Potrebbero piacerti anche

- Purchase and Refinance Mortgage Process: A Handbook and Guide for Real Estate Mortgage!Da EverandPurchase and Refinance Mortgage Process: A Handbook and Guide for Real Estate Mortgage!Nessuna valutazione finora

- Voluntary Liens ReportDocumento6 pagineVoluntary Liens ReportMortgage Compliance Investigators100% (1)

- Property Title Trouble in Non Judicial Foreclosure States The Ibanez Time Bomb PDFDocumento54 pagineProperty Title Trouble in Non Judicial Foreclosure States The Ibanez Time Bomb PDFLisa Stinocher OHanlon100% (1)

- Letter Opposing Arbitration in Insurance PoliciesDocumento7 pagineLetter Opposing Arbitration in Insurance PoliciesTexas WatchNessuna valutazione finora

- Mortgage Compliance Investigators - Level 3 Securitization AuditDocumento35 pagineMortgage Compliance Investigators - Level 3 Securitization AuditBilly BowlesNessuna valutazione finora

- An Introduction To Mortgage Securitization and Foreclosures Involving Securitized TrustsDocumento17 pagineAn Introduction To Mortgage Securitization and Foreclosures Involving Securitized TrustsOccupyOurHomes100% (2)

- How To Purchase A Foreclosure Property From PASDocumento3 pagineHow To Purchase A Foreclosure Property From PASsin2begin2Nessuna valutazione finora

- Marie Mcdonnell (Certified Fraud Examiner) - Amicus Brief - Regarding The Ibanez & U.S. Bank CaseDocumento43 pagineMarie Mcdonnell (Certified Fraud Examiner) - Amicus Brief - Regarding The Ibanez & U.S. Bank Case83jjmack100% (4)

- 10-10-08 A) AP - Bank of America Issues Nationwide Moratorium On Foreclosures, B) CNBC - Foreclosure PrimerDocumento12 pagine10-10-08 A) AP - Bank of America Issues Nationwide Moratorium On Foreclosures, B) CNBC - Foreclosure PrimerHuman Rights Alert - NGO (RA)Nessuna valutazione finora

- TO: FROM: Jason Gold, Senior Fellow For Housing and Financial Services Policy REDocumento10 pagineTO: FROM: Jason Gold, Senior Fellow For Housing and Financial Services Policy REForeclosure FraudNessuna valutazione finora

- 5 YEAR OLD MORTGAGE LOAN RESCINDED BY JUDGE - McGee V Gregory FundingDocumento9 pagine5 YEAR OLD MORTGAGE LOAN RESCINDED BY JUDGE - McGee V Gregory Funding83jjmackNessuna valutazione finora

- Bailee Letter TermsDocumento3 pagineBailee Letter TermsHelpin HandNessuna valutazione finora

- Ferrel L. Agard,: DebtorDocumento20 pagineFerrel L. Agard,: DebtorJfresearch06100% (1)

- Beware Note Article by - Bill-ButlerDocumento7 pagineBeware Note Article by - Bill-ButlerWonderland ExplorerNessuna valutazione finora

- The Mortgage Fraud EnvelopeDocumento5 pagineThe Mortgage Fraud EnvelopenegotiablegohstNessuna valutazione finora

- Taking the Offensive Stance on ForeclosuresDocumento64 pagineTaking the Offensive Stance on ForeclosuresDonna EversNessuna valutazione finora

- Fiduciary ResponsibilityDocumento49 pagineFiduciary Responsibility:Nikolaj: Færch.Nessuna valutazione finora

- State of Ohio V GMAC, ALLY, Jeffrey StephanDocumento175 pagineState of Ohio V GMAC, ALLY, Jeffrey StephanForeclosure Fraud100% (1)

- Feds Foreclosure Enforcement 490070Documento17 pagineFeds Foreclosure Enforcement 490070NoahNemoNessuna valutazione finora

- Secure Method of Payment-Purchase Bank DraftDocumento12 pagineSecure Method of Payment-Purchase Bank DraftSudershan ThaibaNessuna valutazione finora

- Money in FinanceDocumento15 pagineMoney in FinanceRon LimNessuna valutazione finora

- UCC 3-203 (D) /states Adopted: Paradox/Catch 22 Neither Method Allows NegotiationDocumento1 paginaUCC 3-203 (D) /states Adopted: Paradox/Catch 22 Neither Method Allows NegotiationA. CampbellNessuna valutazione finora

