Potrebbero piacerti anche

- Game Audio - Tales of A Technical Sound Designer Volume 02Documento154 pagineGame Audio - Tales of A Technical Sound Designer Volume 02Joshua HuNessuna valutazione finora

- Fuel Injection PDFDocumento11 pagineFuel Injection PDFscaniaNessuna valutazione finora

- Rights, Duties and Liabilities of An AuditorDocumento8 pagineRights, Duties and Liabilities of An AuditorShailee ShahNessuna valutazione finora

- Cost AuditDocumento4 pagineCost AuditsanyamNessuna valutazione finora

- Checklist Code ReviewDocumento2 pagineChecklist Code ReviewTrang Đỗ Thu100% (1)

- Lecture Note-Foreign SubsidiaryDocumento10 pagineLecture Note-Foreign Subsidiaryptnyagortey91Nessuna valutazione finora

- Shirin Farhad StoryDocumento2 pagineShirin Farhad StoryFarhad HussainNessuna valutazione finora

- Auditor's Report On Financial StatementsDocumento10 pagineAuditor's Report On Financial StatementsNastya SelivanovaNessuna valutazione finora

- Cost AuditDocumento10 pagineCost AuditHasan AhmmedNessuna valutazione finora

- TOPIC 3d - Audit PlanningDocumento29 pagineTOPIC 3d - Audit PlanningLANGITBIRUNessuna valutazione finora

- New Python Basics AssignmentDocumento5 pagineNew Python Basics AssignmentRAHUL SONI0% (1)

- GlobalDocumento24 pagineGloballaleye_olumideNessuna valutazione finora

- WORKING CAPITAL - Meaning of Working CapitalDocumento23 pagineWORKING CAPITAL - Meaning of Working Capitalzubair100% (1)

- Advantages of Auditing For Joint Stock CorporationsDocumento3 pagineAdvantages of Auditing For Joint Stock CorporationsQari Nusratullah NooriNessuna valutazione finora

- ConferenceDocumento4 pagineConferenceYourElderSisterWeirdFriendNessuna valutazione finora

- Inflation Accounting New CourseDocumento11 pagineInflation Accounting New CourseAkshay Mhatre100% (1)

- Marine Policy in India and TypesDocumento16 pagineMarine Policy in India and TypesMiraRaiNessuna valutazione finora

- Introduction of Auditing: StructureDocumento56 pagineIntroduction of Auditing: Structureanon_696931352Nessuna valutazione finora

- Price Level Accounting by Rekha - 5212Documento30 paginePrice Level Accounting by Rekha - 5212Khesari Lal YadavNessuna valutazione finora

- ACC3600 Past Year Exam Questions and AnswersDocumento9 pagineACC3600 Past Year Exam Questions and AnswersKirsten Paton100% (1)

- Public Sector Accounting Homework SolutionsDocumento6 paginePublic Sector Accounting Homework SolutionsLoganPearcyNessuna valutazione finora

- Audit Reports and Professional EthicsDocumento20 pagineAudit Reports and Professional EthicsMushfiq SaikatNessuna valutazione finora

- Preparation For An AuditDocumento33 paginePreparation For An Auditanon_672065362Nessuna valutazione finora

- Bcom 3 Audit FinalDocumento17 pagineBcom 3 Audit FinalNayan MaldeNessuna valutazione finora

- Objectives of The Price PolicyDocumento3 pagineObjectives of The Price PolicyPrasanna Hegde100% (1)

- FactoringDocumento15 pagineFactoringddakcyNessuna valutazione finora

- Cost Audit ProjectDocumento23 pagineCost Audit ProjectHarshada SinghNessuna valutazione finora

- Auditing NotesDocumento65 pagineAuditing NotesTushar GaurNessuna valutazione finora

- Budgetary Control System and Inventory Management - Research Study - 150075041Documento3 pagineBudgetary Control System and Inventory Management - Research Study - 150075041aarohi bhattNessuna valutazione finora

- IPO Under Pricing and Short Run Performance in Bangladesh - Faisal MahmudDocumento54 pagineIPO Under Pricing and Short Run Performance in Bangladesh - Faisal MahmudM. A. Faisal Mahmud75% (4)

- Order To CashDocumento3 pagineOrder To CashPrashanth ChidambaramNessuna valutazione finora

