Potrebbero piacerti anche

- Past Papers - Partnership ChangesDocumento10 paginePast Papers - Partnership ChangesFarhan JehangirNessuna valutazione finora

- Partnership Changes... Goodwill and RevaluationDocumento5 paginePartnership Changes... Goodwill and Revaluationtafadzwa tandawaNessuna valutazione finora

- CAF 1 IA Autumn 2020Documento5 pagineCAF 1 IA Autumn 2020Qasim Hafeez KhokharNessuna valutazione finora

- Accounting: Quantitative Information Primarily Financial inDocumento19 pagineAccounting: Quantitative Information Primarily Financial inleeeydoNessuna valutazione finora

- ACW366 - Tutorial Exercises 4 PDFDocumento6 pagineACW366 - Tutorial Exercises 4 PDFMERINANessuna valutazione finora

- Cash Budgets Practice QuestionDocumento1 paginaCash Budgets Practice QuestionDenisa M. Todea50% (2)

- Financial Instruments (2021)Documento17 pagineFinancial Instruments (2021)Tawanda Tatenda Herbert100% (1)

- W7 Module 6 COMPARATIVE FINANCIAL STATEMENT ANALYSISDocumento8 pagineW7 Module 6 COMPARATIVE FINANCIAL STATEMENT ANALYSISDanica VetuzNessuna valutazione finora

- E1-4 Determine The Total Amount of Various Types of Costs: InstructionsDocumento7 pagineE1-4 Determine The Total Amount of Various Types of Costs: InstructionsNgọc KhánhNessuna valutazione finora

- Revision - Test - Paper - CAP - II - June - 2017 9Documento181 pagineRevision - Test - Paper - CAP - II - June - 2017 9Dipen AdhikariNessuna valutazione finora

- Revision Questions - 2 Statement of Cash Flows - SolutionDocumento7 pagineRevision Questions - 2 Statement of Cash Flows - SolutionNadjah JNessuna valutazione finora

- Balance SheetDocumento18 pagineBalance SheetAndriaNessuna valutazione finora

- Far Qualifying ExaminationDocumento30 pagineFar Qualifying ExaminationAlvin BaternaNessuna valutazione finora

- Revaluation-Accounting CompressDocumento13 pagineRevaluation-Accounting CompressEunice Buenaventura100% (1)

- Answers Biological AssetsDocumento4 pagineAnswers Biological AssetsJanella Gail ArenasNessuna valutazione finora

- Division of ProfitsDocumento55 pagineDivision of ProfitsMichole chin MallariNessuna valutazione finora

- Backflush Costing System and Activity Based Costing System With SolutionDocumento15 pagineBackflush Costing System and Activity Based Costing System With SolutionJhazreene ArnozaNessuna valutazione finora

- Q and A PartnershipDocumento9 pagineQ and A PartnershipFaker MejiaNessuna valutazione finora

- Activity 1.1 PDFDocumento2 pagineActivity 1.1 PDFDe Nev OelNessuna valutazione finora

- MCQDocumento3 pagineMCQPeng GuinNessuna valutazione finora

- Chapter 3-Consolidated Statement of Profit and LossDocumento11 pagineChapter 3-Consolidated Statement of Profit and LossSheikh Mass JahNessuna valutazione finora

- A1 Basic Financial Statement Analysis Q8Documento3 pagineA1 Basic Financial Statement Analysis Q8bernard cruzNessuna valutazione finora

- CVP VAnswer Practice QuestionsDocumento5 pagineCVP VAnswer Practice QuestionsAbhijit AshNessuna valutazione finora

- Mathematics Logic PremiseDocumento2 pagineMathematics Logic PremiseLuigi JalandoonNessuna valutazione finora

- 08-Rectification-Of-Errors Good OneDocumento54 pagine08-Rectification-Of-Errors Good OneAejaz MohamedNessuna valutazione finora

- Fully Prepared AccountsDocumento127 pagineFully Prepared AccountsAMIN BUHARI ABDUL KHADER0% (4)

- IAS 12 TaxDocumento12 pagineIAS 12 TaxHarsh KhandelwalNessuna valutazione finora

- Ia Shareholder's Equity Practice ProblemsDocumento5 pagineIa Shareholder's Equity Practice ProblemsMary Jescho Vidal AmpilNessuna valutazione finora

- Cost and Management Accounting: Paper 7Documento31 pagineCost and Management Accounting: Paper 7Atukwatse PamelaNessuna valutazione finora

- Gross Profit AnalysisDocumento5 pagineGross Profit AnalysisInayat Ur RehmanNessuna valutazione finora

- Partnership Liquidation: Problem MDocumento8 paginePartnership Liquidation: Problem MMiko ArniñoNessuna valutazione finora

