Potrebbero piacerti anche

- Penny Stock Success: Tips for Investing in Cheap StocksDa EverandPenny Stock Success: Tips for Investing in Cheap StocksNessuna valutazione finora

- The Ultimate Guide To Wholesaling Real Estate: How To Find, Sign And Close Your First 100 DealsDa EverandThe Ultimate Guide To Wholesaling Real Estate: How To Find, Sign And Close Your First 100 DealsNessuna valutazione finora

- Value InvestingDocumento24 pagineValue InvestingjucazarNessuna valutazione finora

- Go For The GoldDocumento3 pagineGo For The GoldPratyoosh DwivediNessuna valutazione finora

- Manny Koshbin - Real StateDocumento11 pagineManny Koshbin - Real StateMichael A. Alonso RodriguezNessuna valutazione finora

- Options Trading For BeginnersDocumento146 pagineOptions Trading For BeginnersMohaideen Subaire100% (5)

- M&A Success - How Midsize Sellers Cash OutDocumento5 pagineM&A Success - How Midsize Sellers Cash OutQuynh Le Thi NhuNessuna valutazione finora

- Covered Call Expert ReportDocumento50 pagineCovered Call Expert Reporttvadmaker100% (2)

- 7 Stock Buying Mistakes and How To Avoid ThemDocumento5 pagine7 Stock Buying Mistakes and How To Avoid ThemMohammad IskandarNessuna valutazione finora

- 9 Points To Check Before Picking A MultibaggerDocumento17 pagine9 Points To Check Before Picking A MultibaggerbhatambarekarNessuna valutazione finora

- Buying Real Estate Without Cash or Credit (Review and Analysis of Conti and Finkel's Book)Da EverandBuying Real Estate Without Cash or Credit (Review and Analysis of Conti and Finkel's Book)Valutazione: 5 su 5 stelle5/5 (1)

- Tips of InvestmentDocumento6 pagineTips of InvestmentR.v. NaveenanNessuna valutazione finora

- Options Trading THE COMPLETE CRASH COURSE 3 Books in 1 How To Trade Options A Beginnerss Guide To Investing and Making - (Warren Ray Benjamin) (Z-Library)Documento168 pagineOptions Trading THE COMPLETE CRASH COURSE 3 Books in 1 How To Trade Options A Beginnerss Guide To Investing and Making - (Warren Ray Benjamin) (Z-Library)katiyarm51Nessuna valutazione finora

- Ultimate Income StrategyDocumento7 pagineUltimate Income StrategyPyrantel Pamoate0% (1)

- Book Review - One Upon Wall StreetDocumento20 pagineBook Review - One Upon Wall StreetPriya UpadhyayNessuna valutazione finora

- Rule 1Documento7 pagineRule 1margiant76100% (1)

- Stock Marketplace Guide That Will Work For Any Person.20121205.125834Documento2 pagineStock Marketplace Guide That Will Work For Any Person.20121205.125834anon_69098189Nessuna valutazione finora

- 7 Home Buying Secrets: What Every Home Buyer Needs To Know To Gain An Unfair AdvantageDa Everand7 Home Buying Secrets: What Every Home Buyer Needs To Know To Gain An Unfair AdvantageNessuna valutazione finora

- Jim Dalton's Principles To Live by in The New YearDocumento4 pagineJim Dalton's Principles To Live by in The New YearRichard Jones100% (5)

- Rule 1 of Investing: How to Always Be on the Right Side of the MarketDa EverandRule 1 of Investing: How to Always Be on the Right Side of the MarketValutazione: 4 su 5 stelle4/5 (3)

- Li Lu ExtractsDocumento3 pagineLi Lu ExtractsdasharathiNessuna valutazione finora

- Payback Time (Review and Analysis of Town's Book)Da EverandPayback Time (Review and Analysis of Town's Book)Nessuna valutazione finora

- Mini Storage Auctions: Step By Step Blueprint For Making Money With Mini Storage AuctionsDa EverandMini Storage Auctions: Step By Step Blueprint For Making Money With Mini Storage AuctionsNessuna valutazione finora

- Intelligent Investor: Investing Guide To Analyzing The Stock Market And Making Smart InvestmentsDa EverandIntelligent Investor: Investing Guide To Analyzing The Stock Market And Making Smart InvestmentsValutazione: 5 su 5 stelle5/5 (39)

