Potrebbero piacerti anche

- Economy@Glance Jun'09Documento3 pagineEconomy@Glance Jun'09Amirreza ,Nessuna valutazione finora

- HCMF Investor Letter October 2009 FINALDocumento24 pagineHCMF Investor Letter October 2009 FINALAbsolute Return100% (1)

- Economy@Glance Sep'09Documento3 pagineEconomy@Glance Sep'09Amirreza ,Nessuna valutazione finora

- The Week That Just Passed March 12, 2010Documento4 pagineThe Week That Just Passed March 12, 2010WallstreetableNessuna valutazione finora

- Global Commodity Prices, Monetary Transmission, and Exchange Rate Pass-Through in The Pacific IslandsDocumento16 pagineGlobal Commodity Prices, Monetary Transmission, and Exchange Rate Pass-Through in The Pacific IslandslukeniaNessuna valutazione finora

- Ideas & InsightsDocumento2 pagineIdeas & Insightsag rNessuna valutazione finora

- Southeast Texas Labor StatisticsDocumento1 paginaSoutheast Texas Labor StatisticsCharlie FoxworthNessuna valutazione finora

- Baltimore Metropolitan Area: Market ReportDocumento21 pagineBaltimore Metropolitan Area: Market ReportAnonymous Feglbx5Nessuna valutazione finora

- Gmo - For Whom The Bond TollsDocumento8 pagineGmo - For Whom The Bond Tollsfreemind3682Nessuna valutazione finora

- CHP 5 Annual Money 07Documento38 pagineCHP 5 Annual Money 07owltbigNessuna valutazione finora

- Philippine Rice Trade Liberalization: Impacts On Agriculture and The Economy, and Alternative Policy ActionsDocumento12 paginePhilippine Rice Trade Liberalization: Impacts On Agriculture and The Economy, and Alternative Policy ActionsJofred Dela VegaNessuna valutazione finora

- Florida's August Employment Figures Released: Charlie Crist Cynthia R. LorenzoDocumento16 pagineFlorida's August Employment Figures Released: Charlie Crist Cynthia R. LorenzoMichael AllenNessuna valutazione finora

- Florida's November Employment Figures ReleasedDocumento16 pagineFlorida's November Employment Figures ReleasedMichael AllenNessuna valutazione finora

- Accommodation Supply Analysis in Launceston Part 1Documento34 pagineAccommodation Supply Analysis in Launceston Part 1The ExaminerNessuna valutazione finora

- Crisis TimelineDocumento8 pagineCrisis TimelineSoberLookNessuna valutazione finora

- Florida's June Employment Figures Released: Governor DirectorDocumento16 pagineFlorida's June Employment Figures Released: Governor DirectorMichael AllenNessuna valutazione finora

- Inflation Cools, But Stays High: For Personal, Non-Commercial Use OnlyDocumento34 pagineInflation Cools, But Stays High: For Personal, Non-Commercial Use OnlyRazvan Catalin CostinNessuna valutazione finora

- Annual Newsletter 2012 13Documento24 pagineAnnual Newsletter 2012 13Sabarish T ENessuna valutazione finora

- Florida's July Employment Figures Released: Charlie Crist Cynthia R. LorenzoDocumento16 pagineFlorida's July Employment Figures Released: Charlie Crist Cynthia R. LorenzoMichael AllenNessuna valutazione finora

- ch015Documento11 paginech015iatfirmforyouNessuna valutazione finora

- 2015 Priorities of Energy Policy of Japan Under AbenomicsDocumento14 pagine2015 Priorities of Energy Policy of Japan Under AbenomicsHằng ĐặngNessuna valutazione finora

- Florida's September Employment Figures Released: Charlie Crist Cynthia R. LorenzoDocumento16 pagineFlorida's September Employment Figures Released: Charlie Crist Cynthia R. LorenzoMichael AllenNessuna valutazione finora

- Goldman Asia Conviction Call Catch-Up 13sep10Documento11 pagineGoldman Asia Conviction Call Catch-Up 13sep10tanmartinNessuna valutazione finora

- I. Views On The EconomyDocumento3 pagineI. Views On The EconomyThanh NguyenNessuna valutazione finora

- CME - Comparing E-Minis and ETFs - Sep2012 PDFDocumento8 pagineCME - Comparing E-Minis and ETFs - Sep2012 PDFbearsqNessuna valutazione finora

