Potrebbero piacerti anche

- Project On MFDocumento43 pagineProject On MFAbhi Rajendraprasad100% (1)

- Foreign Exchange Market and Management of Foreign Exchange RiskDocumento56 pagineForeign Exchange Market and Management of Foreign Exchange RiskCedric ZvinavasheNessuna valutazione finora

- An Empirical Study of Factors Affecting Sales of Mutual Funds Companies in IndiaDocumento289 pagineAn Empirical Study of Factors Affecting Sales of Mutual Funds Companies in Indiashradha srivastavaNessuna valutazione finora

- StudyDocumento10 pagineStudyirahQNessuna valutazione finora

- Insurance - A Brief Overview: Chapter-1Documento58 pagineInsurance - A Brief Overview: Chapter-1Sreeja Sahadevan75% (4)

- Bhavesh Sawant Bhuvan DalviDocumento8 pagineBhavesh Sawant Bhuvan DalviBhuvan DalviNessuna valutazione finora

- Mutual FundDocumento12 pagineMutual FundyanaNessuna valutazione finora

- Performance Evaluation of Mutual Funds" Conducted at EMKAY GLOBAL FINANCIAL SERVICES PRIVATE LTDDocumento74 paginePerformance Evaluation of Mutual Funds" Conducted at EMKAY GLOBAL FINANCIAL SERVICES PRIVATE LTDPrashanth PBNessuna valutazione finora

- Mutual Fund Industry ProfileDocumento37 pagineMutual Fund Industry ProfileGokul KrishnanNessuna valutazione finora

- Comparative Study On Investment in Stocks, Mutual Funds and ULIPsDocumento66 pagineComparative Study On Investment in Stocks, Mutual Funds and ULIPsbistamasterNessuna valutazione finora

- Portfolio Management & Mutual FundsDocumento69 paginePortfolio Management & Mutual FundsakubadiaNessuna valutazione finora

- Mutual FundsDocumento16 pagineMutual Fundsvirenshah_9846Nessuna valutazione finora

- Mutual Fund ProjectDocumento35 pagineMutual Fund ProjectKripal SinghNessuna valutazione finora

- Mutual Fund Research PaperDocumento22 pagineMutual Fund Research Paperphani100% (1)

- MUTUAL FUNDS: A PROJECT REPORTDocumento88 pagineMUTUAL FUNDS: A PROJECT REPORTsun1986Nessuna valutazione finora

- Perception of People Towards Investment and VariousDocumento20 paginePerception of People Towards Investment and Variouscgs005Nessuna valutazione finora

- Project ReportDocumento57 pagineProject ReportPAWAR0015Nessuna valutazione finora

- Comparative Study On MF and FDDocumento6 pagineComparative Study On MF and FDamrita thakur100% (1)

- Uti - Investor's-Attitude-Towards-Uti-Mutual-FundsDocumento132 pagineUti - Investor's-Attitude-Towards-Uti-Mutual-Fundstrushna19Nessuna valutazione finora

- Comparing Equity Diversification and Sector Specific Mutual Fund SchemesDocumento67 pagineComparing Equity Diversification and Sector Specific Mutual Fund SchemesChethan.sNessuna valutazione finora

- A Project Report On Mutual Funds - UTIDocumento57 pagineA Project Report On Mutual Funds - UTIsidd0830Nessuna valutazione finora

- Study of Mutual FundDocumento106 pagineStudy of Mutual Fundmadhumaddy20096958Nessuna valutazione finora

- Understanding Investors and Equity MarketsDocumento81 pagineUnderstanding Investors and Equity Marketschaluvadiin100% (2)

- A Study On Impact of Financial Crisis On Indian Mutual FundsDocumento86 pagineA Study On Impact of Financial Crisis On Indian Mutual FundsTania MajumderNessuna valutazione finora

- Risk Return Analysis Analysis of Banking and FMCG StocksDocumento93 pagineRisk Return Analysis Analysis of Banking and FMCG StocksbhagathnagarNessuna valutazione finora