- Financial Statements, Deals With An External Auditor's Responsibilities However, Both Internal andDocumento11 pagineFinancial Statements, Deals With An External Auditor's Responsibilities However, Both Internal andDanisa NdhlovuNessuna valutazione finora

- ManagementofcashDocumento7 pagineManagementofcashMd MonirNessuna valutazione finora

- Audit InvestigationsDocumento7 pagineAudit Investigationsafaniran33% (3)

- Audit Expectation Gap in AuditorDocumento3 pagineAudit Expectation Gap in AuditorTantanLeNessuna valutazione finora

- Topic 1 - Review Q&A (Pearson)Documento2 pagineTopic 1 - Review Q&A (Pearson)$t@r0867% (3)

- Abs Journal RankingDocumento52 pagineAbs Journal Rankingrizwan1001Nessuna valutazione finora

- Investment Avenues (Securities) in PakistanDocumento7 pagineInvestment Avenues (Securities) in PakistanPolite Charm100% (1)

- The Balanced Scorecard: A Tool To Implement StrategyDocumento39 pagineThe Balanced Scorecard: A Tool To Implement StrategyAilene QuintoNessuna valutazione finora

- Special Economic ZoneDocumento4 pagineSpecial Economic ZoneDhruvesh ModiNessuna valutazione finora

- Attributes and Features of InvestmentDocumento5 pagineAttributes and Features of InvestmentAashutosh ChandraNessuna valutazione finora

- Audit ProjectDocumento22 pagineAudit ProjectJashan100% (1)

- Explain Why Debt Is Usually Considered The Cheapest Source of Financing AvailableDocumento6 pagineExplain Why Debt Is Usually Considered The Cheapest Source of Financing AvailableAkhileshNessuna valutazione finora

- Audit & Assurance 2nd Lecture by Malik Kashif AwanDocumento15 pagineAudit & Assurance 2nd Lecture by Malik Kashif AwanMalik Kashif AwanNessuna valutazione finora

- Chapter01 2Documento10 pagineChapter01 2Subhankar PatraNessuna valutazione finora

- Valuation of Shares PDFDocumento62 pagineValuation of Shares PDFGarima100% (1)

- Corporate Taxation - Module I: Basic Concepts of Income Tax A. HistoryDocumento15 pagineCorporate Taxation - Module I: Basic Concepts of Income Tax A. HistoryDr Linda Mary SimonNessuna valutazione finora

- Taxable Event and Supply: Presentation By: - Ranvir Singh Rahul Banger Rollno: - 2024550Documento14 pagineTaxable Event and Supply: Presentation By: - Ranvir Singh Rahul Banger Rollno: - 2024550Gurinder SinghNessuna valutazione finora

- Auditing Chapter 2Documento26 pagineAuditing Chapter 2Balach MalikNessuna valutazione finora

- Define Internal Control.: Activity Sheet - Module 6Documento9 pagineDefine Internal Control.: Activity Sheet - Module 6Chris JacksonNessuna valutazione finora

- Divestment and PrivatisationDocumento16 pagineDivestment and Privatisationlali62Nessuna valutazione finora

- ACC803 Advanced Financial Reporting: Week 2: Financial Statement Preparation and PresentationDocumento21 pagineACC803 Advanced Financial Reporting: Week 2: Financial Statement Preparation and PresentationRavinesh PrasadNessuna valutazione finora

- Primary Role of Company AuditorDocumento5 paginePrimary Role of Company AuditorAshutosh GoelNessuna valutazione finora

- Price Level ChangesDocumento7 paginePrice Level Changestwyn774918100% (1)

- 4 Exam Part 2Documento4 pagine4 Exam Part 2RJ DAVE DURUHANessuna valutazione finora

- Unorganised Workers in India: Issues and ConcernsDocumento35 pagineUnorganised Workers in India: Issues and Concernssuresh0% (1)

- Capital and Revenue ExpendituereDocumento30 pagineCapital and Revenue ExpendituereDheeraj Seth0% (1)

- International Control SystemDocumento5 pagineInternational Control SystemCatherine JohnsonNessuna valutazione finora

- Market Efficiency PDFDocumento17 pagineMarket Efficiency PDFBatoul ShokorNessuna valutazione finora

- Post Graduate Programme in Management (PGP) AY: 2020-21 Term: Ii Title of The Course: Finance - I Credits: 3Documento6 paginePost Graduate Programme in Management (PGP) AY: 2020-21 Term: Ii Title of The Course: Finance - I Credits: 3Rohit PanditNessuna valutazione finora