- 115 Profitable Investing IdeasDocumento9 pagine115 Profitable Investing IdeasVinit DhullaNessuna valutazione finora

- Strong Negotiating Principles Set The Foundation For A Deal: Cma Management March 2010Documento5 pagineStrong Negotiating Principles Set The Foundation For A Deal: Cma Management March 2010Rahma WirdaNessuna valutazione finora

- Summary of Michelle Seiler Tucker & Sharon Lechter's Exit RichDa EverandSummary of Michelle Seiler Tucker & Sharon Lechter's Exit RichNessuna valutazione finora

- Jim Cramer's Real Money (Review and Analysis of Cramer's Book)Da EverandJim Cramer's Real Money (Review and Analysis of Cramer's Book)Nessuna valutazione finora

- Houseflipping PDFDocumento110 pagineHouseflipping PDFquedyah100% (2)

- It's A Whole New Ball Game: With Creative FinancingDocumento33 pagineIt's A Whole New Ball Game: With Creative Financingrnj1230Nessuna valutazione finora

- Trading Options My Way BookDocumento83 pagineTrading Options My Way BookkosurugNessuna valutazione finora

- Benjamin Graham Security Analysis PortfolioDocumento4 pagineBenjamin Graham Security Analysis PortfolioSen LeeNessuna valutazione finora

- 18 Real Estate Investing Tips & Strategies to Maximize ProfitsDa Everand18 Real Estate Investing Tips & Strategies to Maximize ProfitsValutazione: 5 su 5 stelle5/5 (1)

- AARM PSX Lesson 8Documento7 pagineAARM PSX Lesson 8mahboob_qayyumNessuna valutazione finora

- Ten Rules For Bargaining Success. You Do Not Have To Use A: 6.1 Rule 1: Be PreparedDocumento18 pagineTen Rules For Bargaining Success. You Do Not Have To Use A: 6.1 Rule 1: Be PreparedO KiNessuna valutazione finora

- 6 Common Problems Real Estate Brokers Encounter and How To Solve ThemDocumento2 pagine6 Common Problems Real Estate Brokers Encounter and How To Solve ThemKemuel RabiNessuna valutazione finora

- Making A Purchase Offer On A Small BusinessDocumento125 pagineMaking A Purchase Offer On A Small BusinessSuhail Gattan100% (2)

- Exit Strategies For Your BusinessDocumento6 pagineExit Strategies For Your Businessnajjarsteve100% (1)

- Don Fishback Ofb - 80 PDFDocumento90 pagineDon Fishback Ofb - 80 PDFCristina0% (1)

- In the Trader's Mind: Learn to Think Like a Real Trader and Manage Money Profitably to Generate Wealth and Live in AbundanceDa EverandIn the Trader's Mind: Learn to Think Like a Real Trader and Manage Money Profitably to Generate Wealth and Live in AbundanceNessuna valutazione finora

- 10 Estrategia para InvertirDocumento13 pagine10 Estrategia para InvertirMauricio Herrera DiazNessuna valutazione finora

- What Causes Small Businesses To FailDocumento11 pagineWhat Causes Small Businesses To Failmounirs719883Nessuna valutazione finora

- Selling Your Fitzroy Home: Insider Secrets for Getting Maximum Value in Any MarketDa EverandSelling Your Fitzroy Home: Insider Secrets for Getting Maximum Value in Any MarketNessuna valutazione finora

- GCAM Initial Letter 2020-03-27Documento13 pagineGCAM Initial Letter 2020-03-27Anil GowdaNessuna valutazione finora

- The Keys To Successful InvestingDocumento4 pagineThe Keys To Successful InvestingArnaldoBritoAraújoNessuna valutazione finora

- Trading HorsepowerDocumento15 pagineTrading HorsepowerfernandohNessuna valutazione finora

- Billion Dollar Portfolio: How to Create a Real Estate EmpireDa EverandBillion Dollar Portfolio: How to Create a Real Estate EmpireNessuna valutazione finora

- AS-IS:THE ROADMAP TO FLIPPING HOUSES: THE SECRET STEPS TO INVESTING IN REAL ESTATE, WHOLESALING, AND FLIPPING HOUSES WITH LITTLE TO NO MONEYDa EverandAS-IS:THE ROADMAP TO FLIPPING HOUSES: THE SECRET STEPS TO INVESTING IN REAL ESTATE, WHOLESALING, AND FLIPPING HOUSES WITH LITTLE TO NO MONEYNessuna valutazione finora