- Retirement of A PartnerDocumento33 pagineRetirement of A PartnerKriti Shah100% (2)

- Final RequirementDocumento18 pagineFinal RequirementZandra GonzalesNessuna valutazione finora

- Leonardo Wagster Decided To Open Wagster's Window Washing On September 1, 2020. in September, The Following Transactions Took PlaceDocumento12 pagineLeonardo Wagster Decided To Open Wagster's Window Washing On September 1, 2020. in September, The Following Transactions Took PlaceJohnMurray111100% (1)

- First Partn - Answer 2Documento5 pagineFirst Partn - Answer 2Monique CabreraNessuna valutazione finora

- Multiple Choice Answers and Solutions: PAR Boogie BirdieDocumento19 pagineMultiple Choice Answers and Solutions: PAR Boogie BirdieNelia Mae S. VillenaNessuna valutazione finora

- Finals Unit 5 Exercise Short Run Decision MakingDocumento6 pagineFinals Unit 5 Exercise Short Run Decision MakingDia Mae Ablao GenerosoNessuna valutazione finora

- Prob 2Documento1 paginaProb 2Mitch Tokong MinglanaNessuna valutazione finora

- MSC F&A AFG 09101 Supplementary Examination 2023Documento9 pagineMSC F&A AFG 09101 Supplementary Examination 2023Sebastian MlingwaNessuna valutazione finora

- Ias 37 Provisions, Contingent Liabilities & Contingent AssetsDocumento12 pagineIas 37 Provisions, Contingent Liabilities & Contingent AssetsTawanda Tatenda HerbertNessuna valutazione finora

- Assignment 1 AFSDocumento14 pagineAssignment 1 AFSSimra SalmanNessuna valutazione finora

- Qa PartnershipDocumento9 pagineQa PartnershipFaker MejiaNessuna valutazione finora

- Case Study #3: Wake Up and Smell The Coffee!Documento4 pagineCase Study #3: Wake Up and Smell The Coffee!USD 654Nessuna valutazione finora

- This Study Resource Was: Problem Set 7 Budgeting Problem 1 (Garrison Et Al. v15 8-1)Documento8 pagineThis Study Resource Was: Problem Set 7 Budgeting Problem 1 (Garrison Et Al. v15 8-1)NCT100% (1)

- Exercises On Issue of Shares and DebenturesDocumento6 pagineExercises On Issue of Shares and Debenturesontykerls100% (1)

- PDF PDFDocumento7 paginePDF PDFMikey MadRatNessuna valutazione finora

- Multiple Choices - Quiz - Chapter 1-To-3Documento21 pagineMultiple Choices - Quiz - Chapter 1-To-3Ella SingcaNessuna valutazione finora

- More Practice Problems CH 1-5 EconomicsDocumento23 pagineMore Practice Problems CH 1-5 EconomicsAdam GillNessuna valutazione finora

- 05 - Chapter 5 - Partnership AccountsDocumento16 pagine05 - Chapter 5 - Partnership Accountszubairkhan_leo100% (15)

- Chapter 005 - Valuing Bonds: True / False QuestionsDocumento12 pagineChapter 005 - Valuing Bonds: True / False QuestionsLaraNessuna valutazione finora

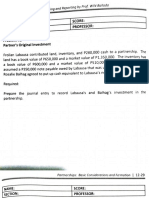

- Name:: Score: ProfessorDocumento6 pagineName:: Score: ProfessorkakaoNessuna valutazione finora

- G1 6.4 Partnership - Amalgamation and Business PurchaseDocumento15 pagineG1 6.4 Partnership - Amalgamation and Business Purchasesridhartks100% (2)

- Part IIDocumento58 paginePart IIhaaasaaNessuna valutazione finora

- 19696ipcc Acc Vol2 Chapter14Documento41 pagine19696ipcc Acc Vol2 Chapter14Shivam TripathiNessuna valutazione finora

- Additional Illustratiions 2Documento14 pagineAdditional Illustratiions 2Naman ChotiaNessuna valutazione finora

- Financial Accounting & Reporting Final Examination: Name: Date: Professor: Section: ScoreDocumento17 pagineFinancial Accounting & Reporting Final Examination: Name: Date: Professor: Section: ScoreMaryjoy NemenoNessuna valutazione finora

- Accounting For Treatment For MergerDocumento6 pagineAccounting For Treatment For Mergergoel76vishalNessuna valutazione finora

- Introduction To Partnership AccountsDocumento20 pagineIntroduction To Partnership Accountsanon_672065362100% (1)

- Reviewer in Partnership Corporation MycDocumento22 pagineReviewer in Partnership Corporation MycScwythle65% (20)

- G1 6.3 Partnership - DissolutionDocumento15 pagineG1 6.3 Partnership - Dissolutionsridhartks100% (2)

