Potrebbero piacerti anche

- Climate Variability and Its Impacts in Tanzania: Climatology of TanzaniaDa EverandClimate Variability and Its Impacts in Tanzania: Climatology of TanzaniaNessuna valutazione finora

- Corporate Finance Project Finance AssignmentDocumento10 pagineCorporate Finance Project Finance AssignmentGaurav PandeyNessuna valutazione finora

- © 2010 Financial Management Prepared By: Amyn WahidDocumento66 pagine© 2010 Financial Management Prepared By: Amyn Wahidfatimasal33m100% (1)

- Sample Business Plan 2015 PDFDocumento15 pagineSample Business Plan 2015 PDFRommel ParejaNessuna valutazione finora

- Financial LeverageDocumento21 pagineFinancial LeverageSarab Gurpreet BatraNessuna valutazione finora

- BoJ Project FInance Third EditionDocumento142 pagineBoJ Project FInance Third EditionbagirNessuna valutazione finora

- Chapter 4 Financial IntermediariesDocumento29 pagineChapter 4 Financial IntermediariesMinh ThuNessuna valutazione finora

- Statement of Cash Flows Indirect MethodDocumento3 pagineStatement of Cash Flows Indirect MethodheykmmyNessuna valutazione finora

- Equity Research Report On Mundra Port SEZDocumento73 pagineEquity Research Report On Mundra Port SEZRitesh100% (11)

- Project Appraisal & Impact Analysis: Product: 4325 - Course Code: c207 - c307Documento46 pagineProject Appraisal & Impact Analysis: Product: 4325 - Course Code: c207 - c307hariprasathkgNessuna valutazione finora

- Sources of FinanceDocumento26 pagineSources of Financevyasgautam28Nessuna valutazione finora

- Marginal Cost of Capital - CFA Level 1 - InvestopediaDocumento4 pagineMarginal Cost of Capital - CFA Level 1 - InvestopediajoysinhaNessuna valutazione finora

- Fin Man 1 FINANCIAL Ratio AnalysisDocumento15 pagineFin Man 1 FINANCIAL Ratio AnalysisAnnie EinnaNessuna valutazione finora

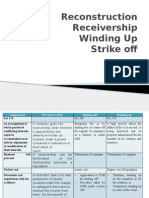

- Reconstruction Receivership Winding Up Strike OffDocumento71 pagineReconstruction Receivership Winding Up Strike OffMohammad Hasrul AkmalNessuna valutazione finora

- Teaching Notes-FMI-342 PDFDocumento162 pagineTeaching Notes-FMI-342 PDFArun PatelNessuna valutazione finora

- Managing IT in A Digital World: ObjectivesDocumento11 pagineManaging IT in A Digital World: ObjectivesKakada100% (1)

- Interest Rate ParityDocumento5 pagineInterest Rate Parityrosario correiaNessuna valutazione finora

- Long Term Source of Finance 222222Documento12 pagineLong Term Source of Finance 222222mandeep singhNessuna valutazione finora

- AFSA Cash Flow AnalysisDocumento19 pagineAFSA Cash Flow AnalysisRikhabh DasNessuna valutazione finora

- SynergyDocumento19 pagineSynergyYash AgarwalNessuna valutazione finora

- Part II Operations Management PDFDocumento178 paginePart II Operations Management PDFandrapradeshsse100% (1)

- Credit Risk ManagementDocumento3 pagineCredit Risk Managementamrut_bNessuna valutazione finora

- Haileleul Teshome MM Individual AssignmentDocumento5 pagineHaileleul Teshome MM Individual AssignmentHaileleul TeshomeNessuna valutazione finora

- Global Credit Exposure Management Policy - 2019 - PDF - Credit Risk - CreditDocumento86 pagineGlobal Credit Exposure Management Policy - 2019 - PDF - Credit Risk - CreditRavi PrajapatiNessuna valutazione finora

- Title of The Paper:: Mergers and Acquisitions Financial ManagementDocumento25 pagineTitle of The Paper:: Mergers and Acquisitions Financial ManagementfatinNessuna valutazione finora

- Debt and Global Economy: The Challenges and The Way-OutDocumento15 pagineDebt and Global Economy: The Challenges and The Way-Outbelayneh100% (1)

- Capital Structure Theory - Net Operating Income ApproachDocumento3 pagineCapital Structure Theory - Net Operating Income Approachoutlanderlord100% (1)

- Cost of CapitalDocumento8 pagineCost of CapitalAreeb BaqaiNessuna valutazione finora

- Residual Income ValuationDocumento21 pagineResidual Income ValuationqazxswNessuna valutazione finora

- Managers.: Investment Decisions Are Made by Investors and InvestmentDocumento5 pagineManagers.: Investment Decisions Are Made by Investors and InvestmentRe KhanNessuna valutazione finora