- Negotiation in Real EstateDocumento13 pagineNegotiation in Real EstateSiddhartha KamatNessuna valutazione finora

- OPTIONS TRADING CRASH COURSE: Mastering Strategies for Financial Success (2023 Guide for Beginners)Da EverandOPTIONS TRADING CRASH COURSE: Mastering Strategies for Financial Success (2023 Guide for Beginners)Nessuna valutazione finora

- Generate Monthly Cash Flow by Selling OptionsDocumento23 pagineGenerate Monthly Cash Flow by Selling OptionsCHAIMA CHICHA100% (2)

- Share Tweet: by Ben KillerbyDocumento4 pagineShare Tweet: by Ben KillerbyCarlos Mario AgueroNessuna valutazione finora

- Airline ConsolidationDocumento1 paginaAirline ConsolidationPNWBizBrokerNessuna valutazione finora

- Resurrection ChronologyDocumento1 paginaResurrection ChronologyPNWBizBrokerNessuna valutazione finora

- Bankers DozenDocumento3 pagineBankers DozenPNWBizBrokerNessuna valutazione finora

- LTR 18-03.17Documento1 paginaLTR 18-03.17PNWBizBrokerNessuna valutazione finora

- Capitilization RateDocumento1 paginaCapitilization RatePNWBizBrokerNessuna valutazione finora

- 2009 Thru 2016 Econ StatsDocumento1 pagina2009 Thru 2016 Econ StatsPNWBizBrokerNessuna valutazione finora

- 2014 DealflowDocumento1 pagina2014 DealflowPNWBizBrokerNessuna valutazione finora

- SBA Loan 2Documento1 paginaSBA Loan 2PNWBizBrokerNessuna valutazione finora

- SBA Loan SecretsDocumento3 pagineSBA Loan SecretsPNWBizBrokerNessuna valutazione finora

- SBA Loan 2Documento1 paginaSBA Loan 2PNWBizBrokerNessuna valutazione finora

- ChemistryDocumento1 paginaChemistryPNWBizBrokerNessuna valutazione finora

- Sources of FinanceDocumento1 paginaSources of FinancePNWBizBrokerNessuna valutazione finora

- Calving The Cash CowDocumento1 paginaCalving The Cash CowPNWBizBrokerNessuna valutazione finora

- SBA LoanDocumento1 paginaSBA LoanPNWBizBrokerNessuna valutazione finora

- Master 44633 DME Profile1 2FBDocumento1 paginaMaster 44633 DME Profile1 2FBPNWBizBrokerNessuna valutazione finora

- Scan0067 Page1 Image1Documento1 paginaScan0067 Page1 Image1PNWBizBrokerNessuna valutazione finora

- Retail PharmaciesDocumento1 paginaRetail PharmaciesPNWBizBrokerNessuna valutazione finora

- Rates of Return PDFDocumento1 paginaRates of Return PDFPNWBizBrokerNessuna valutazione finora

- Aviation Related Business For SaleDocumento1 paginaAviation Related Business For SalePNWBizBrokerNessuna valutazione finora

- HR 2274Documento1 paginaHR 2274PNWBizBrokerNessuna valutazione finora

- Preparing For The SaleDocumento1 paginaPreparing For The SalePNWBizBrokerNessuna valutazione finora

- 1120S For S CorpsDocumento22 pagine1120S For S CorpsPNWBizBrokerNessuna valutazione finora

- Client 44660 ProfileDocumento1 paginaClient 44660 ProfilePNWBizBrokerNessuna valutazione finora

- PDFDocumento1 paginaPDFPNWBizBrokerNessuna valutazione finora

- A Tale of Three EEQ DealsADocumento1 paginaA Tale of Three EEQ DealsAPNWBizBrokerNessuna valutazione finora

- Sources of FinanceDocumento1 paginaSources of FinancePNWBizBrokerNessuna valutazione finora

- Business Owners Top Ten ExcusesDocumento3 pagineBusiness Owners Top Ten ExcusesPNWBizBrokerNessuna valutazione finora

