Potrebbero piacerti anche

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- Notice To The MarketDocumento1 paginaNotice To The MarketJBS RINessuna valutazione finora

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- Minutes of The Board of Directors' Meeting Held On May 08, 2017Documento2 pagineMinutes of The Board of Directors' Meeting Held On May 08, 2017JBS RINessuna valutazione finora

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- Release and FS 1Q17Documento53 pagineRelease and FS 1Q17JBS RINessuna valutazione finora

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (400)

- 1Q17 Earnings PresentationDocumento15 pagine1Q17 Earnings PresentationJBS RINessuna valutazione finora

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- 1Q17 Financial StatementsDocumento31 pagine1Q17 Financial StatementsJBS RINessuna valutazione finora

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- 1Q17 Conference Call TranscriptDocumento13 pagine1Q17 Conference Call TranscriptJBS RINessuna valutazione finora

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- Notice To The MarketDocumento1 paginaNotice To The MarketJBS RINessuna valutazione finora

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- Notice To The MarketDocumento1 paginaNotice To The MarketJBS RINessuna valutazione finora

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- JBS S.A. Releases Its 2016 Annual and Sustainability ReportDocumento1 paginaJBS S.A. Releases Its 2016 Annual and Sustainability ReportJBS RINessuna valutazione finora

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- JBS S.A. Announces The Conclusion of Plumrose AcquisitionDocumento1 paginaJBS S.A. Announces The Conclusion of Plumrose AcquisitionJBS RINessuna valutazione finora

- Minutes of The Board of Directors' Meeting Held On May 05, 2017Documento2 pagineMinutes of The Board of Directors' Meeting Held On May 05, 2017JBS RINessuna valutazione finora

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- JBS - Annual and Sustainability Report 2016Documento144 pagineJBS - Annual and Sustainability Report 2016JBS RINessuna valutazione finora

- Minutes of The Fiscal Council's Meeting Held On May 04, 2017Documento2 pagineMinutes of The Fiscal Council's Meeting Held On May 04, 2017JBS RINessuna valutazione finora

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- JBS - ARCA - 2017 04 06 - Aprovao Reapresentao DFs 2015 e 2016 (JUCESP) EngDocumento5 pagineJBS - ARCA - 2017 04 06 - Aprovao Reapresentao DFs 2015 e 2016 (JUCESP) EngJBS RINessuna valutazione finora

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (73)

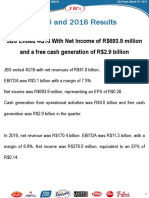

- 4Q16 Conference Call TranscriptDocumento16 pagine4Q16 Conference Call TranscriptJBS RINessuna valutazione finora

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (344)

- Minutes of The Fiscal Council's Meeting Held On April 05, 2017Documento5 pagineMinutes of The Fiscal Council's Meeting Held On April 05, 2017JBS RINessuna valutazione finora

- MGMT Report FS 2015 (Reap 2017)Documento95 pagineMGMT Report FS 2015 (Reap 2017)JBS RINessuna valutazione finora

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- REMOTE VOTING FORM OF OESM To Be Held On April 28, 2017Documento5 pagineREMOTE VOTING FORM OF OESM To Be Held On April 28, 2017JBS RINessuna valutazione finora

- 4Q16 and 2016 Earnings PresentationDocumento21 pagine4Q16 and 2016 Earnings PresentationJBS RINessuna valutazione finora

- MGMT Report FS 2016 (Reap 2017)Documento97 pagineMGMT Report FS 2016 (Reap 2017)JBS RINessuna valutazione finora

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- Minutes of The Board of Directors' Meeting Held On March 13, 2017Documento4 pagineMinutes of The Board of Directors' Meeting Held On March 13, 2017JBS RINessuna valutazione finora

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- JBS - ARCF - 2017 03 10 - Aprovao DFs 4T2016 (Livro) MZT EngDocumento4 pagineJBS - ARCF - 2017 03 10 - Aprovao DFs 4T2016 (Livro) MZT EngJBS RINessuna valutazione finora

- JBS Institutional Presentation Including 4Q16 and 2016 ResultsDocumento24 pagineJBS Institutional Presentation Including 4Q16 and 2016 ResultsJBS RINessuna valutazione finora

- Notice To The Market - Federal Police OperationDocumento1 paginaNotice To The Market - Federal Police OperationJBS RINessuna valutazione finora

- MgmtReport FSDocumento96 pagineMgmtReport FSJBS RINessuna valutazione finora

- Minutes of The Board of Directors' Meeting Held On February 23, 2017Documento20 pagineMinutes of The Board of Directors' Meeting Held On February 23, 2017JBS RINessuna valutazione finora

- 4Q16 and 2016 Earnings ReleaseDocumento31 pagine4Q16 and 2016 Earnings ReleaseJBS RI100% (1)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (121)