- Pro Se Motion To Withdraw Capias Packet EnglishDocumento5 paginePro Se Motion To Withdraw Capias Packet EnglishBz Alina0% (1)

- Creditors Remedies in Muncipal Default, 1976 Duke Law Journal PDFDocumento34 pagineCreditors Remedies in Muncipal Default, 1976 Duke Law Journal PDFDaniel NashidNessuna valutazione finora

- SovereignDocumento151 pagineSovereignlenorescribdaccountNessuna valutazione finora

- NMTDocumento174 pagineNMTsfirleyNessuna valutazione finora

- Substitution of Trustee Document for CA Property TS # CA-08-169594-RMDocumento1 paginaSubstitution of Trustee Document for CA Property TS # CA-08-169594-RM1maximallNessuna valutazione finora

- I Am An Attorney So I Decided To Sue My Lender... (Conclusion: Failed) Mills v. First Horizon HomeDocumento6 pagineI Am An Attorney So I Decided To Sue My Lender... (Conclusion: Failed) Mills v. First Horizon Homejga30328Nessuna valutazione finora

- Bank Authorization Form for Foreclosure ResolutionDocumento1 paginaBank Authorization Form for Foreclosure ResolutionJim SchroederNessuna valutazione finora

- Notice of Trustees SaleDocumento1 paginaNotice of Trustees SaleChariseB2012Nessuna valutazione finora

- RHemricMeadowbrook Securitization AuditDocumento23 pagineRHemricMeadowbrook Securitization AuditrodclassteamNessuna valutazione finora

- Outline Foreclosure Defense - Tila & RespaDocumento13 pagineOutline Foreclosure Defense - Tila & RespaEdward BrownNessuna valutazione finora

- In Re Tiffany M. Kritharakis Debtor, United States Bankruptcy Court, District of Connecticut, Bridge Port Division No. 10-51328Documento10 pagineIn Re Tiffany M. Kritharakis Debtor, United States Bankruptcy Court, District of Connecticut, Bridge Port Division No. 10-51328Foreclosure FraudNessuna valutazione finora

- Letter To Attorney General PennyMac ModDocumento3 pagineLetter To Attorney General PennyMac Modboytoy 9774Nessuna valutazione finora

- Assignment Assumption and Recognition Agreement UBS IndymacDocumento10 pagineAssignment Assumption and Recognition Agreement UBS IndymacTBNessuna valutazione finora

- Case in Point - Foreclosure Mills, Judicial Fraud, Consumer ExploitationDocumento2 pagineCase in Point - Foreclosure Mills, Judicial Fraud, Consumer ExploitationBarbara Ann JacksonNessuna valutazione finora

- Oregon Judge Voids Foreclosure Sale June 2011Documento7 pagineOregon Judge Voids Foreclosure Sale June 201183jjmackNessuna valutazione finora

- Default and Enforcement: NtroductionDocumento20 pagineDefault and Enforcement: NtroductionSeniorNessuna valutazione finora

- QT Complaint NO Exhibits 62nd AveDocumento14 pagineQT Complaint NO Exhibits 62nd AveCheryl WhelestNessuna valutazione finora

- Dustin Rollins V Mers Class Action SuitDocumento46 pagineDustin Rollins V Mers Class Action Suitrebecca1966220% (1)

- Ibanez DecisionDocumento414 pagineIbanez Decisionmike_engle100% (1)

- Attorneys For C-III Asset Management LLC: LEGAL20390473.3Documento20 pagineAttorneys For C-III Asset Management LLC: LEGAL20390473.3Chapter 11 DocketsNessuna valutazione finora

- What Is A Statement of AccountsDocumento5 pagineWhat Is A Statement of AccountsHsin Wua ChiNessuna valutazione finora

- Judge Tom Rickhoff Letter To ReceiversDocumento3 pagineJudge Tom Rickhoff Letter To ReceiversKatherine SayreNessuna valutazione finora

- Procedures For The Issue of Pre/Post-possession DocumentsDocumento18 pagineProcedures For The Issue of Pre/Post-possession Documentsabc_dNessuna valutazione finora

- WellsDocumento3 pagineWellsForeclosure Fraud100% (1)

