna valutazione finora

- 10 - Chapter 2 PDFDocumento38 pagine10 - Chapter 2 PDFLoolik SoliNessuna valutazione finora

- Labh PDFDocumento5 pagineLabh PDFNon ChalantNessuna valutazione finora

- BSNL SynopsisDocumento72 pagineBSNL SynopsisAtul MauryaNessuna valutazione finora

- Bharat Sanchar Nigam LimitedDocumento31 pagineBharat Sanchar Nigam LimitedTimothy TownsendNessuna valutazione finora

- Yashikkaaa 100000000000000000Documento85 pagineYashikkaaa 100000000000000000Yashika SainiNessuna valutazione finora

- Performancemanagementsystem At: ScribdDocumento9 paginePerformancemanagementsystem At: ScribdSunita RaniNessuna valutazione finora

- Introductio N About BSNLDocumento27 pagineIntroductio N About BSNLcollin_77777Nessuna valutazione finora

- ADocumento78 pagineATushar PandeyNessuna valutazione finora

- Calculation of Working Capital Auto Saved)Documento13 pagineCalculation of Working Capital Auto Saved)Soni AgrawalNessuna valutazione finora

- Himani Naithani.... RPORT (Repaired)Documento67 pagineHimani Naithani.... RPORT (Repaired)Kshitij RastogiNessuna valutazione finora

- Bharat Sanchar Nigam LimitedDocumento5 pagineBharat Sanchar Nigam LimitedApat AnghaaNessuna valutazione finora

- BSNL Company ProfileDocumento3 pagineBSNL Company ProfilesrikutyNessuna valutazione finora

- Summer Internship at BSNL, TrivandrumDocumento17 pagineSummer Internship at BSNL, TrivandrumAnakha Balachandran100% (1)

- Project Report On Performance Appraisal at BSNLDocumento46 pagineProject Report On Performance Appraisal at BSNLSuksham Sood100% (2)

- Company ProfileDocumento13 pagineCompany ProfileratishyamgaurNessuna valutazione finora

- Comparative Statement Analysis of BSNLDocumento64 pagineComparative Statement Analysis of BSNLmss_singh_sikarwar82% (11)

- BSNL WikiDocumento6 pagineBSNL WikiMumin KhanNessuna valutazione finora

- Vision, Mission & Objectives of BSNL VISION: To Become TheDocumento3 pagineVision, Mission & Objectives of BSNL VISION: To Become Thedanu75Nessuna valutazione finora

- SynopsisDocumento2 pagineSynopsisVinni NavlaniNessuna valutazione finora

- Project BSNLDocumento14 pagineProject BSNLSachin RajNessuna valutazione finora

- Research Report by Shailesh KR Singh (Sc-2) Ss 2009-11Documento61 pagineResearch Report by Shailesh KR Singh (Sc-2) Ss 2009-119899866563Nessuna valutazione finora

- Contents of The Project: History About BSNLDocumento35 pagineContents of The Project: History About BSNLBharat SinghNessuna valutazione finora

- BC ReportDocumento8 pagineBC ReportSreedhar SnNessuna valutazione finora

- Bba 3rd Sem Project ReportDocumento64 pagineBba 3rd Sem Project Reportsinghraj100100% (5)

- Project - Revenue Assuarance in BSNL Submitted By-MohitDocumento73 pagineProject - Revenue Assuarance in BSNL Submitted By-Mohitmohit1990gupta3749Nessuna valutazione finora

- A Presentation On Organization Study: Bharat Sanchar Nigam Limited (BSNL), SirsaDocumento17 pagineA Presentation On Organization Study: Bharat Sanchar Nigam Limited (BSNL), SirsaKapil SethiNessuna valutazione finora

- BSNLDocumento17 pagineBSNLNagaveni Gl100% (4)

- BSNL Marketing Mix and StrategiesDocumento6 pagineBSNL Marketing Mix and Strategiesvarun joshiNessuna valutazione finora

- Outlines: Services Offered by BSNL Types of Exchanges Layout of Exchanges RefrencesDocumento22 pagineOutlines: Services Offered by BSNL Types of Exchanges Layout of Exchanges RefrencesShivam SinghNessuna valutazione finora

- Comparison of BSNL Services With Its CompetitorsDocumento98 pagineComparison of BSNL Services With Its Competitorslokesh_045Nessuna valutazione finora

- About Us: Gross Investment in Fixed AssetsDocumento3 pagineAbout Us: Gross Investment in Fixed AssetsSainu SanuNessuna valutazione finora

- Papers on the field: Telecommunication Economic, Business, Regulation & PolicyDa EverandPapers on the field: Telecommunication Economic, Business, Regulation & PolicyNessuna valutazione finora

- Telecommunications Reseller Revenues World Summary: Market Values & Financials by CountryDa EverandTelecommunications Reseller Revenues World Summary: Market Values & Financials by CountryNessuna valutazione finora

