Potrebbero piacerti anche

- P 14Documento728 pagineP 14Moaaz Ahmed100% (1)

- Duties and Taxes For Govt Purchase ProposalsDocumento45 pagineDuties and Taxes For Govt Purchase Proposalsdate_milindNessuna valutazione finora

- Central Excise DutyDocumento19 pagineCentral Excise DutyGurneet Kaur GujralNessuna valutazione finora

- Mining & Beneficiation Workshop on Finance for Non-Finance ExecutivesDocumento36 pagineMining & Beneficiation Workshop on Finance for Non-Finance ExecutivesSaikumar SelaNessuna valutazione finora

- 4 Applied Indirect TaxationDocumento316 pagine4 Applied Indirect TaxationSanjay VanjayNessuna valutazione finora

- Scheme 1Documento19 pagineScheme 1Jayesh ValwarNessuna valutazione finora

- Central Excise DutyDocumento3 pagineCentral Excise DutyRanvijay Kumar BhartiNessuna valutazione finora

- Drawback Section 75.Documento4 pagineDrawback Section 75.PRATHAMESH MUNGEKARNessuna valutazione finora

- ITX AssignmentDocumento4 pagineITX AssignmentDaniel_Solomon_9624Nessuna valutazione finora

- A Project Report: On / inDocumento30 pagineA Project Report: On / inNeeraj BhatiNessuna valutazione finora

- Indirect Tax GuideDocumento6 pagineIndirect Tax GuideSaloni GuptaNessuna valutazione finora

- Assessable Value: Prof. P. RajendranDocumento18 pagineAssessable Value: Prof. P. RajendranProfessor RajendranNessuna valutazione finora

- Applied Indirect TaxationDocumento349 pagineApplied Indirect TaxationVijetha K Murthy100% (1)

- Central Excise Act Notes For Self PreparationDocumento29 pagineCentral Excise Act Notes For Self PreparationVivek ReddyNessuna valutazione finora

- Various Schemes Like EOUDocumento14 pagineVarious Schemes Like EOUranger_passionNessuna valutazione finora

- Indirect Taxes: Excise, VAT and GSTDocumento19 pagineIndirect Taxes: Excise, VAT and GSTmanikaNessuna valutazione finora

- BY Vinod K Raju Musaliar College PathanamthittaDocumento20 pagineBY Vinod K Raju Musaliar College PathanamthittaAvinashNessuna valutazione finora

- Valuation of Excisable Goods: 3.1 Basis of Computing Duty PayableDocumento38 pagineValuation of Excisable Goods: 3.1 Basis of Computing Duty PayableVaishnaviNessuna valutazione finora

- Central Excise Duty BasicsDocumento20 pagineCentral Excise Duty Basicsvulbiz30Nessuna valutazione finora

- Relevant Indirect Tax Provisions ExplainedDocumento68 pagineRelevant Indirect Tax Provisions ExplainedVikas GuptaNessuna valutazione finora

- Indirect TaxDocumento8 pagineIndirect TaxPavan JayaprakashNessuna valutazione finora

- Central ExciseDocumento53 pagineCentral ExciseSuyash JainNessuna valutazione finora

- Excise DutyDocumento4 pagineExcise DutyDigvijay LakdeNessuna valutazione finora

- Excise Clearance For ExportsDocumento10 pagineExcise Clearance For ExportsRadhakrishna UppalapatiNessuna valutazione finora

- ProjectDocumento9 pagineProjectAkash JaipuriaNessuna valutazione finora

- Customs Duty Explained: Rates, Types, Objectives & DefinitionsDocumento24 pagineCustoms Duty Explained: Rates, Types, Objectives & DefinitionsSoujanya NagarajaNessuna valutazione finora

- Presentation1 1Documento31 paginePresentation1 1Faizan AhmedNessuna valutazione finora

- Business Law OverviewDocumento25 pagineBusiness Law Overviewapce501Nessuna valutazione finora

- Small Scale Exemption SchemeDocumento8 pagineSmall Scale Exemption SchemebakulhariaNessuna valutazione finora

- Export & Import Management FinalDocumento15 pagineExport & Import Management FinalNisha MenonNessuna valutazione finora

- Remaning TopicsDocumento7 pagineRemaning TopicsAbhishekNessuna valutazione finora

