Potrebbero piacerti anche

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (74)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- In The Zone: EZ Walks Press Captures EventsDocumento12 pagineIn The Zone: EZ Walks Press Captures EventsEDC AdminNessuna valutazione finora

- EDA LawDocumento9 pagineEDA LawEDC AdminNessuna valutazione finora

- EDA Newsletter V1 I1 April 2008Documento8 pagineEDA Newsletter V1 I1 April 2008EDC AdminNessuna valutazione finora

- Reg Section 1.864-2Documento5 pagineReg Section 1.864-2EDC AdminNessuna valutazione finora

- Reg Section 1.864-7Documento6 pagineReg Section 1.864-7EDC AdminNessuna valutazione finora

- Reg Section 1.937-1Documento13 pagineReg Section 1.937-1EDC AdminNessuna valutazione finora

- Treas - Reg. Section 1.862-1Documento2 pagineTreas - Reg. Section 1.862-1EDC AdminNessuna valutazione finora

- IRC Section 934Documento2 pagineIRC Section 934EDC AdminNessuna valutazione finora

- Reg Section 1.861-4Documento13 pagineReg Section 1.861-4EDC AdminNessuna valutazione finora

- IRC Section 932Documento3 pagineIRC Section 932EDC AdminNessuna valutazione finora

- Code Section Summary Background Notes 26 U.S.C. 865 Regulations 1999 Tax Relief Extension ActDocumento4 pagineCode Section Summary Background Notes 26 U.S.C. 865 Regulations 1999 Tax Relief Extension ActEDC Admin100% (1)

- IRC Section 7701Documento18 pagineIRC Section 7701EDC AdminNessuna valutazione finora

- IRC Section 861Documento6 pagineIRC Section 861EDC AdminNessuna valutazione finora

- IRC Section 863Documento3 pagineIRC Section 863EDC AdminNessuna valutazione finora

- Go To Code Archive Directory For This JurisdictionDocumento88 pagineGo To Code Archive Directory For This JurisdictionEDC AdminNessuna valutazione finora

- Code Section Summary Background Notes 26 U.S.C. 862 RegulationsDocumento1 paginaCode Section Summary Background Notes 26 U.S.C. 862 RegulationsEDC AdminNessuna valutazione finora

- Afroza Sultana RumaDocumento1 paginaAfroza Sultana RumaImam HasanNessuna valutazione finora

- Tax Law AssignmentDocumento18 pagineTax Law AssignmentAmanNessuna valutazione finora

- Price - Chanel - Chalele TeamDocumento20 paginePrice - Chanel - Chalele TeamThanhHoàiNguyễnNessuna valutazione finora

- Week 22 - Home ProjectDocumento1 paginaWeek 22 - Home ProjectmisterreidNessuna valutazione finora

- The Study of Ratio AnalysisDocumento55 pagineThe Study of Ratio AnalysisVijay Tendolkar100% (2)

- Casal and Williams Equality CH 7 PDFDocumento23 pagineCasal and Williams Equality CH 7 PDFrodrigonakahara100% (2)

- Script AuditingReportDocumento3 pagineScript AuditingReportElaine Joyce GarciaNessuna valutazione finora

- Finance Management Notes MbaDocumento12 pagineFinance Management Notes MbaSandeep Kumar SahaNessuna valutazione finora

- Browerville Blade - 03/06/2014Documento12 pagineBrowerville Blade - 03/06/2014bladepublishingNessuna valutazione finora

- Chapter 12: Assessment of Various Entities: Section - A: Statutory UpdateDocumento49 pagineChapter 12: Assessment of Various Entities: Section - A: Statutory UpdateAmol TambeNessuna valutazione finora

- TAXDocumento2 pagineTAXJoshy BanbanNessuna valutazione finora

- METROPOLITAN WATERWORKS SEWERAGE Vs Quezon CityDocumento16 pagineMETROPOLITAN WATERWORKS SEWERAGE Vs Quezon CityJaysonNessuna valutazione finora

- Salary SlipDocumento1 paginaSalary SlipAnkit SinghNessuna valutazione finora

- ARROW Hospitality Consulting: Tax InvoiceDocumento1 paginaARROW Hospitality Consulting: Tax InvoiceShaShockNessuna valutazione finora

- Nigeria Property Tax in Federal Capital TerritoryDocumento3 pagineNigeria Property Tax in Federal Capital TerritoryMark allenNessuna valutazione finora

- Labor Code Book IVDocumento17 pagineLabor Code Book IVJestoni PabiaNessuna valutazione finora

- GST Book Bank AnswersDocumento10 pagineGST Book Bank AnswersAditya DasNessuna valutazione finora

- Assignment-Transfer PricingDocumento2 pagineAssignment-Transfer PricingMerliza Jusayan100% (1)

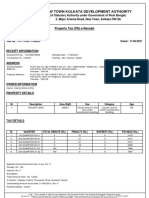

- New Town Kolkata Development Authority: Property Tax (PD) E-ReceiptDocumento2 pagineNew Town Kolkata Development Authority: Property Tax (PD) E-ReceiptSSK DEVELOPERSNessuna valutazione finora

- Rodwin - The French Health Care SystemDocumento7 pagineRodwin - The French Health Care SystemChris HarrisNessuna valutazione finora

- Solved MR and Mrs Janus Operate A Restaurant Business As ADocumento1 paginaSolved MR and Mrs Janus Operate A Restaurant Business As AAnbu jaromiaNessuna valutazione finora

- Intersectoral Linkages in Extractive Industries-The Case of Sao TomeDocumento51 pagineIntersectoral Linkages in Extractive Industries-The Case of Sao Tometsar_philip2010Nessuna valutazione finora

- Corporate Social Responsibility (CSR) As A Model of "Extended" Corporate Governance. An Explanation Based On The Economic Theories of Social Contract, Reputation and Reciprocal ConformismDocumento49 pagineCorporate Social Responsibility (CSR) As A Model of "Extended" Corporate Governance. An Explanation Based On The Economic Theories of Social Contract, Reputation and Reciprocal ConformismronaqvNessuna valutazione finora

- Taxation: GlossaryDocumento8 pagineTaxation: GlossarySara PattersonNessuna valutazione finora

- Industrial ParksDocumento30 pagineIndustrial ParksSubham DahalNessuna valutazione finora

- 2016 Merrill Taxes PDFDocumento8 pagine2016 Merrill Taxes PDFholymolyNessuna valutazione finora

- Spouses Pacquiao v. CTA-First Division (2016)Documento39 pagineSpouses Pacquiao v. CTA-First Division (2016)Meg ReyesNessuna valutazione finora

- Tax Q&A - Employment IncomeDocumento5 pagineTax Q&A - Employment IncomeHadifli100% (1)