- LTE Self-Organising Networks (SON): Network Management Automation for Operational EfficiencyDa EverandLTE Self-Organising Networks (SON): Network Management Automation for Operational EfficiencySeppo HämäläinenNessuna valutazione finora

- Promoting Information and Communication Technology in ADB OperationsDa EverandPromoting Information and Communication Technology in ADB OperationsNessuna valutazione finora

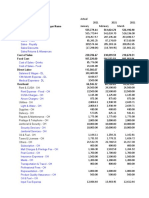

- Cable & Program Distribution Lines World Summary: Market Values & Financials by CountryDa EverandCable & Program Distribution Lines World Summary: Market Values & Financials by CountryNessuna valutazione finora

- Satellite Telecommunications Lines World Summary: Market Values & Financials by CountryDa EverandSatellite Telecommunications Lines World Summary: Market Values & Financials by CountryNessuna valutazione finora

- Emerging FinTech: Understanding and Maximizing Their BenefitsDa EverandEmerging FinTech: Understanding and Maximizing Their BenefitsNessuna valutazione finora

- JustCo Plans To Dominate AsiaDocumento10 pagineJustCo Plans To Dominate AsiaYC TeoNessuna valutazione finora

- Template Expense Report - With JobsDocumento6 pagineTemplate Expense Report - With JobsLiz AnNessuna valutazione finora

- HDFCDocumento4 pagineHDFCTrue ChallengerNessuna valutazione finora

- Terms ReferenceDocumento4 pagineTerms ReferenceEmmanuel Mends FynnNessuna valutazione finora

- The Strategy For Chinese Brands: Part 1 - The Perception ChallengeDocumento8 pagineThe Strategy For Chinese Brands: Part 1 - The Perception ChallengeAanal PrajapatiNessuna valutazione finora

- Chapter FiveDocumento14 pagineChapter Fivemubarek oumerNessuna valutazione finora

- Faculty of Commerce and Management Kumaun University, NainitalDocumento8 pagineFaculty of Commerce and Management Kumaun University, Nainitalsaddam_1991Nessuna valutazione finora

- Introduction To DerivativesDocumento34 pagineIntroduction To Derivativessalil1285100% (2)

- Income From Business and Profession HandoutDocumento29 pagineIncome From Business and Profession HandoutAnantha Krishna BhatNessuna valutazione finora

- Brochure Management Manual - EN PDFDocumento45 pagineBrochure Management Manual - EN PDFbudiaeroNessuna valutazione finora

- MS-1stPB 10.22Documento12 pagineMS-1stPB 10.22Harold Dan Acebedo0% (1)

- Strat SheetDocumento1 paginaStrat Sheetcourier12Nessuna valutazione finora

- Case Study Project Income Statement BudgetingDocumento186 pagineCase Study Project Income Statement BudgetingKate ChuaNessuna valutazione finora

- LKP Spade - Torrent Pharma - 7octDocumento3 pagineLKP Spade - Torrent Pharma - 7octpremNessuna valutazione finora

- Best Practices For Work-At-Home (WAH) Operations: Webinar SeriesDocumento24 pagineBest Practices For Work-At-Home (WAH) Operations: Webinar SeriesHsekum AtpakNessuna valutazione finora

- The IB Business of EquitiesDocumento79 pagineThe IB Business of EquitiesNgọc Phan Thị BíchNessuna valutazione finora

- 0106XXXXXX8428-01-04-21 - 31-03-2022Documento27 pagine0106XXXXXX8428-01-04-21 - 31-03-2022SabyasachiBanerjeeNessuna valutazione finora

- The Social Function of BusinessDocumento10 pagineThe Social Function of BusinessJupiter WhitesideNessuna valutazione finora

- Screen (HTS) - WINPro 200 DocumentationDocumento83 pagineScreen (HTS) - WINPro 200 DocumentationBob ClarksonNessuna valutazione finora

- A Methodology For Performance Measurement and Peer Comparison in The Public Transportation Industry (2010)Documento17 pagineA Methodology For Performance Measurement and Peer Comparison in The Public Transportation Industry (2010)Alfred LochanNessuna valutazione finora

- Groz ToolsDocumento71 pagineGroz ToolsAnil BatraNessuna valutazione finora

- List of Ledgers and It's Under Group in TallyDocumento5 pagineList of Ledgers and It's Under Group in Tallyrachel KujurNessuna valutazione finora

- Marginal CostingDocumento30 pagineMarginal Costinganon_3722476140% (1)

- MGT 210Documento19 pagineMGT 210FAYAZ AHMEDNessuna valutazione finora

- Erika Xim Paola Santos BSBA (Marketing) - III BA 170 - 4Documento4 pagineErika Xim Paola Santos BSBA (Marketing) - III BA 170 - 4XimPao SaintNessuna valutazione finora

- Top Qualities of A Successful BusinessmanDocumento40 pagineTop Qualities of A Successful Businessmansufyanbutt007Nessuna valutazione finora

- Case Study (ENT530)Documento12 pagineCase Study (ENT530)Nur Diyana50% (2)