- A Project Report On Mutual Fund As An Investment Avenue at NJ India InvestDocumento16 pagineA Project Report On Mutual Fund As An Investment Avenue at NJ India InvestYogesh AroraNessuna valutazione finora

- Sip Mutual Fund Project On Edelweiss Broking LiitedDocumento44 pagineSip Mutual Fund Project On Edelweiss Broking LiitedHardik Agarwal100% (1)

- A Study On Investors Perception and Performance Towards Sbi Mutual FundDocumento51 pagineA Study On Investors Perception and Performance Towards Sbi Mutual FundHareesh HareeshNessuna valutazione finora

- Impact of FIIs on Indian Mutual FundsDocumento57 pagineImpact of FIIs on Indian Mutual FundsAadil KakarNessuna valutazione finora

- India Infoline (Awarness About The Mutual Fund)Documento95 pagineIndia Infoline (Awarness About The Mutual Fund)c_nptl50% (2)

- Security Analysis and Portfolio Management Project by TanveerDocumento77 pagineSecurity Analysis and Portfolio Management Project by TanveeradeenNessuna valutazione finora

- Invest in Mutual Funds for Long Term Growth (40 charactersDocumento20 pagineInvest in Mutual Funds for Long Term Growth (40 charactersAshish SrivastavaNessuna valutazione finora

- Portfolio Management and Investment DecisionsDocumento74 paginePortfolio Management and Investment DecisionsChillara Sai Kiran NaiduNessuna valutazione finora

- Parative Analysis On The Performance of Mutual Funds Between Private & PublicDocumento3 pagineParative Analysis On The Performance of Mutual Funds Between Private & PublicN.MUTHUKUMARANNessuna valutazione finora

- Risk and Return Analysis of Mutual FundDocumento12 pagineRisk and Return Analysis of Mutual FundMounika Ch100% (1)

- Mutual Fund InvstDocumento109 pagineMutual Fund Invstdhwaniganger24Nessuna valutazione finora

- SBI Mutual FundDocumento88 pagineSBI Mutual FundSubramanya Dg100% (1)

- Creating Awareness of Mutual FundsDocumento82 pagineCreating Awareness of Mutual FundsNavyaRaoNessuna valutazione finora

- Sandeep Blackbook PlagiarismDocumento50 pagineSandeep Blackbook PlagiarismRitvik SaxenaNessuna valutazione finora

- Payal DoDocumento82 paginePayal DoPayal PatelNessuna valutazione finora

- Executive Summary RaviDocumento2 pagineExecutive Summary RaviAditya Verma0% (1)

- Investment Decision Analysis at ICICI BankDocumento11 pagineInvestment Decision Analysis at ICICI BankKhaisarKhaisarNessuna valutazione finora

- Derivatives Final SIP Done 4597 PDFDocumento71 pagineDerivatives Final SIP Done 4597 PDFrdhk72100% (1)

- Risk & Return Analysis in Mutual Fund IndustryDocumento3 pagineRisk & Return Analysis in Mutual Fund IndustrySubrat Patnaik50% (2)

- Portfolio Management in Mutual FundsDocumento87 paginePortfolio Management in Mutual FundsDawarNessuna valutazione finora

- A Detailed Analysis of The Mutual Fund Industry & A Customer Perception StudyDocumento93 pagineA Detailed Analysis of The Mutual Fund Industry & A Customer Perception StudyNishant GuptaNessuna valutazione finora

- A Study On Risk and Return of Selected Mutual Funds Through Integrated Enterprises (India) LTDDocumento68 pagineA Study On Risk and Return of Selected Mutual Funds Through Integrated Enterprises (India) LTDMakkuMadhaiyanNessuna valutazione finora

- Project ReportDocumento53 pagineProject ReportAbhishek MishraNessuna valutazione finora

- Reliance Mutual FundDocumento32 pagineReliance Mutual Fundshiva_kuttimma100% (1)

- Religare Mutual Fund Project ReportDocumento44 pagineReligare Mutual Fund Project Reportsks4986100% (1)