- Tax AssignmentDocumento20 pagineTax AssignmentAnamNessuna valutazione finora

- Duty Drawback India Presentation 2003Documento10 pagineDuty Drawback India Presentation 2003dinkar13375Nessuna valutazione finora

- Central Excise ActDocumento19 pagineCentral Excise ActPoonam MehtaNessuna valutazione finora

- Understanding Excise Duty in IndiaDocumento21 pagineUnderstanding Excise Duty in IndiajaskaranNessuna valutazione finora

- Import of Capital GoodsDocumento24 pagineImport of Capital GoodsPranav KumarNessuna valutazione finora

- Central Exercise Duty ExplainedDocumento10 pagineCentral Exercise Duty ExplainedKrishna RajputNessuna valutazione finora

- Tax Deduction at Source (TDS) : SalariesDocumento6 pagineTax Deduction at Source (TDS) : Salariesaniruddha_2012Nessuna valutazione finora

- Unit-1 GST (Continuation)Documento70 pagineUnit-1 GST (Continuation)Anurag KandariNessuna valutazione finora

- Customs Duties in India - Types, Rates, HS CodeDocumento14 pagineCustoms Duties in India - Types, Rates, HS CodeViraja GuruNessuna valutazione finora

- Types of Duty PDFDocumento27 pagineTypes of Duty PDFfirastiNessuna valutazione finora

- VatDocumento41 pagineVatRAM67% (3)

- Indirect Taxes - A Review: Applicability of Duties / Taxes - Excise Duty Customs Duty. Vat / CST Service TaxDocumento39 pagineIndirect Taxes - A Review: Applicability of Duties / Taxes - Excise Duty Customs Duty. Vat / CST Service TaxarungajankushNessuna valutazione finora

- Excise Registration: Advantages and Disadvantages of Indirect TaxesDocumento16 pagineExcise Registration: Advantages and Disadvantages of Indirect TaxesDinesh SinghNessuna valutazione finora

- Understanding Central Excise Duty in IndiaDocumento16 pagineUnderstanding Central Excise Duty in IndiaVinod PatelNessuna valutazione finora

- EOU Audit Guide - Key Documents, Areas of Focus, and Common ObjectionsDocumento5 pagineEOU Audit Guide - Key Documents, Areas of Focus, and Common Objectionsశ్రీనివాసకిరణ్కుమార్చతుర్వేదులNessuna valutazione finora

- NMIMS Global Access Course Export Import ProceduresDocumento11 pagineNMIMS Global Access Course Export Import ProceduresTeena RawatNessuna valutazione finora

- Nature of Central Excise Act ExplainedDocumento14 pagineNature of Central Excise Act ExplainedChanrdra MohanNessuna valutazione finora

- Central ExciseDocumento3 pagineCentral ExciseVenkata SwamyNessuna valutazione finora

- Customs DutyDocumento17 pagineCustoms DutyBabasab Patil (Karrisatte)100% (1)

- Excise DutyDocumento12 pagineExcise DutyshreeMaliNessuna valutazione finora

- Central Excise - Into & Basic ConceptsDocumento21 pagineCentral Excise - Into & Basic ConceptsMruduta JainNessuna valutazione finora

- Understand Customs Duty in IndiaDocumento17 pagineUnderstand Customs Duty in IndiaMubbashir Khan RanaNessuna valutazione finora

- I Direct TaxDocumento155 pagineI Direct TaxRajnish ShastriNessuna valutazione finora

- Central Excise Duty Rules for Levy in IndiaDocumento9 pagineCentral Excise Duty Rules for Levy in IndiaAzhar KhanNessuna valutazione finora

- Chapter 12Documento32 pagineChapter 12Ram SskNessuna valutazione finora

- Industrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisDa EverandIndustrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisNessuna valutazione finora

- Consti NotesDocumento115 pagineConsti NotesTIRUNAGIRI PRANAV SAINessuna valutazione finora

- Human Rights PDFDocumento111 pagineHuman Rights PDFRajveer Singh SekhonNessuna valutazione finora

- What Is An Alternative Dispute Resolution?Documento8 pagineWhat Is An Alternative Dispute Resolution?Rajveer Singh SekhonNessuna valutazione finora