- North South University: Course-ACT310, Sec: 01 Individual Assignment On APEX Foods LTDDocumento10 pagineNorth South University: Course-ACT310, Sec: 01 Individual Assignment On APEX Foods LTDMostafa haqueNessuna valutazione finora

- 197 Dodge v. Ford Motor Co.Documento1 pagina197 Dodge v. Ford Motor Co.MlaNessuna valutazione finora

- Paper Pattern: Do Not Copy The Questions OnDocumento4 paginePaper Pattern: Do Not Copy The Questions OnMANISHA GARGNessuna valutazione finora

- Appendix eDocumento2 pagineAppendix eapi-283357075Nessuna valutazione finora

- Defect and DeficiencyDocumento3 pagineDefect and DeficiencyNitish Pai DukleNessuna valutazione finora

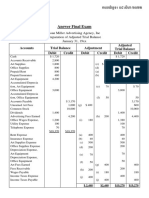

- Answer Final Exam (POA)Documento2 pagineAnswer Final Exam (POA)Phâk Tèr ÑgNessuna valutazione finora

- LGU Budget CycleDocumento3 pagineLGU Budget CycleDelfinNessuna valutazione finora

- Answer KeysDocumento26 pagineAnswer Keysmia uyNessuna valutazione finora

- Popescu & Diaconu (2009)Documento6 paginePopescu & Diaconu (2009)kautsarekaNessuna valutazione finora

- FRA Class NotesDocumento16 pagineFRA Class NotesUtkarsh Sinha100% (1)

- SAP Reports Record Third Quarter 2011 Software RevenueDocumento18 pagineSAP Reports Record Third Quarter 2011 Software RevenueVersion2dkNessuna valutazione finora

- Microns20 DraftDocumento294 pagineMicrons20 DraftadhavvikasNessuna valutazione finora

- Bessrawl Corporation Is A U S Based Company That Prepares Its ConsolidatedDocumento1 paginaBessrawl Corporation Is A U S Based Company That Prepares Its ConsolidatedFreelance WorkerNessuna valutazione finora

- Paradise Island Resort A Completed Business PlanDocumento30 pagineParadise Island Resort A Completed Business PlanMohdShahrukh100% (2)

- Lesson 10 - Manufacturing BusinessDocumento4 pagineLesson 10 - Manufacturing BusinessVISITACION JAIRUS GWENNessuna valutazione finora

- Bronze Adora Case StudyDocumento8 pagineBronze Adora Case StudyTitiNessuna valutazione finora

- RR No. 11-2018Documento90 pagineRR No. 11-2018Leticia TaclasNessuna valutazione finora

- RFM Business Review PDFDocumento32 pagineRFM Business Review PDFJessicaNessuna valutazione finora

- Wacc and MMDocumento2 pagineWacc and MMThảo NguyễnNessuna valutazione finora

- Syntech FibresDocumento33 pagineSyntech FibresSaaDii KhanNessuna valutazione finora

- Marc Lavoie History and Methods of Post Keynesian Economics 184458Documento34 pagineMarc Lavoie History and Methods of Post Keynesian Economics 184458José Ignacio Fuentes PeñaililloNessuna valutazione finora

- REED FileDocumento4 pagineREED FileJake VargasNessuna valutazione finora

- Installment Sales LectureDocumento10 pagineInstallment Sales LecturePenny TratiaNessuna valutazione finora

- Homework CVP & BEDocumento11 pagineHomework CVP & BEYamato De Jesus NakazawaNessuna valutazione finora

- Term Paper FinanceDocumento49 pagineTerm Paper FinanceKristine Astorga-NgNessuna valutazione finora

- FAR 2 Final Departmental Examination 2022Documento35 pagineFAR 2 Final Departmental Examination 2022ILOVE MATURED FANSNessuna valutazione finora

- 1701 Bir Form 2006 2013-2019Documento9 pagine1701 Bir Form 2006 2013-2019Jessie Boy Balino BalderamaNessuna valutazione finora

- Biotechnology Positioning and What Matters in 2014Documento196 pagineBiotechnology Positioning and What Matters in 2014dickygNessuna valutazione finora

- RER Appendix 46 1 SampleDocumento1 paginaRER Appendix 46 1 SampleMary Grace Lagdamen PerochoNessuna valutazione finora

- Quizzer rfbt1 PDFDocumento8 pagineQuizzer rfbt1 PDFleighNessuna valutazione finora