- The Global Liquidity Tracker - 22 Apr 22Documento13 pagineThe Global Liquidity Tracker - 22 Apr 22Apurva ShethNessuna valutazione finora

- RBI Annual Policy 2011-12 ReviewDocumento2 pagineRBI Annual Policy 2011-12 ReviewclevinnashNessuna valutazione finora

- Al Ahli Bank of Kuwait - Egypt - MMF - November 2017 - English - Monthly ReportDocumento1 paginaAl Ahli Bank of Kuwait - Egypt - MMF - November 2017 - English - Monthly ReportSobolNessuna valutazione finora

- Leveraging Crowdsourced Earnings Forecasts (40 charactersDocumento13 pagineLeveraging Crowdsourced Earnings Forecasts (40 charactersAnonymous pb0lJ4n5jNessuna valutazione finora

- WFP Guidelines 2020Documento82 pagineWFP Guidelines 2020Tina Grace CruzNessuna valutazione finora

- Tracking Financial ConditionsDocumento14 pagineTracking Financial ConditionsSathishNessuna valutazione finora

- MER March 2021Documento30 pagineMER March 2021Arden Muhumuza KitomariNessuna valutazione finora

- Update On IDFC Arbitrage FundDocumento6 pagineUpdate On IDFC Arbitrage FundGNessuna valutazione finora

- MER January 2022Documento29 pagineMER January 2022Arden Muhumuza KitomariNessuna valutazione finora

- Enhanced Services Package Implementation: Costs, Administrative Decision Making, and Agency LeadershipDocumento24 pagineEnhanced Services Package Implementation: Costs, Administrative Decision Making, and Agency LeadershipThunder PigNessuna valutazione finora

- Impact of Covid-19 On Air Cargo Transport IndustryDocumento7 pagineImpact of Covid-19 On Air Cargo Transport IndustryWahaj Hafeez MughalNessuna valutazione finora

- The Global Liquidity Tracker - 27 May 22Documento5 pagineThe Global Liquidity Tracker - 27 May 22Apurva ShethNessuna valutazione finora

- Florida's October Employment Figures Released: TallahasseeDocumento16 pagineFlorida's October Employment Figures Released: TallahasseeMichael AllenNessuna valutazione finora

- AEOA PMS Factsheet Sep2023Documento5 pagineAEOA PMS Factsheet Sep2023nuthan.10986Nessuna valutazione finora

- PESTLE Analysis TemplatesDocumento4 paginePESTLE Analysis TemplatesazimasNessuna valutazione finora

- Indian fixed income market update and outlookDocumento2 pagineIndian fixed income market update and outlookAnubhav TripathiNessuna valutazione finora

- Impact of Covid-19 On Air Cargo Transport IndustryDocumento13 pagineImpact of Covid-19 On Air Cargo Transport IndustryWahaj Hafeez MughalNessuna valutazione finora

- Expense and Budget 08Documento10 pagineExpense and Budget 08DCameron21Nessuna valutazione finora

- The Global Liquidity Tracker - 17 Jun 22Documento9 pagineThe Global Liquidity Tracker - 17 Jun 22Apurva ShethNessuna valutazione finora

- rhb-report-my_banks_sector-update_20190903_rhb-25301621779206685d6cc49b3d11fDocumento9 paginerhb-report-my_banks_sector-update_20190903_rhb-25301621779206685d6cc49b3d11fLeow Ann HongNessuna valutazione finora

- BBM Long Short Fund Performance January 2008Documento1 paginaBBM Long Short Fund Performance January 2008pelekNessuna valutazione finora

- Chapter 2Documento17 pagineChapter 2Salvy BaulNessuna valutazione finora

- Gerald CorcoranDocumento9 pagineGerald CorcoranMarketsWikiNessuna valutazione finora

- Al Rajhi Bank: Less Affected Than Its Local and Regional PeersDocumento31 pagineAl Rajhi Bank: Less Affected Than Its Local and Regional PeersAhmedHany Mohamed SayedNessuna valutazione finora

- The Global Liquidity Tracker - 06 May 22Documento8 pagineThe Global Liquidity Tracker - 06 May 22Apurva ShethNessuna valutazione finora

- Kotak Mahindra Bank Limited Managements Discussion and Analysis FY18Documento38 pagineKotak Mahindra Bank Limited Managements Discussion and Analysis FY18ss gNessuna valutazione finora