- What Is An Alternative Dispute Resolution?Documento8 pagineWhat Is An Alternative Dispute Resolution?Rajveer Singh SekhonNessuna valutazione finora

- Consti NotesDocumento115 pagineConsti NotesTIRUNAGIRI PRANAV SAINessuna valutazione finora

- Crime Against ChildrenDocumento4 pagineCrime Against ChildrenRajveer Singh SekhonNessuna valutazione finora

- Human Rights PDFDocumento111 pagineHuman Rights PDFRajveer Singh SekhonNessuna valutazione finora

- Question Bank of Sem - 1 To Sem-9 of Faculty of Law PDFDocumento203 pagineQuestion Bank of Sem - 1 To Sem-9 of Faculty of Law PDFHasnain Qaiyumi0% (1)

- HAND WRITTEN Labour-Law-Notes PDFDocumento110 pagineHAND WRITTEN Labour-Law-Notes PDFRajveer Singh Sekhon100% (1)

- Syllabus of Law For AllDocumento3 pagineSyllabus of Law For AllRajveer Singh SekhonNessuna valutazione finora

- Act Box PDFDocumento65 pagineAct Box PDFdeveshwerNessuna valutazione finora

- Consti NotesDocumento115 pagineConsti NotesTIRUNAGIRI PRANAV SAINessuna valutazione finora

- Act Box PDFDocumento65 pagineAct Box PDFdeveshwerNessuna valutazione finora

- Act Box PDFDocumento65 pagineAct Box PDFdeveshwerNessuna valutazione finora

- Law of Crimes Notes on Elements and KindsDocumento9 pagineLaw of Crimes Notes on Elements and KindsRajveer Singh SekhonNessuna valutazione finora

- Industrial, Labour and General Laws (Module II Paper 7)Documento0 pagineIndustrial, Labour and General Laws (Module II Paper 7)Jhha KKhushbuNessuna valutazione finora

- CPC, 1908Documento271 pagineCPC, 1908kaustubh880% (1)

- Question Bank of Sem - 1 To Sem-9 of Faculty of Law PDFDocumento203 pagineQuestion Bank of Sem - 1 To Sem-9 of Faculty of Law PDFHasnain Qaiyumi0% (1)

- Notes On Law of CrimesDocumento9 pagineNotes On Law of CrimesRajveer Singh SekhonNessuna valutazione finora

- Law of Evidence Notes LLBDocumento216 pagineLaw of Evidence Notes LLBSpeedie records83% (47)

- Law NotesDocumento79 pagineLaw NotesRajveer Singh SekhonNessuna valutazione finora

- Adm TribunalsDocumento3 pagineAdm TribunalsRajveer Singh SekhonNessuna valutazione finora

- Limitation Act 1963Documento24 pagineLimitation Act 1963Dikshagoyal1230% (1)

- New Motor Vehicles Act ProvisionsDocumento7 pagineNew Motor Vehicles Act ProvisionsExpress Web86% (7)

- Sustainable DevelopmentDocumento8 pagineSustainable DevelopmentRajveer Singh SekhonNessuna valutazione finora

- Law of Crimes Notes on Elements and KindsDocumento9 pagineLaw of Crimes Notes on Elements and KindsRajveer Singh Sekhon0% (1)

- Road SafetyDocumento44 pagineRoad SafetySwararagam Audios And VideosNessuna valutazione finora

- Project Family LawDocumento17 pagineProject Family Lawravi_bhateja_2Nessuna valutazione finora

- Definition of International Law and its SourcesDocumento10 pagineDefinition of International Law and its SourcesRajveer Singh SekhonNessuna valutazione finora

- International Law NotesDocumento29 pagineInternational Law NotesAaditya BhattNessuna valutazione finora

- Case Dismissals For Lack of Standing To ForecloseDocumento28 pagineCase Dismissals For Lack of Standing To Foreclosejacque zidane100% (1)

- 10000003728Documento32 pagine10000003728Chapter 11 DocketsNessuna valutazione finora

- Corporate Financial Management Practice Exam QuestionsDocumento10 pagineCorporate Financial Management Practice Exam QuestionsAston CheeNessuna valutazione finora

- Chapter 3 Review Quiz SolutionsDocumento4 pagineChapter 3 Review Quiz SolutionsA. ZNessuna valutazione finora

