Potrebbero piacerti anche

- Poverty: Its Illegal Causes and Legal Cure: Lysander SpoonerDa EverandPoverty: Its Illegal Causes and Legal Cure: Lysander SpoonerNessuna valutazione finora

- Stop! Illegal Predatory Lending: A Self-Help GuideDa EverandStop! Illegal Predatory Lending: A Self-Help GuideNessuna valutazione finora

- Defeat Foreclosure: Save Your House,Your Credit and Your Rights.Da EverandDefeat Foreclosure: Save Your House,Your Credit and Your Rights.Nessuna valutazione finora

- The Self-Help Guide to the Law: Contracts and Sales Agreements for Non-Lawyers: Guide for Non-Lawyers, #5Da EverandThe Self-Help Guide to the Law: Contracts and Sales Agreements for Non-Lawyers: Guide for Non-Lawyers, #5Nessuna valutazione finora

- Code Breaker; The § 83 Equation: The Tax Code’s Forgotten ParagraphDa EverandCode Breaker; The § 83 Equation: The Tax Code’s Forgotten ParagraphValutazione: 3.5 su 5 stelle3.5/5 (2)

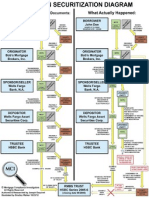

- Explanation of Securitization By: Joe Esquivel (MCI)Documento3 pagineExplanation of Securitization By: Joe Esquivel (MCI)Billy Bowles0% (1)

- Beware Note Article by - Bill-ButlerDocumento7 pagineBeware Note Article by - Bill-ButlerWonderland ExplorerNessuna valutazione finora

- MSFraud Forum PageDocumento23 pagineMSFraud Forum PageJohn Reed100% (1)

- Get Outta Jail Free Card “Jim Crow’s last stand at perpetuating slavery” Non-Unanimous Jury Verdicts & Voter SuppressionDa EverandGet Outta Jail Free Card “Jim Crow’s last stand at perpetuating slavery” Non-Unanimous Jury Verdicts & Voter SuppressionValutazione: 5 su 5 stelle5/5 (1)

- Securities and Exchange Commission (SEC) - Sec1661Documento4 pagineSecurities and Exchange Commission (SEC) - Sec1661highfinanceNessuna valutazione finora

- Petition for Certiorari – Patent Case 01-438 - Federal Rule of Civil Procedure 52(a)Da EverandPetition for Certiorari – Patent Case 01-438 - Federal Rule of Civil Procedure 52(a)Nessuna valutazione finora

- Naked Guide to Bonds: What You Need to Know -- Stripped Down to the Bare EssentialsDa EverandNaked Guide to Bonds: What You Need to Know -- Stripped Down to the Bare EssentialsNessuna valutazione finora

- Lawfully Yours: The Realm of Business, Government and LawDa EverandLawfully Yours: The Realm of Business, Government and LawNessuna valutazione finora

- Traffic Tickets. Don't Get Mad. Get Them Dismissed. Stories From The Streets.Da EverandTraffic Tickets. Don't Get Mad. Get Them Dismissed. Stories From The Streets.Valutazione: 4 su 5 stelle4/5 (1)

- Anti-SLAPP Law Modernized: The Uniform Public Expression Protection ActDa EverandAnti-SLAPP Law Modernized: The Uniform Public Expression Protection ActNessuna valutazione finora

- Custom and PracticeDocumento5 pagineCustom and PracticeRichard Franklin KesslerNessuna valutazione finora

- The Artificial Person and the Color of Law: How to Take Back the "Consent"! Social Geometry of LifeDa EverandThe Artificial Person and the Color of Law: How to Take Back the "Consent"! Social Geometry of LifeValutazione: 4.5 su 5 stelle4.5/5 (9)

- How To File Your Own Bankruptcy: The Step-by-Step Handbook to Filing Your Own Bankruptcy PetitionDa EverandHow To File Your Own Bankruptcy: The Step-by-Step Handbook to Filing Your Own Bankruptcy PetitionNessuna valutazione finora

- Notice of Default Must Have Signature Of.....Documento3 pagineNotice of Default Must Have Signature Of.....83jjmackNessuna valutazione finora

- An Inexplicable Deception: A State Corruption of JusticeDa EverandAn Inexplicable Deception: A State Corruption of JusticeNessuna valutazione finora

- Quantum of Justice - The Fraud of Foreclosure and the Illegal Securitization of Notes by Wall Street: The Fraud of Foreclosure and the Illegal Securitization of Notes by Wall StreetDa EverandQuantum of Justice - The Fraud of Foreclosure and the Illegal Securitization of Notes by Wall Street: The Fraud of Foreclosure and the Illegal Securitization of Notes by Wall StreetNessuna valutazione finora