- Chaitanya Chemicals - Capital Structure - 2018Documento82 pagineChaitanya Chemicals - Capital Structure - 2018maheshfbNessuna valutazione finora

- Executive SummaryDocumento38 pagineExecutive Summarypuneet_srs0% (1)

- INVESTOR S PERCEPTION TOWARDS MUTUAL FUNDS Project ReportDocumento53 pagineINVESTOR S PERCEPTION TOWARDS MUTUAL FUNDS Project ReportPallavi Pallu100% (1)

- A Study On Changing Investment Pattern Among Youth: G.H.Patel Post Graduate Institute of Business ManagementDocumento50 pagineA Study On Changing Investment Pattern Among Youth: G.H.Patel Post Graduate Institute of Business ManagementNaveen SahaNessuna valutazione finora

- Financial Stuff (More Complete)Documento24 pagineFinancial Stuff (More Complete)jeff_airwalker23Nessuna valutazione finora

- Creating and Monitoring A Diversified Stock PortfolioDocumento11 pagineCreating and Monitoring A Diversified Stock Portfolioసతీష్ మండవNessuna valutazione finora

- Investing in Mutual Funds: Factors to ConsiderDocumento4 pagineInvesting in Mutual Funds: Factors to ConsiderSatbir Ratti33% (3)

- Start With Mutual Funds: ProspectusDocumento4 pagineStart With Mutual Funds: ProspectusrajuttanNessuna valutazione finora

- 1.1 Introduction To The TopicDocumento92 pagine1.1 Introduction To The TopicNithya Devi ANessuna valutazione finora

- Los: 40 Portfolio Management: An Overview: A Portfolio Perspective On InvestingDocumento2 pagineLos: 40 Portfolio Management: An Overview: A Portfolio Perspective On InvestingArpit MaheshwariNessuna valutazione finora

- Advantages of Mutual FundsDocumento7 pagineAdvantages of Mutual FundsSiri PadmaNessuna valutazione finora

- Marketing of Agricultural Inputs: LPD RM Dec 2011Documento59 pagineMarketing of Agricultural Inputs: LPD RM Dec 2011Hector OliverNessuna valutazione finora

- Job AnalysisDocumento22 pagineJob AnalysisAnand MishraNessuna valutazione finora

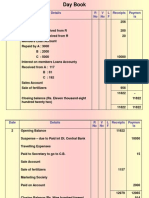

- Date Details R No V No L F Receipts Paymen TsDocumento8 pagineDate Details R No V No L F Receipts Paymen TsAnand MishraNessuna valutazione finora

- Accountancy: Accounting Is The Language of The BusinessDocumento41 pagineAccountancy: Accounting Is The Language of The BusinessAnand Mishra100% (1)

- Managing the Project Cycle Using the Integrated Approach and Logical FrameworkDocumento10 pagineManaging the Project Cycle Using the Integrated Approach and Logical FrameworkAnand MishraNessuna valutazione finora

- ITapplications AgriwatchDocumento77 pagineITapplications AgriwatchAnand MishraNessuna valutazione finora

- Ô " S#%& ' S$ ('S S: ! 0 S# Ss S1S$$$S Ss S#S S ! S# S $ss S Ss$Sss S$$ $S SsssDocumento7 pagineÔ " S#%& ' S$ ('S S: ! 0 S# Ss S1S$$$S Ss S#S S ! S# S $ss S Ss$Sss S$$ $S SsssAnand MishraNessuna valutazione finora

- Buzz Plan.... Potato ChipsDocumento11 pagineBuzz Plan.... Potato ChipsAnand MishraNessuna valutazione finora

- Lightstream FaqDocumento2 pagineLightstream Faqapi-256317677Nessuna valutazione finora

- Mrunal's Economy Win22 Updates For UPSC & Other Competitive ExamsDocumento21 pagineMrunal's Economy Win22 Updates For UPSC & Other Competitive ExamsTrial UserNessuna valutazione finora

- Stock ScreenerDocumento18 pagineStock ScreenerWajeeha IftikharNessuna valutazione finora