- Retainage Release Invoices in Oracle AP - ErpSchoolsDocumento9 pagineRetainage Release Invoices in Oracle AP - ErpSchoolsK.rajesh Kumar ReddyNessuna valutazione finora

- Harish NatarajanDocumento10 pagineHarish NatarajanbananiacorpNessuna valutazione finora

- StartUp India - Case AnalysisDocumento3 pagineStartUp India - Case AnalysisIrshad AzeezNessuna valutazione finora

- Break Even Point ExplanationDocumento2 pagineBreak Even Point ExplanationEdgar IbarraNessuna valutazione finora

- Cheque and Its TypesDocumento2 pagineCheque and Its Typesdevraj subediNessuna valutazione finora

- RWJ 08Documento38 pagineRWJ 08Kunal PuriNessuna valutazione finora

- PricelistDocumento3 paginePricelist4 fruit companyNessuna valutazione finora

- Jack Daniel'sDocumento17 pagineJack Daniel'sIon TarlevNessuna valutazione finora

- Spisak Parfema NEWDocumento1 paginaSpisak Parfema NEWDouglas CoxNessuna valutazione finora

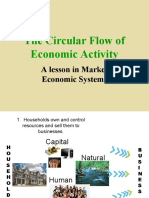

- Circular FlowDocumento21 pagineCircular FlowSheryl BorromeoNessuna valutazione finora

- Antwoordblad Instaptoets EngelsDocumento4 pagineAntwoordblad Instaptoets EngelskadpoortNessuna valutazione finora

- Putting English Unit14Documento13 paginePutting English Unit14Dung LeNessuna valutazione finora

- Corporate FinanceDocumento11 pagineCorporate Financemishu082002100% (2)

- Business Level StrategyDocumento28 pagineBusiness Level StrategyMohammad Raihanul HasanNessuna valutazione finora

- Gat PreparationDocumento21 pagineGat PreparationHAFIZ IMRAN AKHTERNessuna valutazione finora

- Powerpoint Lectures For Principles of Macroeconomics, 9E by Karl E. Case, Ray C. Fair & Sharon M. OsterDocumento24 paginePowerpoint Lectures For Principles of Macroeconomics, 9E by Karl E. Case, Ray C. Fair & Sharon M. OsterJiya Nitric AcidNessuna valutazione finora

- Tennis Ball Activity - Diminishing Returns - Notes - 3Documento1 paginaTennis Ball Activity - Diminishing Returns - Notes - 3Raghvi AryaNessuna valutazione finora

- PinoyDocumento5 paginePinoyLarete PaoloNessuna valutazione finora

- Concentration of SolutionsDocumento32 pagineConcentration of SolutionsRaja Mohan Gopalakrishnan100% (2)

- VisuSon - Business Stress TestingDocumento7 pagineVisuSon - Business Stress TestingAmira Nur Afiqah Agus SalimNessuna valutazione finora

- Akuntansi Keuangan Lanjutan 2Documento6 pagineAkuntansi Keuangan Lanjutan 2Marselinus Aditya Hartanto TjungadiNessuna valutazione finora

- Cash Flows From Operating ActivitiesDocumento5 pagineCash Flows From Operating ActivitiesIrfan MansoorNessuna valutazione finora

- Magazine Still Holds True With Its Mission Statement-Dedicated To The Growth of TheDocumento5 pagineMagazine Still Holds True With Its Mission Statement-Dedicated To The Growth of TheRush YuviencoNessuna valutazione finora

- Chief Executive Officer CPG in West Palm Beach FL Resume James MercerDocumento2 pagineChief Executive Officer CPG in West Palm Beach FL Resume James MercerJames MercerNessuna valutazione finora

- International Marketing - ChinaDocumento10 pagineInternational Marketing - ChinaNaijalegendNessuna valutazione finora

- Tourism PolicyDocumento6 pagineTourism Policylanoox0% (1)

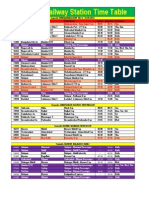

- Solapur Railway Station Time TableDocumento2 pagineSolapur Railway Station Time TableAndrea Lopez33% (3)

- 3.1.2 and 3.1.3.import - LC Open and Amend Karl Mayer - Nov.28.2014Documento8 pagine3.1.2 and 3.1.3.import - LC Open and Amend Karl Mayer - Nov.28.2014thanhtuan12Nessuna valutazione finora

- Respond To Business OpportunitiesDocumento21 pagineRespond To Business OpportunitiesRissabelle CoscaNessuna valutazione finora

- Key Points in Creation of Huf and Format of Deed For Creation of HufDocumento5 pagineKey Points in Creation of Huf and Format of Deed For Creation of HufGopalakrishna SrinivasanNessuna valutazione finora