- Importance of Mutual FundsDocumento14 pagineImportance of Mutual FundsMukesh Kumar SinghNessuna valutazione finora

- Characteristics of Effective Control SystemsDocumento2 pagineCharacteristics of Effective Control SystemsLoveleen KesarNessuna valutazione finora

- Investigation into the Adherence to Corporate Governance in Zimbabwe’s SME SectorDa EverandInvestigation into the Adherence to Corporate Governance in Zimbabwe’s SME SectorNessuna valutazione finora

- The Four Walls: Live Like the Wind, Free, Without HindrancesDa EverandThe Four Walls: Live Like the Wind, Free, Without HindrancesValutazione: 5 su 5 stelle5/5 (1)

- Auditing 2Documento47 pagineAuditing 2Sonu Harris GeorgeNessuna valutazione finora

- Auditing 9 15Documento12 pagineAuditing 9 15loyaextraNessuna valutazione finora

- Road To IELTS - ReadingDocumento7 pagineRoad To IELTS - ReadingOsama ElsayedNessuna valutazione finora

- POG Sign Off SheetDocumento1 paginaPOG Sign Off SheetFarhad HussainNessuna valutazione finora

- I e Lts Notice To CandidatesDocumento1 paginaI e Lts Notice To CandidatesFarhad HussainNessuna valutazione finora

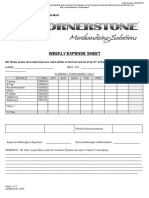

- Expense FormDocumento1 paginaExpense FormFarhad HussainNessuna valutazione finora

- Road To IELTS - ReadingDocumento7 pagineRoad To IELTS - ReadingOsama ElsayedNessuna valutazione finora

- Harvard CompleteDocumento15 pagineHarvard CompleteFahmi Muhammad AbdillahNessuna valutazione finora

- Admission Form For MComDocumento2 pagineAdmission Form For MComFarhad HussainNessuna valutazione finora

- Writing StructureDocumento1 paginaWriting StructureFarhad HussainNessuna valutazione finora

- IELTS Application Summary - Hussain.i.khan@Gmail - Com - GmailDocumento1 paginaIELTS Application Summary - Hussain.i.khan@Gmail - Com - GmailFarhad HussainNessuna valutazione finora

- Ends, Ways and Means: 3 Comments Strategy Real-World ExampleDocumento4 pagineEnds, Ways and Means: 3 Comments Strategy Real-World ExampleFarhad HussainNessuna valutazione finora

- VocabularyDocumento2 pagineVocabularyFarhad HussainNessuna valutazione finora

- Product Quality and Market SizeDocumento37 pagineProduct Quality and Market SizejoshidoanNessuna valutazione finora

- Essay Writing IELTSDocumento14 pagineEssay Writing IELTSFarhad HussainNessuna valutazione finora

- WW Ice Cream Sep 2015 - Bdoc - FinalDocumento12 pagineWW Ice Cream Sep 2015 - Bdoc - FinalFarhad HussainNessuna valutazione finora

- Affidavit of Personal PropertyDocumento2 pagineAffidavit of Personal PropertyFarhad HussainNessuna valutazione finora

- ArrivalFormSCHobart 2Documento2 pagineArrivalFormSCHobart 2fadi786Nessuna valutazione finora

- Article - How Do CFOs Make Capital Budgeting and Capital Structure DecisionsDocumento16 pagineArticle - How Do CFOs Make Capital Budgeting and Capital Structure DecisionsmssanNessuna valutazione finora

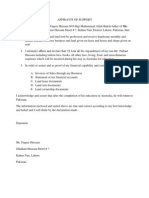

- Affidavit of SupportDocumento1 paginaAffidavit of SupportFarhad HussainNessuna valutazione finora

- Loan LetterDocumento3 pagineLoan LetterFarhad HussainNessuna valutazione finora

- Angro FinnancialDocumento25 pagineAngro FinnancialFarhad HussainNessuna valutazione finora

- Financial Statement AnalysisDocumento27 pagineFinancial Statement AnalysisFarhad Hussain100% (1)

- Article - How Do CFOs Make Capital Budgeting and Capital Structure DecisionsDocumento16 pagineArticle - How Do CFOs Make Capital Budgeting and Capital Structure DecisionsmssanNessuna valutazione finora