- Summary Economics of Money Banking and Financial Markets Frederic S Mishkin PDFDocumento143 pagineSummary Economics of Money Banking and Financial Markets Frederic S Mishkin PDFJohn StephensNessuna valutazione finora

- Merchant Bank in IndiaDocumento14 pagineMerchant Bank in IndiaRk BainsNessuna valutazione finora

- AccA P4/3.7 - 2002 - Dec - QDocumento12 pagineAccA P4/3.7 - 2002 - Dec - Qroker_m3Nessuna valutazione finora

- Administrative Memorandum Civ10-ADocumento3 pagineAdministrative Memorandum Civ10-Agox3Nessuna valutazione finora

- Alpha Beta GammaDocumento27 pagineAlpha Beta GammaSarakhannnNessuna valutazione finora

- Financial Statement ReportingDocumento20 pagineFinancial Statement ReportingAshwini Khare0% (1)

- What You Need To Know About The Westbury Park TransitionDocumento4 pagineWhat You Need To Know About The Westbury Park Transitionapi-133522662Nessuna valutazione finora

- Coa - M2013-004 Cash Exam Manual PDFDocumento104 pagineCoa - M2013-004 Cash Exam Manual PDFAnie Guiling-Hadji Gaffar88% (8)

- Crump - The Phenomenon of Money (1981)Documento258 pagineCrump - The Phenomenon of Money (1981)Anonymous OOeTGKMAdD100% (1)

- ACCOUNTING COMPETENCY EXAM SAMPLEDocumento12 pagineACCOUNTING COMPETENCY EXAM SAMPLEAmber AJNessuna valutazione finora

- Guide To Bank Charges Circular To All Banks Other Financial Institutions and Mobile Payments OperatorsDocumento69 pagineGuide To Bank Charges Circular To All Banks Other Financial Institutions and Mobile Payments OperatorsOsemwengie OsahonNessuna valutazione finora

- Briault (1995) PDFDocumento13 pagineBriault (1995) PDFMiguel SzejnblumNessuna valutazione finora

- Bank of England's Financial Policy Committee: Powers and ProcessDocumento9 pagineBank of England's Financial Policy Committee: Powers and ProcessancasofiaNessuna valutazione finora

- TPA Act Introduction and Key DefinitionsDocumento41 pagineTPA Act Introduction and Key DefinitionsakhilNessuna valutazione finora

- Indian Mental Disability ActDocumento78 pagineIndian Mental Disability ActVinit YadavNessuna valutazione finora

- Cost of Capital 4Documento5 pagineCost of Capital 4sudarshan1985Nessuna valutazione finora

- Syllabus Credit ManagementDocumento2 pagineSyllabus Credit ManagementMd Salah UddinNessuna valutazione finora

- National Shelter ProgramDocumento43 pagineNational Shelter ProgramLara CayagoNessuna valutazione finora

- Wells Fargo Company AnalysisDocumento15 pagineWells Fargo Company Analysisapi-310628084Nessuna valutazione finora

- Project Appraisal - Stages FlowchartDocumento6 pagineProject Appraisal - Stages FlowchartAshokNessuna valutazione finora

- Apply for Hotel CreditDocumento3 pagineApply for Hotel CreditIkaLianiManurungNessuna valutazione finora

- Broiler Farming Income GuideDocumento16 pagineBroiler Farming Income GuideB.p. MugunthanNessuna valutazione finora

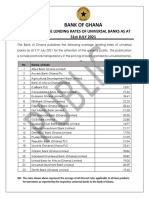

- Average Lending Rates As at July 2021Documento1 paginaAverage Lending Rates As at July 2021Fuaad DodooNessuna valutazione finora

- FIN 535 Week 10 HomeworkDocumento7 pagineFIN 535 Week 10 HomeworkDonald Shipman JrNessuna valutazione finora

- Karur Vysya Bank Is A Scheduled Commercial BankDocumento4 pagineKarur Vysya Bank Is A Scheduled Commercial BankMamtha KumarNessuna valutazione finora

- Adopt-A-Family: of The Palm Beaches, IncDocumento4 pagineAdopt-A-Family: of The Palm Beaches, Incm_constantine8807Nessuna valutazione finora