- AStep 1 Answer and CounterclaimDocumento16 pagineAStep 1 Answer and CounterclaimEl_NobleNessuna valutazione finora

- Get a Second Opinion before You Sign: What to do when the Bank says 'No' ? How to survive and thrive with Private Lending.Da EverandGet a Second Opinion before You Sign: What to do when the Bank says 'No' ? How to survive and thrive with Private Lending.Nessuna valutazione finora

- Real Estate Transactions and Foreclosure Control—A Home Mortgage Reference Handbook: The Causes and Remedies of Foreclosure PainsDa EverandReal Estate Transactions and Foreclosure Control—A Home Mortgage Reference Handbook: The Causes and Remedies of Foreclosure PainsNessuna valutazione finora

- Petition for Certiorari – Patent Case 01-438 - Federal Rule of Civil Procedure 52(a)Da EverandPetition for Certiorari – Patent Case 01-438 - Federal Rule of Civil Procedure 52(a)Nessuna valutazione finora

- Constitution of the State of Minnesota — 1876 VersionDa EverandConstitution of the State of Minnesota — 1876 VersionNessuna valutazione finora

- The Mortgage Loan Process: The Good, Bad, and Ugly but the Real - A Humorous, Sarcastic Walk-Through of a Dry, Boring Topic for BeginnersDa EverandThe Mortgage Loan Process: The Good, Bad, and Ugly but the Real - A Humorous, Sarcastic Walk-Through of a Dry, Boring Topic for BeginnersNessuna valutazione finora

- American Foreclosure: Everything U Need to Know About Preventing and BuyingDa EverandAmerican Foreclosure: Everything U Need to Know About Preventing and BuyingNessuna valutazione finora

- Nonprofit Law for Religious Organizations: Essential Questions & AnswersDa EverandNonprofit Law for Religious Organizations: Essential Questions & AnswersValutazione: 5 su 5 stelle5/5 (1)

- Real Estate Escapes: True tales of getting out of contracts, leases, prosecutions and legal liabilityDa EverandReal Estate Escapes: True tales of getting out of contracts, leases, prosecutions and legal liabilityNessuna valutazione finora

- Lawfully Yours: The Realm of Business, Government and LawDa EverandLawfully Yours: The Realm of Business, Government and LawNessuna valutazione finora

- Mortgage Compliance Investigators - Mortgage Fraud InvestigationDocumento16 pagineMortgage Compliance Investigators - Mortgage Fraud InvestigationBilly Bowles100% (3)

- Mortgage Compliance Investigators - Chain of Title AnalysisDocumento31 pagineMortgage Compliance Investigators - Chain of Title AnalysisBilly BowlesNessuna valutazione finora

- Attorneys' "Unbundled Service Pre - Litigation Package"Documento3 pagineAttorneys' "Unbundled Service Pre - Litigation Package"Damion EmholtzNessuna valutazione finora

- Alvie's "Pig in A Poke"Documento9 pagineAlvie's "Pig in A Poke"Billy BowlesNessuna valutazione finora

- Explanation of Securitization By: Joe Esquivel (MCI)Documento3 pagineExplanation of Securitization By: Joe Esquivel (MCI)Billy Bowles0% (1)

- What Will A Trustee's Deed Tell?Documento3 pagineWhat Will A Trustee's Deed Tell?Billy BowlesNessuna valutazione finora

- Mortgage Compliance Investigators - Level 3 Securitization AuditDocumento35 pagineMortgage Compliance Investigators - Level 3 Securitization AuditBilly BowlesNessuna valutazione finora

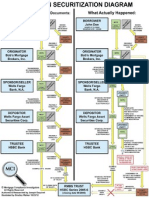

- RMBS Loan Securitization Flow ChartDocumento1 paginaRMBS Loan Securitization Flow ChartBilly BowlesNessuna valutazione finora

- FANNIE MAE/FREDDIE MAC Loan Securitization Flow ChartDocumento1 paginaFANNIE MAE/FREDDIE MAC Loan Securitization Flow ChartBilly Bowles100% (1)

- Test Bank For Financial Accounting 47 - 68Documento4 pagineTest Bank For Financial Accounting 47 - 68John_Dunkin300Nessuna valutazione finora

- De Thi Business Econ K58 CTTT C A Vinh Thi 14h30 Ngày 15.7.2021Documento2 pagineDe Thi Business Econ K58 CTTT C A Vinh Thi 14h30 Ngày 15.7.2021Trương Tuấn ĐạtNessuna valutazione finora