- I Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Da EverandI Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Valutazione: 4.5 su 5 stelle4.5/5 (15)

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesDa EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesNessuna valutazione finora

- Getting to Yes: How to Negotiate Agreement Without Giving InDa EverandGetting to Yes: How to Negotiate Agreement Without Giving InValutazione: 4 su 5 stelle4/5 (652)

- The ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!Da EverandThe ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!Valutazione: 4.5 su 5 stelle4.5/5 (14)

- The Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindDa EverandThe Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindValutazione: 5 su 5 stelle5/5 (231)

- Start, Study and Pass The CPA Exam FAST - Proven 8 Step CPA Exam Study PlaybookDa EverandStart, Study and Pass The CPA Exam FAST - Proven 8 Step CPA Exam Study PlaybookValutazione: 5 su 5 stelle5/5 (4)

- Overcoming Underearning(TM): A Simple Guide to a Richer LifeDa EverandOvercoming Underearning(TM): A Simple Guide to a Richer LifeValutazione: 4 su 5 stelle4/5 (21)

- SAP Foreign Currency Revaluation: FAS 52 and GAAP RequirementsDa EverandSAP Foreign Currency Revaluation: FAS 52 and GAAP RequirementsNessuna valutazione finora

- The Big Four: The Curious Past and Perilous Future of the Global Accounting MonopolyDa EverandThe Big Four: The Curious Past and Perilous Future of the Global Accounting MonopolyNessuna valutazione finora

- The Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)Da EverandThe Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)Valutazione: 4 su 5 stelle4/5 (33)

- A Beginners Guide to QuickBooks Online 2023: A Step-by-Step Guide and Quick Reference for Small Business Owners, Churches, & Nonprofits to Track their Finances and Master QuickBooks OnlineDa EverandA Beginners Guide to QuickBooks Online 2023: A Step-by-Step Guide and Quick Reference for Small Business Owners, Churches, & Nonprofits to Track their Finances and Master QuickBooks OnlineNessuna valutazione finora

- How to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)Da EverandHow to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)Valutazione: 4.5 su 5 stelle4.5/5 (5)

- How to Measure Anything: Finding the Value of "Intangibles" in BusinessDa EverandHow to Measure Anything: Finding the Value of "Intangibles" in BusinessValutazione: 4.5 su 5 stelle4.5/5 (28)

- Beyond the E-Myth: The Evolution of an Enterprise: From a Company of One to a Company of 1,000!Da EverandBeyond the E-Myth: The Evolution of an Enterprise: From a Company of One to a Company of 1,000!Valutazione: 4.5 su 5 stelle4.5/5 (8)

- Ratio Analysis Fundamentals: How 17 Financial Ratios Can Allow You to Analyse Any Business on the PlanetDa EverandRatio Analysis Fundamentals: How 17 Financial Ratios Can Allow You to Analyse Any Business on the PlanetValutazione: 4.5 su 5 stelle4.5/5 (14)

- The Wall Street MBA, Third Edition: Your Personal Crash Course in Corporate FinanceDa EverandThe Wall Street MBA, Third Edition: Your Personal Crash Course in Corporate FinanceValutazione: 4 su 5 stelle4/5 (1)

- Accounting For Small Businesses QuickStart Guide: Understanding Accounting For Your Sole Proprietorship, Startup, & LLCDa EverandAccounting For Small Businesses QuickStart Guide: Understanding Accounting For Your Sole Proprietorship, Startup, & LLCValutazione: 5 su 5 stelle5/5 (1)

- Purchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsDa EverandPurchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsValutazione: 5 su 5 stelle5/5 (1)

- The Intelligent Investor, Rev. Ed: The Definitive Book on Value InvestingDa EverandThe Intelligent Investor, Rev. Ed: The Definitive Book on Value InvestingValutazione: 4.5 su 5 stelle4.5/5 (760)

- Contract Negotiation Handbook: Getting the Most Out of Commercial DealsDa EverandContract Negotiation Handbook: Getting the Most Out of Commercial DealsValutazione: 4.5 su 5 stelle4.5/5 (2)

- Your Amazing Itty Bitty(R) Personal Bookkeeping BookDa EverandYour Amazing Itty Bitty(R) Personal Bookkeeping BookNessuna valutazione finora

- Financial Accounting For Dummies: 2nd EditionDa EverandFinancial Accounting For Dummies: 2nd EditionValutazione: 5 su 5 stelle5/5 (10)

- Small Business: A Complete Guide to Accounting Principles, Bookkeeping Principles and Taxes for Small BusinessDa EverandSmall Business: A Complete Guide to Accounting Principles, Bookkeeping Principles and Taxes for Small BusinessNessuna valutazione finora