- MgmtReport FSDocumento96 pagineMgmtReport FSJBS RINessuna valutazione finora

- MATERIAL FACT - JBS Announces The Acquisition of Plumrose USADocumento2 pagineMATERIAL FACT - JBS Announces The Acquisition of Plumrose USAJBS RINessuna valutazione finora

- UntitledDocumento4 pagineUntitledJBS RINessuna valutazione finora

- Case Note Butler Machine 201718Documento4 pagineCase Note Butler Machine 201718Maggie SalisburyNessuna valutazione finora

- Palma vs. Fortich PDFDocumento3 paginePalma vs. Fortich PDFKristine VillanuevaNessuna valutazione finora

- Chapter 4 TeethDocumento17 pagineChapter 4 TeethAbegail RuizNessuna valutazione finora

- Test Bank For Biology 7th Edition Neil A CampbellDocumento36 pagineTest Bank For Biology 7th Edition Neil A Campbellpoupetonlerneanoiv0ob100% (31)

- Group5 (Legit) - Brain Base-Curriculum-InnovationsDocumento6 pagineGroup5 (Legit) - Brain Base-Curriculum-InnovationsTiffany InocenteNessuna valutazione finora

- The Apollo Parachute Landing SystemDocumento28 pagineThe Apollo Parachute Landing SystemBob Andrepont100% (2)

- Barber ResumeDocumento6 pagineBarber Resumefrebulnfg100% (1)

- SPM Bahasa Inggeris PAPER 1 - NOTES 2020Documento11 pagineSPM Bahasa Inggeris PAPER 1 - NOTES 2020MaryNessuna valutazione finora

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- RPMDocumento35 pagineRPMnisfyNessuna valutazione finora

- Mettler Ics429 User ManualDocumento60 pagineMettler Ics429 User ManualJhonny Velasquez PerezNessuna valutazione finora

- Order: Philadelphia Municipal CourtDocumento1 paginaOrder: Philadelphia Municipal CourtRyan BriggsNessuna valutazione finora

- 4-String Cigar Box Guitar Chord Book (Brent Robitaille) (Z-Library)Documento172 pagine4-String Cigar Box Guitar Chord Book (Brent Robitaille) (Z-Library)gregory berlemontNessuna valutazione finora

- Gaffney S Business ContactsDocumento6 pagineGaffney S Business ContactsSara Mitchell Mitchell100% (1)

- Becg Unit-1Documento8 pagineBecg Unit-1Bhaskaran Balamurali0% (1)

- A Study of Cognitive Human Factors in Mascot DesignDocumento16 pagineA Study of Cognitive Human Factors in Mascot DesignAhmadNessuna valutazione finora

- First Aid EssentialsDocumento5 pagineFirst Aid EssentialsQueen ValleNessuna valutazione finora

- Gucci MurderDocumento13 pagineGucci MurderPatsy StoneNessuna valutazione finora

- SSD Term 3Documento52 pagineSSD Term 3anne_barltropNessuna valutazione finora

- Human Rights in The Secondary SchoolDocumento57 pagineHuman Rights in The Secondary SchoolJacaNessuna valutazione finora

- ATM BrochuresDocumento5 pagineATM Brochuresगुंजन सिन्हाNessuna valutazione finora

- Power Electronics For RenewablesDocumento22 paginePower Electronics For RenewablesShiv Prakash M.Tech., Electrical Engineering, IIT(BHU)Nessuna valutazione finora

- 2012 Fall TSJ s03 The Mystery of The Gospel PT 1 - Stuart GreavesDocumento5 pagine2012 Fall TSJ s03 The Mystery of The Gospel PT 1 - Stuart Greavesapi-164301844Nessuna valutazione finora

- Polygamy A Very Short Introduction Pearsall Sarah M S Download PDF ChapterDocumento51 paginePolygamy A Very Short Introduction Pearsall Sarah M S Download PDF Chapterharry.bailey869100% (5)

- Bocconi PE and VC CourseraDocumento15 pagineBocconi PE and VC CourseraMuskanDodejaNessuna valutazione finora

- DharmakirtiDocumento7 pagineDharmakirtialephfirmino1Nessuna valutazione finora

- Max3080 Max3089Documento21 pagineMax3080 Max3089Peter BirdNessuna valutazione finora

- Lista Destinatari Tema IDocumento4 pagineLista Destinatari Tema INicola IlieNessuna valutazione finora

- Arne Langaskens - HerbalistDocumento3 pagineArne Langaskens - HerbalistFilipNessuna valutazione finora

- Thesis - Behaviour of Prefabricated Modular Buildings Subjected To Lateral Loads PDFDocumento247 pagineThesis - Behaviour of Prefabricated Modular Buildings Subjected To Lateral Loads PDFFumaça FilosóficaNessuna valutazione finora

- Power Systems Kuestion PDFDocumento39 paginePower Systems Kuestion PDFaaaNessuna valutazione finora