- Hafiz Salman Majeed: Composed & SolvedDocumento13 pagineHafiz Salman Majeed: Composed & SolvedFun NNessuna valutazione finora

- Letter of Authorisation (Agency) : Change of Servicing Agent (Private and Commercial Vehicles)Documento1 paginaLetter of Authorisation (Agency) : Change of Servicing Agent (Private and Commercial Vehicles)llllNessuna valutazione finora

- India Banking Industry ProfileDocumento23 pagineIndia Banking Industry ProfileBasappaSarkarNessuna valutazione finora

- Latihan Soal With DiscussionDocumento6 pagineLatihan Soal With DiscussionNicolas ErnestoNessuna valutazione finora

- 1709988038462kCf1zPm6V0XHmZJmDocumento6 pagine1709988038462kCf1zPm6V0XHmZJmAmar JainNessuna valutazione finora

- Financial FreedomDocumento4 pagineFinancial FreedomMarianne Jene DumagsaNessuna valutazione finora

- IFT 2016 2017 All Levels CFA Program Changes PDFDocumento5 pagineIFT 2016 2017 All Levels CFA Program Changes PDFTrisha SharmaNessuna valutazione finora

- Division of ProfitsDocumento55 pagineDivision of ProfitsMichole chin MallariNessuna valutazione finora

- To WHOME IT MAY CONCERNDocumento35 pagineTo WHOME IT MAY CONCERNAdnan Iftikhar100% (1)

- Principles of InsuranceDocumento4 paginePrinciples of InsuranceVandita KhudiaNessuna valutazione finora

- Class 1Documento40 pagineClass 1Jhon MontNessuna valutazione finora

- (21/04) Mscfe 660 Case Studies in Risk Management (C20-S1) Module 5: The 2008 Global Financial Crisis Practice Quiz M5 (Ungraded)Documento4 pagine(21/04) Mscfe 660 Case Studies in Risk Management (C20-S1) Module 5: The 2008 Global Financial Crisis Practice Quiz M5 (Ungraded)Abdullah AbdullahNessuna valutazione finora

- CTFP Unit 2 PGBPDocumento43 pagineCTFP Unit 2 PGBPKshitishNessuna valutazione finora

- Insurance Portfolio ReviewDocumento2 pagineInsurance Portfolio ReviewHetal ShahNessuna valutazione finora

- FINAL For Students Premium and Warranry Liability and LiabilitiesDocumento8 pagineFINAL For Students Premium and Warranry Liability and LiabilitiesHardly Dare GonzalesNessuna valutazione finora

- MLAMU Account Opening Form 1Documento4 pagineMLAMU Account Opening Form 1Tumwine Kahweza ProsperNessuna valutazione finora

- Unit-6:-Project FinanceDocumento2 pagineUnit-6:-Project FinanceShradha KapseNessuna valutazione finora

- Cost of Goods Sold Journal EntriesDocumento6 pagineCost of Goods Sold Journal EntriesJasmine P. Manlungat - EMERALDNessuna valutazione finora

- Assignment Classification Table: Topics Brief Exercises Exercises ProblemsDocumento95 pagineAssignment Classification Table: Topics Brief Exercises Exercises ProblemsMtl AndyNessuna valutazione finora

- Finding Fraud in The Loan DocumentsDocumento3 pagineFinding Fraud in The Loan Documentsrodclassteam100% (1)

- Finon - Week6 - Banking SystemDocumento30 pagineFinon - Week6 - Banking SystemivanNessuna valutazione finora

- Rural Marketing - InsuranceDocumento106 pagineRural Marketing - InsurancesinghinkingNessuna valutazione finora

- GO2 BankDocumento1 paginaGO2 Bank邱建华Nessuna valutazione finora

- Commercial and industrial property codesDocumento870 pagineCommercial and industrial property codesManual GuyNessuna valutazione finora

- Internship in Banking SIP ReportDocumento101 pagineInternship in Banking SIP ReportDaniel PedrosaNessuna valutazione finora