Potrebbero piacerti anche

- 34th GST CouncilDocumento3 pagine34th GST CouncilYashwanth PrasadNessuna valutazione finora

- Basel Norms I, II and IIIDocumento30 pagineBasel Norms I, II and IIIYashwanth PrasadNessuna valutazione finora

- English TestDocumento23 pagineEnglish Testಸುಹಾಸ ಎNessuna valutazione finora

- Banking Products (R)Documento53 pagineBanking Products (R)Yashwanth PrasadNessuna valutazione finora

- HDFC BankDocumento32 pagineHDFC BankKapilMalhotraNessuna valutazione finora

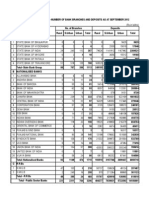

- 9.1-9.10-Banking Statistics and DisbursementDocumento19 pagine9.1-9.10-Banking Statistics and DisbursementYashwanth PrasadNessuna valutazione finora

- Export Finance1Documento29 pagineExport Finance1Yashwanth PrasadNessuna valutazione finora

- Follow The FootprintsDocumento7 pagineFollow The FootprintsYashwanth PrasadNessuna valutazione finora

- The Validity of Company Valuation Using Discounted Cash Flow MethodsDocumento25 pagineThe Validity of Company Valuation Using Discounted Cash Flow MethodsSoumya MishraNessuna valutazione finora

- Ram Kumar KakaniDocumento359 pagineRam Kumar KakaniYashwanth Prasad0% (1)

- ForfaitDocumento12 pagineForfaitgaurav11july1981Nessuna valutazione finora

- Bajaj Allianz Life InsuranceDocumento26 pagineBajaj Allianz Life InsuranceYashwanth PrasadNessuna valutazione finora

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (399)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (121)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- 164.100.129.99 Scientific2017 Payment ResponseDocumento1 pagina164.100.129.99 Scientific2017 Payment ResponseRavi RanjanNessuna valutazione finora

- ContinueDocumento2 pagineContinueAsjsjsjsNessuna valutazione finora

- Hsa Compliant Gap Plan: Level-Funded Gap Coverage For Groups With High Deductible Health Insurance PlansDocumento2 pagineHsa Compliant Gap Plan: Level-Funded Gap Coverage For Groups With High Deductible Health Insurance PlansamazonrecieptsNessuna valutazione finora

- Numerical SDocumento14 pagineNumerical SVIRAJ MODINessuna valutazione finora

- Issue ManagementDocumento21 pagineIssue ManagementArun DasNessuna valutazione finora

- Closed Medical Record ReviewDocumento6 pagineClosed Medical Record ReviewMuzna Iqbal50% (2)

- Battleface IPID GBPDocumento2 pagineBattleface IPID GBPmaria monsecaNessuna valutazione finora

- Place of SupplyDocumento6 paginePlace of SupplyMadhuram SharmaNessuna valutazione finora

- DISCOVERING Ethiopia - Tourism Sector GuideDocumento17 pagineDISCOVERING Ethiopia - Tourism Sector GuideMULUSEWNessuna valutazione finora

- Official Receipt: - 0000 Agent Code: Tin: Business Style: AmountDocumento1 paginaOfficial Receipt: - 0000 Agent Code: Tin: Business Style: AmountFamela Mae CagampangNessuna valutazione finora

- Guia Modem ZTE F670LDocumento5 pagineGuia Modem ZTE F670LCarlos PalmaNessuna valutazione finora

- Multiplexing and DemultiplexingDocumento48 pagineMultiplexing and DemultiplexingAkpevwe IsireNessuna valutazione finora

- Basic Instructions For A Bank Reconciliation Statement PDFDocumento4 pagineBasic Instructions For A Bank Reconciliation Statement PDFAman KodwaniNessuna valutazione finora

- Royal Colleges of Physicians of The United Kingdom: Form BDocumento4 pagineRoyal Colleges of Physicians of The United Kingdom: Form BBenjamin NelsonNessuna valutazione finora

- Rights & Responsibilities of An Insurance Policyholder And/or Prospective PolicyholderDocumento7 pagineRights & Responsibilities of An Insurance Policyholder And/or Prospective PolicyholderSharma KawalNessuna valutazione finora

- Quiz # 11 Bank Reconciliation, Proof of Cash & AR - FinalDocumento2 pagineQuiz # 11 Bank Reconciliation, Proof of Cash & AR - FinalDarren Jacob EspinaNessuna valutazione finora

- 5G - WikipediaDocumento7 pagine5G - WikipediaYu KiNessuna valutazione finora

- Banking Products and Services - Course PresentationDocumento171 pagineBanking Products and Services - Course Presentationnimitjain10Nessuna valutazione finora

- T Rec K.26 200804 I!!pdf eDocumento8 pagineT Rec K.26 200804 I!!pdf ejmrs7322Nessuna valutazione finora

- Frauds in InsuranceDocumento47 pagineFrauds in InsuranceVarsha Singh25% (4)

- LIC Profile 2013 PDFDocumento19 pagineLIC Profile 2013 PDFKokila RamarNessuna valutazione finora

- Tesda NC III Periodic UmakDocumento13 pagineTesda NC III Periodic UmakRinalyn AsuncionNessuna valutazione finora

- Dear Vivek Vinod Chaube: 13-Mar-2024 Generated By: 2669663 - LAL CHAND SHARMADocumento1 paginaDear Vivek Vinod Chaube: 13-Mar-2024 Generated By: 2669663 - LAL CHAND SHARMAchoube varunNessuna valutazione finora

- Week 9 PPT 9 - Statement of Cash FlowsDocumento23 pagineWeek 9 PPT 9 - Statement of Cash FlowsAmel Surya GumilangNessuna valutazione finora

- Margalla Services Officers Mess-169Documento1 paginaMargalla Services Officers Mess-169Wasi MohammadNessuna valutazione finora

- Apauline IciciDocumento41 pagineApauline Icicihalotog831Nessuna valutazione finora

- SUNDRAY AP-S500 Pro Wireless Access Point: Product OverviewDocumento9 pagineSUNDRAY AP-S500 Pro Wireless Access Point: Product OverviewIrvan SyahNessuna valutazione finora

- Bizmanualz Accounting Policies and Procedures SampleDocumento8 pagineBizmanualz Accounting Policies and Procedures SamplePaulo LindgrenNessuna valutazione finora

- Geeta Sy Fee ReceiptDocumento1 paginaGeeta Sy Fee Receiptrocky handsomeNessuna valutazione finora

- Kristine M. Walters ResumeDocumento4 pagineKristine M. Walters Resumesmnan5Nessuna valutazione finora