- Using Big Data To Improve Clinical CareDocumento32 pagineUsing Big Data To Improve Clinical CareXiaodong WangNessuna valutazione finora

- Global Investment Policy Committee Notes December 15, 2010: Overall Outlook Recommended AllocationDocumento4 pagineGlobal Investment Policy Committee Notes December 15, 2010: Overall Outlook Recommended Allocationankan4000Nessuna valutazione finora

- Indonesia EconomicsDocumento6 pagineIndonesia EconomicsNyoman RiyoNessuna valutazione finora

- Get The Power of Equity and Debt With Sbi Dual Advantage Fund - Series XxiiDocumento4 pagineGet The Power of Equity and Debt With Sbi Dual Advantage Fund - Series Xxiiarghya000Nessuna valutazione finora

- ALS-Facilitator AIPDocumento7 pagineALS-Facilitator AIPCristina Mendoza100% (1)

- PESTLE Analysis TemplatesDocumento4 paginePESTLE Analysis Templatesdevidas11100% (1)

- October 2009Documento3 pagineOctober 2009Amirreza ,Nessuna valutazione finora

- Economy@Glance May'09Documento3 pagineEconomy@Glance May'09Amirreza ,Nessuna valutazione finora

- Economy@Glance Aug 2009Documento3 pagineEconomy@Glance Aug 2009Amirreza ,Nessuna valutazione finora

- India: Economy@Glance Apr'09Documento4 pagineIndia: Economy@Glance Apr'09Amirreza ,100% (3)

- Economy@Glance July 2009Documento4 pagineEconomy@Glance July 2009Amirreza ,100% (2)

- Office Market Review Q1 - 2009Documento28 pagineOffice Market Review Q1 - 2009Amirreza ,Nessuna valutazione finora

- India: Economy@Glance Jan 09Documento3 pagineIndia: Economy@Glance Jan 09Amirreza ,Nessuna valutazione finora

- India: Economy@Glance Feb 09Documento4 pagineIndia: Economy@Glance Feb 09Amirreza ,Nessuna valutazione finora

- Hotel Market Review Booklet 2008 QTR 4Documento28 pagineHotel Market Review Booklet 2008 QTR 4Amirreza ,100% (23)

- India: Economy@Glance Dec-08 FinalDocumento1 paginaIndia: Economy@Glance Dec-08 FinalAmirreza ,Nessuna valutazione finora

- The Commercial Observer - Sept. 14, 2010Documento75 pagineThe Commercial Observer - Sept. 14, 2010Jesse CostelloNessuna valutazione finora

- RBI ROI FormatDocumento11 pagineRBI ROI FormatSandeep SandyNessuna valutazione finora

- Servicemembers' Guide to SCRA ProtectionsDocumento4 pagineServicemembers' Guide to SCRA Protectionsradny enageNessuna valutazione finora

- Cryptarith 1Documento24 pagineCryptarith 1Subhendu Ghosh0% (2)

- Prudential Regulations by SBP For SME FinancingDocumento40 paginePrudential Regulations by SBP For SME FinancingsirfanalizaidiNessuna valutazione finora

- IMF's Role in the Global Financial CrisisDocumento9 pagineIMF's Role in the Global Financial Crisissimmi kaushikNessuna valutazione finora

- Real Estate Dictionary - A Glossary of Indian RE TermsDocumento34 pagineReal Estate Dictionary - A Glossary of Indian RE TermsHarsh Shah100% (1)

- State Sen. Eric Lesser 2018 SFIDocumento16 pagineState Sen. Eric Lesser 2018 SFIDusty ChristensenNessuna valutazione finora

- Analysis On Customer Service Department Activities Of: HBL, Itahari BranchDocumento50 pagineAnalysis On Customer Service Department Activities Of: HBL, Itahari BranchSujan BajracharyaNessuna valutazione finora

- Lease FinancingDocumento37 pagineLease Financingpuspa Raj upadhayayNessuna valutazione finora

- HUD PEMCO Forfeiture and Extension Policy (Revised 031212)Documento3 pagineHUD PEMCO Forfeiture and Extension Policy (Revised 031212)ACGRealEstateNessuna valutazione finora

- Sample: MERS Mortgage Language Has Been Inserted As Blue TextDocumento3 pagineSample: MERS Mortgage Language Has Been Inserted As Blue TextRichie CollinsNessuna valutazione finora