- Artical Review For WeekendDocumento18 pagineArtical Review For WeekendHabte DebeleNessuna valutazione finora

- Capital StructureDocumento4 pagineCapital StructurenaveenngowdaNessuna valutazione finora

- Trade Off TheoryDocumento1 paginaTrade Off TheoryHaider ShahNessuna valutazione finora

- Buena Terra Corporation Is Reviewing Its Capital Budget For The UpcomingDocumento2 pagineBuena Terra Corporation Is Reviewing Its Capital Budget For The UpcomingAmit PandeyNessuna valutazione finora

- Methods of Project Financing: Project Finance Equity Finance The ProjectDocumento9 pagineMethods of Project Financing: Project Finance Equity Finance The ProjectA vyasNessuna valutazione finora

- Consolidation GAAPDocumento77 pagineConsolidation GAAPMisganaw DebasNessuna valutazione finora

- Financial IntermediaryDocumento5 pagineFinancial IntermediarySmriti KhannaNessuna valutazione finora

- Analysis of Financial StatementsDocumento33 pagineAnalysis of Financial StatementsKushal Lapasia100% (1)

- Board Diversity and Its Effects On Bank Performance - An International Analysis PDFDocumento13 pagineBoard Diversity and Its Effects On Bank Performance - An International Analysis PDFDavid Adeabah OsafoNessuna valutazione finora

- Portfolio Management-Module One Discussion - MandoDocumento2 paginePortfolio Management-Module One Discussion - MandoDavid Luko ChifwaloNessuna valutazione finora

- Organizational Behavior Assignment 1Documento17 pagineOrganizational Behavior Assignment 1Olivia WongNessuna valutazione finora

- Assignment I-Summers-Decision TheoryDocumento2 pagineAssignment I-Summers-Decision TheorysaadNessuna valutazione finora

- Draft Research Report-1Documento23 pagineDraft Research Report-1Prince FranieNessuna valutazione finora

- Module 3 FinancingDocumento69 pagineModule 3 FinancingHoly BankNessuna valutazione finora

- Preparing Financial StatementsDocumento15 paginePreparing Financial StatementsAUDITOR97Nessuna valutazione finora

- Debt RatioDocumento7 pagineDebt RatioAamir BilalNessuna valutazione finora

- Liquidity ManagementDocumento35 pagineLiquidity ManagementJadMadiNessuna valutazione finora

- IGNOU MBA MS - 04 Solved Assignment 2011Documento12 pagineIGNOU MBA MS - 04 Solved Assignment 2011Nazif LcNessuna valutazione finora

- 3.shiftability Theory 1Documento2 pagine3.shiftability Theory 1Mohammad SaadmanNessuna valutazione finora

- 3 Case StudiesDocumento3 pagine3 Case Studies8110 Kamila0% (1)

- Accounting ResearchDocumento65 pagineAccounting ResearchTaqi DesaNessuna valutazione finora

- Venture Capital CH2&3 AssignmentDocumento2 pagineVenture Capital CH2&3 AssignmentRahmati RahmatullahNessuna valutazione finora

- Assignment PM The Case 1Documento3 pagineAssignment PM The Case 1Ali Khan88% (8)

- Cost of CapitalDocumento18 pagineCost of CapitalyukiNessuna valutazione finora

- Sharpe RatioDocumento7 pagineSharpe RatioSindhuja PalanichamyNessuna valutazione finora

- Chap 13Documento5 pagineChap 13Jade Marie FerrolinoNessuna valutazione finora

- Finance Case StudyDocumento8 pagineFinance Case StudyEvans MettoNessuna valutazione finora

- Chapter 3 Mini Case Working Papers Fall 2014Documento6 pagineChapter 3 Mini Case Working Papers Fall 2014ZachLoving100% (2)

- BFW 3331 T6 AnswersDocumento6 pagineBFW 3331 T6 AnswersDylanchong91Nessuna valutazione finora

- Bank Reconcilation StatementDocumento1 paginaBank Reconcilation StatementAbhijith PaiNessuna valutazione finora

- RTP Mod-2.4Documento81 pagineRTP Mod-2.4saideepika_bNessuna valutazione finora

- Cashbook SampleDocumento15 pagineCashbook Samplemaneesh_nayak3Nessuna valutazione finora

- CUTOMER Perception and Attitude Towards Bajaj Allianz PROJECT REPORTDocumento78 pagineCUTOMER Perception and Attitude Towards Bajaj Allianz PROJECT REPORTBabasab Patil (Karrisatte)Nessuna valutazione finora

- Back Office SerivceDocumento172 pagineBack Office SerivceAbhijith Pai100% (2)

- Financial GlossaryDocumento56 pagineFinancial Glossarygcu93Nessuna valutazione finora

- Questionnair NewDocumento5 pagineQuestionnair NewAbhijith PaiNessuna valutazione finora