- Week 1 (MGMT 4512) Exercise Questions (Excel)Documento4 pagineWeek 1 (MGMT 4512) Exercise Questions (Excel)Big DripNessuna valutazione finora

- 03 - Quality Management SystemDocumento12 pagine03 - Quality Management SystemCharlon Adrian RuizNessuna valutazione finora

- JD & MainDocumento2 pagineJD & MainSourabh Sharma100% (1)

- SALUDO Vs CADocumento2 pagineSALUDO Vs CALaika CorralNessuna valutazione finora

- PR and The Party - The Truth About Media Relations in ChinaDocumento11 paginePR and The Party - The Truth About Media Relations in ChinaMSLNessuna valutazione finora

- Heartland Robotics Hires Scott Eckert As Chief Executive OfficerDocumento2 pagineHeartland Robotics Hires Scott Eckert As Chief Executive Officerapi-25891623Nessuna valutazione finora

- Temu 4Documento8 pagineTemu 4leddy teresaNessuna valutazione finora

- Tally 7.2Documento38 pagineTally 7.2sarthakmohanty697395Nessuna valutazione finora

- Quizzes Property Combined Questions and AnswersDocumento10 pagineQuizzes Property Combined Questions and AnswersCars CarandangNessuna valutazione finora

- AR Gapura Angkasa 2018Documento222 pagineAR Gapura Angkasa 2018Alexius SPNessuna valutazione finora

- IATF Internal Auditor 2019Documento1 paginaIATF Internal Auditor 2019Prakash kumarTripathiNessuna valutazione finora

- Q3 - Financial Accounting and Reporting (Partnership Accounting) All About Partnership DissolutionDocumento3 pagineQ3 - Financial Accounting and Reporting (Partnership Accounting) All About Partnership DissolutionALMA MORENANessuna valutazione finora

- MBA Financial Management Chapter 1 OverviewDocumento80 pagineMBA Financial Management Chapter 1 Overviewadiba10mkt67% (3)

- Process Costing Breakdown/TITLEDocumento76 pagineProcess Costing Breakdown/TITLEAnas4253Nessuna valutazione finora

- Psa 210Documento3 paginePsa 210Medina PangilinanNessuna valutazione finora

- PHA Training - Day 2Documento75 paginePHA Training - Day 2ahmad jamalNessuna valutazione finora

- 3017 Tutorial 7 SolutionsDocumento3 pagine3017 Tutorial 7 SolutionsNguyễn HảiNessuna valutazione finora

- (NAK) Northern Dynasty Presentation 2017-06-05Documento39 pagine(NAK) Northern Dynasty Presentation 2017-06-05Ken Storey100% (1)

- An Introduction To Integrated Marketing CommunicationsDocumento21 pagineAn Introduction To Integrated Marketing CommunicationsMEDISHETTY MANICHANDANANessuna valutazione finora

- CMM-006-15536-0006 - 6 - Radar AltimeterDocumento367 pagineCMM-006-15536-0006 - 6 - Radar AltimeterDadang100% (4)

- The Marketer's Guide To Travel Content: by Aaron TaubeDocumento18 pagineThe Marketer's Guide To Travel Content: by Aaron TaubeSike ThedeviantNessuna valutazione finora

- Strategic ManagementDocumento22 pagineStrategic ManagementAhmad Azhar Aman ShahNessuna valutazione finora

- Differences Between Sole ProprietorshipDocumento5 pagineDifferences Between Sole ProprietorshipUsman KhalidNessuna valutazione finora

- 21.SAP MM - Service ManagementDocumento8 pagine21.SAP MM - Service ManagementNiranjan NaiduNessuna valutazione finora

- Exposing the Financial Core of the Transnational Capitalist ClassDocumento26 pagineExposing the Financial Core of the Transnational Capitalist ClassMichinito05Nessuna valutazione finora

- Suza Business Plan (Honey Popcorn)Documento49 pagineSuza Business Plan (Honey Popcorn)Cartoon WalaNessuna valutazione finora

- The Effect of Management TrainingDocumento30 pagineThe Effect of Management TrainingPulak09100% (1)

- Steel Industry PitchDocumento17 pagineSteel Industry Pitchnavinmba2010Nessuna valutazione finora