Potrebbero piacerti anche

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- Schedule of Fees 2009Documento2 pagineSchedule of Fees 2009Veronica BayaniNessuna valutazione finora

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- Washington AccordDocumento17 pagineWashington AccordVeronica BayaniNessuna valutazione finora

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- 10 AUG 2019 CBTM Be So Good They Cant Ignore YouDocumento2 pagine10 AUG 2019 CBTM Be So Good They Cant Ignore YouVeronica BayaniNessuna valutazione finora

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- Instrumentation and Control Servicing NC IIDocumento88 pagineInstrumentation and Control Servicing NC IIVeronica BayaniNessuna valutazione finora

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- 2013-2014 UPLB Academic Calendar PDFDocumento2 pagine2013-2014 UPLB Academic Calendar PDFVeronica Bayani100% (1)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- A Critical Analysis of A FilmDocumento4 pagineA Critical Analysis of A FilmVeronica BayaniNessuna valutazione finora

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (400)

- SM Trash To CashDocumento2 pagineSM Trash To CashVeronica BayaniNessuna valutazione finora

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- Investment Guide For FilipinosDocumento2 pagineInvestment Guide For FilipinosGian Carlo BeroNessuna valutazione finora

- Jaeger Products, Inc: Superior Performance by DesignDocumento18 pagineJaeger Products, Inc: Superior Performance by Designpulse550100% (1)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- EnglishDocumento6 pagineEnglishDiep NgocNessuna valutazione finora

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- Purchasing Presentation 11iDocumento59 paginePurchasing Presentation 11iadityakhadkeNessuna valutazione finora

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- Log-2023 11 18 04 58Documento5 pagineLog-2023 11 18 04 58maikapaghubasanNessuna valutazione finora

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- Introduction To Physical SecurityDocumento11 pagineIntroduction To Physical SecuritytanweerNessuna valutazione finora

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (74)

- Study Informatics at School - WorldwideDocumento67 pagineStudy Informatics at School - WorldwideMauricio Oyanader ArntzNessuna valutazione finora

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (344)

- Hill ClimbingDocumento12 pagineHill ClimbingVishesh YadavNessuna valutazione finora

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- Lesson 4.2 - Greatest Common FactorDocumento23 pagineLesson 4.2 - Greatest Common FactorehystadNessuna valutazione finora

- Kurukshetra University, Kurukshetra: Roll N0.-cum-Admit CardDocumento2 pagineKurukshetra University, Kurukshetra: Roll N0.-cum-Admit CardANKIT ranaNessuna valutazione finora

- SM-G970F Tshoo 7Documento64 pagineSM-G970F Tshoo 7Rosbel Hernandez100% (2)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- Partial DerivativesDocumento15 paginePartial DerivativesAien Nurul AinNessuna valutazione finora

- Global Sourcing OptionsDocumento25 pagineGlobal Sourcing OptionsKazi ZamanNessuna valutazione finora

- Exam Student HSC 90 Percen Le Student Download Old Data Candidate ListDocumento1 paginaExam Student HSC 90 Percen Le Student Download Old Data Candidate ListKrishnaVyasNessuna valutazione finora

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- Projet Geological Imaging Idriss MontheDocumento30 pagineProjet Geological Imaging Idriss MontheIdriss MonthéNessuna valutazione finora

- Vmware Certification Tracks DiagramDocumento3 pagineVmware Certification Tracks Diagrameppoxro0% (1)

- 020 - Revised Regular Result - Siddharth Kumar - 41624002018 - December 2019Documento2 pagine020 - Revised Regular Result - Siddharth Kumar - 41624002018 - December 2019Nilesh SinghNessuna valutazione finora

- Section 1Documento10 pagineSection 1Alfin GithuNessuna valutazione finora

- Fireclass Overview Presentation PDFDocumento34 pagineFireclass Overview Presentation PDFRamon Mendoza PantojaNessuna valutazione finora

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (121)

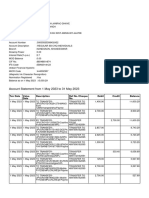

- Account Statement From 1 May 2023 To 31 May 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocumento10 pagineAccount Statement From 1 May 2023 To 31 May 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit Balanceavinashdeshmukh7027Nessuna valutazione finora

- Jeporday GameDocumento27 pagineJeporday Gameapi-540635052Nessuna valutazione finora

- Characterstics of Project ManagementDocumento28 pagineCharacterstics of Project ManagementAnkit Berasiya100% (1)

- 6 Matrix Chain M UltiplicationDocumento19 pagine6 Matrix Chain M UltiplicationArslan Ahmed DanishNessuna valutazione finora

- LSE400S Tutorial 1Documento1 paginaLSE400S Tutorial 1Willy K. Ng'etichNessuna valutazione finora

- Trick-1: Create Shortcut For Removing PendriveDocumento230 pagineTrick-1: Create Shortcut For Removing Pendriveprince4458Nessuna valutazione finora

- Introduction To Computing To FASADocumento118 pagineIntroduction To Computing To FASAabdoulayNessuna valutazione finora

- Automine For Trucks Brochure EnglishDocumento4 pagineAutomine For Trucks Brochure EnglishJH Miguel AngelNessuna valutazione finora

- Program 5th NSysS v5Documento4 pagineProgram 5th NSysS v5LabibaNessuna valutazione finora

- Rtflex System PDFDocumento67 pagineRtflex System PDFPintu KumarNessuna valutazione finora

- ArcadisOrbic SystemSoftwareInstallationDocumento56 pagineArcadisOrbic SystemSoftwareInstallationEduardo Saul MendozaNessuna valutazione finora

- Sap BW Data Modeling GuideDocumento18 pagineSap BW Data Modeling GuideSapbi SriNessuna valutazione finora

- S922X Public Datasheet V0.2 PDFDocumento1.111 pagineS922X Public Datasheet V0.2 PDFady_gligor7987Nessuna valutazione finora

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)