- Hafiz Muhammad Waseem CVDocumento1 paginaHafiz Muhammad Waseem CVFarhad HussainNessuna valutazione finora

- CB ArticleDocumento1 paginaCB ArticleFarhad HussainNessuna valutazione finora

- Presentation of E-ComDocumento17 paginePresentation of E-ComFarhad HussainNessuna valutazione finora

- Higher Algebra - Hall & KnightDocumento593 pagineHigher Algebra - Hall & KnightRam Gollamudi100% (2)

- Case: Wal-Mart's Global Expansion: Localization Strategy Adopted After Trial and ErrorDocumento14 pagineCase: Wal-Mart's Global Expansion: Localization Strategy Adopted After Trial and ErrorFarhad HussainNessuna valutazione finora

- WaqasDocumento11 pagineWaqasFarhad HussainNessuna valutazione finora

- Lesson Plan Outline - Rebounding - Perez - JoseDocumento7 pagineLesson Plan Outline - Rebounding - Perez - JoseJose PerezNessuna valutazione finora

- Student's T DistributionDocumento6 pagineStudent's T DistributionNur AliaNessuna valutazione finora

- Almutairy / Musa MR: Boarding PassDocumento1 paginaAlmutairy / Musa MR: Boarding PassMusaNessuna valutazione finora

- AppendixA LaplaceDocumento12 pagineAppendixA LaplaceSunny SunNessuna valutazione finora

- PET Formal Letter SamplesDocumento7 paginePET Formal Letter SamplesLe Anh ThuNessuna valutazione finora

- Multidimensional Scaling Groenen Velden 2004 PDFDocumento14 pagineMultidimensional Scaling Groenen Velden 2004 PDFjoséNessuna valutazione finora

- Esp 1904 A - 70 TPH o & M ManualDocumento50 pagineEsp 1904 A - 70 TPH o & M Manualpulakjaiswal85Nessuna valutazione finora

- SrsDocumento7 pagineSrsRahul Malhotra50% (2)

- Strategy Guide To Twilight Imperium Third EditionDocumento74 pagineStrategy Guide To Twilight Imperium Third Editioninquartata100% (1)

- 2062 TSSR Site Sharing - Rev02Documento44 pagine2062 TSSR Site Sharing - Rev02Rio DefragNessuna valutazione finora

- Luigi Cherubini Requiem in C MinorDocumento8 pagineLuigi Cherubini Requiem in C MinorBen RutjesNessuna valutazione finora

- Annexure I Project Details DateDocumento4 pagineAnnexure I Project Details DateAshish SinghaniaNessuna valutazione finora

- List of Every National School Walkout PDF LinksDocumento373 pagineList of Every National School Walkout PDF LinksStephanie Dube Dwilson100% (1)

- Eat Something DifferentDocumento3 pagineEat Something Differentsrajendr200100% (1)

- Consumer PresentationDocumento30 pagineConsumer PresentationShafiqur Rahman KhanNessuna valutazione finora

- Fabrication Daily Progress: No DescriptionDocumento4 pagineFabrication Daily Progress: No DescriptionAris PurniawanNessuna valutazione finora

- Sample Database of SQL in Mysql FormatDocumento7 pagineSample Database of SQL in Mysql FormatsakonokeNessuna valutazione finora

- Guide Rail Bracket AssemblyDocumento1 paginaGuide Rail Bracket AssemblyPrasanth VarrierNessuna valutazione finora

- The Latest Open Source Software Available and The Latest Development in IctDocumento10 pagineThe Latest Open Source Software Available and The Latest Development in IctShafirahFameiJZNessuna valutazione finora

- AOCS Ca 12-55 - 2009 - Phosphorus PDFDocumento2 pagineAOCS Ca 12-55 - 2009 - Phosphorus PDFGeorgianaNessuna valutazione finora

- Formula BookletDocumento2 pagineFormula BookletOm PatelNessuna valutazione finora

- Bylaws of A Texas CorporationDocumento34 pagineBylaws of A Texas CorporationDiego AntoliniNessuna valutazione finora

- Med Error PaperDocumento4 pagineMed Error Paperapi-314062228100% (1)

- HOWO SERVICE AND MAINTENANCE SCHEDULE SinotruckDocumento3 pagineHOWO SERVICE AND MAINTENANCE SCHEDULE SinotruckRPaivaNessuna valutazione finora

- Digital Economy 1Documento11 pagineDigital Economy 1Khizer SikanderNessuna valutazione finora