- Lecture Credit and Collection Chapter 1Documento7 pagineLecture Credit and Collection Chapter 1Celso I. MendozaNessuna valutazione finora

- Process of Fundamental Analysis PDFDocumento8 pagineProcess of Fundamental Analysis PDFajay.1k7625100% (1)

- Sources of RiskDocumento2 pagineSources of RiskeswarlalbkNessuna valutazione finora

- 1 Erca - Natasha Group - 112923Documento17 pagine1 Erca - Natasha Group - 112923Amino BenitoNessuna valutazione finora

- Solutions Manual: Financial Accounting: Reporting, Analysis and Decision MakingDocumento61 pagineSolutions Manual: Financial Accounting: Reporting, Analysis and Decision MakingJeffrey Sanchez Rojas100% (2)

- Notice of Facts - The Bankers ManifestDocumento2 pagineNotice of Facts - The Bankers ManifestHarold Louis100% (2)

- WorldCom SummaryDocumento4 pagineWorldCom Summaryburka123100% (1)

- Intro To Skip TracingDocumento33 pagineIntro To Skip Tracinggoosebumps1942100% (2)

- Valley of Food Insecurity and Chronic HungerDocumento65 pagineValley of Food Insecurity and Chronic HungerVikas SamvadNessuna valutazione finora

- AALendingAdvancedPart4 PDFDocumento102 pagineAALendingAdvancedPart4 PDFlolitaferoz100% (2)

- Aviation Law ResearchDocumento23 pagineAviation Law Researchvelan naveen natrajNessuna valutazione finora

- Unit Number/ Heading Learning Outcomes: Intermediate Accounting Ii (Ae 16) Learning Material: Bonds PayableDocumento20 pagineUnit Number/ Heading Learning Outcomes: Intermediate Accounting Ii (Ae 16) Learning Material: Bonds PayablePillos Jr., ElimarNessuna valutazione finora

- Holyoke Property Receivership ListDocumento2 pagineHolyoke Property Receivership ListMike PlaisanceNessuna valutazione finora

- Week 14 Chapter 16 PC 4 - Wintersport V WhiteDocumento1 paginaWeek 14 Chapter 16 PC 4 - Wintersport V Whiteapi-340865637Nessuna valutazione finora

- Sports Authority BankruptcyDocumento21 pagineSports Authority BankruptcyZerohedgeNessuna valutazione finora

- Business Finance Lecture NotesDocumento118 pagineBusiness Finance Lecture NotesSmitaNessuna valutazione finora

- Recursion and Financial Maths AnswerDocumento23 pagineRecursion and Financial Maths AnswerZhiyong HuangNessuna valutazione finora

- FIN 205 Tutorial Questions Sem 3 2021Documento55 pagineFIN 205 Tutorial Questions Sem 3 2021黄于绮Nessuna valutazione finora

- IndiaRising KuveraDocumento35 pagineIndiaRising Kuveragauravmundhra2001Nessuna valutazione finora

- Analysis of Entrepreneurship Ecosystem in Narra, Palawan, PhilippinesDocumento23 pagineAnalysis of Entrepreneurship Ecosystem in Narra, Palawan, PhilippinesDarwin AniarNessuna valutazione finora

- IBPA Yield Curve: Daily Fair Price & Yield Indonesia Government Securities December 12, 2018Documento3 pagineIBPA Yield Curve: Daily Fair Price & Yield Indonesia Government Securities December 12, 2018Nelli MarselinaNessuna valutazione finora

- 0823.HK The Link REIT 2009-2010 Annual ReportDocumento198 pagine0823.HK The Link REIT 2009-2010 Annual Reportwalamaking100% (1)

- FIN081 P3 Quiz2 Short-Term-Financing AnswerDocumento4 pagineFIN081 P3 Quiz2 Short-Term-Financing AnswerMary Lyn DatuinNessuna valutazione finora

- Credit Bureau Report SampleDocumento5 pagineCredit Bureau Report SampleIndra ChanNessuna valutazione finora

- m1050 Credit Card Debt ProjectDocumento5 paginem1050 Credit Card Debt Projectapi-302403854Nessuna valutazione finora

- Kinds of ObligationDocumento428 pagineKinds of ObligationMrcharming Jadraque82% (39)

- Capital Adequacy CalculationDocumento9 pagineCapital Adequacy CalculationSyed Ameer HayderNessuna valutazione finora

- Chapter 2 Audit of ReceivablesDocumento33 pagineChapter 2 Audit of ReceivablesDominique Anne BenozaNessuna valutazione finora

- Managerial EconomicsDocumento4 pagineManagerial EconomicsCarina BratuNessuna valutazione finora

- Literally: A Detained Thing Technically: "Detention of A Corporeal Property On Account ofDocumento8 pagineLiterally: A Detained Thing Technically: "Detention of A Corporeal Property On Account ofamelia stephanieNessuna valutazione finora