- Project On Role of Credit Rating Agencies of Loan of Bank of BarodaDocumento42 pagineProject On Role of Credit Rating Agencies of Loan of Bank of BarodaVaishaliNessuna valutazione finora

- Umesh Bajaj REPORT1Documento63 pagineUmesh Bajaj REPORT1Harapalsinh DarabarNessuna valutazione finora

- Sales Nov 20Documento10 pagineSales Nov 20Maribel Nicole LopezNessuna valutazione finora

- Scripta 1COJ 3 2017 StudentDocumento50 pagineScripta 1COJ 3 2017 Studentsekeresova.nikolaNessuna valutazione finora

- Isaac Kornbluh On Real Estate ScamsDocumento3 pagineIsaac Kornbluh On Real Estate ScamsJacob KornbluhNessuna valutazione finora

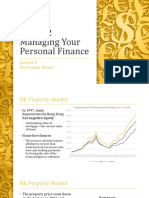

- GE1202 Managing Your Personal Finance: Purchasing HomesDocumento33 pagineGE1202 Managing Your Personal Finance: Purchasing HomesAiden LANNessuna valutazione finora

- 124416-1998-Medel v. Court of AppealsDocumento7 pagine124416-1998-Medel v. Court of AppealsaifapnglnnNessuna valutazione finora

- Banks Core Technology Conundrum Reaches An Inflection PointDocumento9 pagineBanks Core Technology Conundrum Reaches An Inflection Pointjuliae.delacourNessuna valutazione finora

- NSNP 100 Application FormDocumento7 pagineNSNP 100 Application FormRonaldo HertezNessuna valutazione finora

- Personal Financial StatementDocumento9 paginePersonal Financial StatementTrading CuesNessuna valutazione finora

- Vitamin D discovery boosts healthDocumento32 pagineVitamin D discovery boosts healthva15la15Nessuna valutazione finora

- Foreclosure of Mortgages in Connecticut Law Library 2011 EditionDocumento96 pagineForeclosure of Mortgages in Connecticut Law Library 2011 EditionCarrieonic100% (1)

- OMB 2004 SpreadsheetDocumento700 pagineOMB 2004 Spreadsheetrs314861100% (2)

- Types of Banks, Banking Relationships, and Insurance Recovery LimitsDocumento6 pagineTypes of Banks, Banking Relationships, and Insurance Recovery LimitsAdrian CampillaNessuna valutazione finora

- PNB v Timbol: Court of Appeals reverses RTC decision on annulment of real estate mortgageDocumento3 paginePNB v Timbol: Court of Appeals reverses RTC decision on annulment of real estate mortgageCharisse Christianne Yu CabanlitNessuna valutazione finora

- Bar Questions in Sales, Lease, Agency, and PartnershipDocumento75 pagineBar Questions in Sales, Lease, Agency, and PartnershipReuel RealinNessuna valutazione finora

- West Sherburne TribuneDocumento16 pagineWest Sherburne TribunewestribNessuna valutazione finora

- 2023/2024 ASVAB For Dummies (+ 7 Practice Tests, Flashcards, & Videos Online)Da Everand2023/2024 ASVAB For Dummies (+ 7 Practice Tests, Flashcards, & Videos Online)Nessuna valutazione finora

- EMT (Emergency Medical Technician) Crash Course with Online Practice Test, 2nd Edition: Get a Passing Score in Less TimeDa EverandEMT (Emergency Medical Technician) Crash Course with Online Practice Test, 2nd Edition: Get a Passing Score in Less TimeValutazione: 3.5 su 5 stelle3.5/5 (3)

- Outliers by Malcolm Gladwell - Book Summary: The Story of SuccessDa EverandOutliers by Malcolm Gladwell - Book Summary: The Story of SuccessValutazione: 4.5 su 5 stelle4.5/5 (17)

- Nursing School Entrance Exams: HESI A2 / NLN PAX-RN / PSB-RN / RNEE / TEASDa EverandNursing School Entrance Exams: HESI A2 / NLN PAX-RN / PSB-RN / RNEE / TEASNessuna valutazione finora

- Auto Parts Storekeeper: Passbooks Study GuideDa EverandAuto Parts Storekeeper: Passbooks Study GuideNessuna valutazione finora

- Radiographic Testing: Theory, Formulas, Terminology, and Interviews Q&ADa EverandRadiographic Testing: Theory, Formulas, Terminology, and Interviews Q&ANessuna valutazione finora