- FORECLOSE ON THE FRAUDSTERS - PUT BANK OF AMERICA IN RECEIVERSHIP - White Collar Expert Calls For FDIC To Take Control of BofADocumento8 pagineFORECLOSE ON THE FRAUDSTERS - PUT BANK OF AMERICA IN RECEIVERSHIP - White Collar Expert Calls For FDIC To Take Control of BofA83jjmack100% (2)

- Mortgage Fraud PresentationDocumento5 pagineMortgage Fraud Presentation92589258Nessuna valutazione finora

- Constitution of the State of Minnesota — 1876 VersionDa EverandConstitution of the State of Minnesota — 1876 VersionNessuna valutazione finora

- Petition for Certiorari Denied Without Opinion: Patent Case 96-1178Da EverandPetition for Certiorari Denied Without Opinion: Patent Case 96-1178Nessuna valutazione finora

- I. Amendment Modification Waiver: Unsecured Promissory Note (Installment Payments)Documento3 pagineI. Amendment Modification Waiver: Unsecured Promissory Note (Installment Payments)Emman Dumayas100% (1)

- Courts and Procedure in England and in New JerseyDa EverandCourts and Procedure in England and in New JerseyNessuna valutazione finora

- The Declaration of Independence: A Play for Many ReadersDa EverandThe Declaration of Independence: A Play for Many ReadersNessuna valutazione finora

- Petition for Certiorari Denied Without Opinion: Patent Case 98-1151Da EverandPetition for Certiorari Denied Without Opinion: Patent Case 98-1151Nessuna valutazione finora

- The Ultimate Weapon in Debt Elimination: Unlocking the Secrets in Debt EliminationDa EverandThe Ultimate Weapon in Debt Elimination: Unlocking the Secrets in Debt EliminationValutazione: 5 su 5 stelle5/5 (1)

- Business Was Established After The Disaster: Pdcrecons@sba - GovDocumento2 pagineBusiness Was Established After The Disaster: Pdcrecons@sba - GovVince KimmetNessuna valutazione finora

- What Everyone Ought to Know About: Debt Relief Today! Some Plain Talk About Today's Economy That no one Talks About!Da EverandWhat Everyone Ought to Know About: Debt Relief Today! Some Plain Talk About Today's Economy That no one Talks About!Nessuna valutazione finora

- That Man from Nebraska - Confronting the ConstitutionDa EverandThat Man from Nebraska - Confronting the ConstitutionNessuna valutazione finora

- The administration and you – A handbook: Principles of administrative law concerning relations between individuals and public authoritiesDa EverandThe administration and you – A handbook: Principles of administrative law concerning relations between individuals and public authoritiesNessuna valutazione finora

- Milstead No AuthorityDocumento5 pagineMilstead No AuthorityArgusJHultNessuna valutazione finora

- FRAUDULENT Foreclosure Action BY F.D.I.C. SEIZED BANKUNITED, FSBDocumento11 pagineFRAUDULENT Foreclosure Action BY F.D.I.C. SEIZED BANKUNITED, FSBAlbertelli_Law100% (1)

- Chas Beaman v. Mountain America Federal Credit UnionDocumento16 pagineChas Beaman v. Mountain America Federal Credit UnionAnonymous WCaY6r100% (1)

- Commentary On The Security AgreementDocumento1 paginaCommentary On The Security AgreementJason HenryNessuna valutazione finora

- Mortgage Compliance Investigators - Mortgage Fraud InvestigationDocumento16 pagineMortgage Compliance Investigators - Mortgage Fraud InvestigationBilly Bowles100% (3)

- Attorneys' "Unbundled Service Pre - Litigation Package"Documento3 pagineAttorneys' "Unbundled Service Pre - Litigation Package"Damion EmholtzNessuna valutazione finora

- Mortgage Compliance Investigators - Chain of Title AnalysisDocumento31 pagineMortgage Compliance Investigators - Chain of Title AnalysisBilly BowlesNessuna valutazione finora

- Alvie's "Pig in A Poke"Documento9 pagineAlvie's "Pig in A Poke"Billy BowlesNessuna valutazione finora

- Explanation of Securitization By: Joe Esquivel (MCI)Documento3 pagineExplanation of Securitization By: Joe Esquivel (MCI)Billy Bowles0% (1)

- Mortgage Compliance Investigators - Loan Disposition Analysis (LDA)Documento15 pagineMortgage Compliance Investigators - Loan Disposition Analysis (LDA)Billy BowlesNessuna valutazione finora

- Mortgage Compliance Investigators - Level 3 Securitization AuditDocumento35 pagineMortgage Compliance Investigators - Level 3 Securitization AuditBilly Bowles100% (1)

- RMBS Loan Securitization Flow ChartDocumento1 paginaRMBS Loan Securitization Flow ChartBilly BowlesNessuna valutazione finora

- FANNIE MAE/FREDDIE MAC Loan Securitization Flow ChartDocumento1 paginaFANNIE MAE/FREDDIE MAC Loan Securitization Flow ChartBilly Bowles100% (1)