- The PMP Project Management Professional Certification Exam Study Guide PMBOK Seventh 7th Edition: The Complete Exam Prep With Practice Tests and Insider Tips & Tricks | Achieve a 98% Pass Rate on Your First AttemptDa EverandThe PMP Project Management Professional Certification Exam Study Guide PMBOK Seventh 7th Edition: The Complete Exam Prep With Practice Tests and Insider Tips & Tricks | Achieve a 98% Pass Rate on Your First AttemptNessuna valutazione finora

- The NCLEX-RN Exam Study Guide: Premium Edition: Proven Methods to Pass the NCLEX-RN Examination with Confidence – Extensive Next Generation NCLEX (NGN) Practice Test Questions with AnswersDa EverandThe NCLEX-RN Exam Study Guide: Premium Edition: Proven Methods to Pass the NCLEX-RN Examination with Confidence – Extensive Next Generation NCLEX (NGN) Practice Test Questions with AnswersNessuna valutazione finora

- EMT (Emergency Medical Technician) Crash Course Book + OnlineDa EverandEMT (Emergency Medical Technician) Crash Course Book + OnlineValutazione: 4.5 su 5 stelle4.5/5 (4)

- Real Property, Law Essentials: Governing Law for Law School and Bar Exam PrepDa EverandReal Property, Law Essentials: Governing Law for Law School and Bar Exam PrepNessuna valutazione finora

- Storekeeper I: Passbooks Study GuideDa EverandStorekeeper I: Passbooks Study GuideNessuna valutazione finora

- ASE A1 Engine Repair Study Guide: Complete Review & Test Prep For The ASE A1 Engine Repair Exam: With Three Full-Length Practice Tests & AnswersDa EverandASE A1 Engine Repair Study Guide: Complete Review & Test Prep For The ASE A1 Engine Repair Exam: With Three Full-Length Practice Tests & AnswersNessuna valutazione finora

- The Science of Self-Discipline: The Willpower, Mental Toughness, and Self-Control to Resist Temptation and Achieve Your GoalsDa EverandThe Science of Self-Discipline: The Willpower, Mental Toughness, and Self-Control to Resist Temptation and Achieve Your GoalsValutazione: 4.5 su 5 stelle4.5/5 (76)

- USMLE Step 1: Integrated Vignettes: Must-know, high-yield reviewDa EverandUSMLE Step 1: Integrated Vignettes: Must-know, high-yield reviewValutazione: 4.5 su 5 stelle4.5/5 (7)

- Programmer Aptitude Test (PAT): Passbooks Study GuideDa EverandProgrammer Aptitude Test (PAT): Passbooks Study GuideNessuna valutazione finora

- Intermediate Accounting 2: a QuickStudy Digital Reference GuideDa EverandIntermediate Accounting 2: a QuickStudy Digital Reference GuideNessuna valutazione finora

- 2024 – 2025 FAA Drone License Exam Guide: A Simplified Approach to Passing the FAA Part 107 Drone License Exam at a sitting With Test Questions and AnswersDa Everand2024 – 2025 FAA Drone License Exam Guide: A Simplified Approach to Passing the FAA Part 107 Drone License Exam at a sitting With Test Questions and AnswersNessuna valutazione finora

- PTCE - Pharmacy Technician Certification Exam Flashcard Book + OnlineDa EverandPTCE - Pharmacy Technician Certification Exam Flashcard Book + OnlineNessuna valutazione finora

- Improve Your Global Business English: The Essential Toolkit for Writing and Communicating Across BordersDa EverandImprove Your Global Business English: The Essential Toolkit for Writing and Communicating Across BordersValutazione: 4 su 5 stelle4/5 (14)

- Check Your English Vocabulary for TOEFL: Essential words and phrases to help you maximise your TOEFL scoreDa EverandCheck Your English Vocabulary for TOEFL: Essential words and phrases to help you maximise your TOEFL scoreValutazione: 5 su 5 stelle5/5 (1)

- Summary of Sapiens: A Brief History of Humankind By Yuval Noah HarariDa EverandSummary of Sapiens: A Brief History of Humankind By Yuval Noah HarariValutazione: 1 su 5 stelle1/5 (3)

- NCLEX-RN Exam Prep 2024-2025: 500 NCLEX-RN Test Prep Questions and Answers with ExplanationsDa EverandNCLEX-RN Exam Prep 2024-2025: 500 NCLEX-RN Test Prep Questions and Answers with ExplanationsNessuna valutazione finora