Potrebbero piacerti anche

- Chattel Mortgage, AffidavitsDocumento7 pagineChattel Mortgage, Affidavitscoldplay_addictNessuna valutazione finora

- Act 1508Documento7 pagineAct 1508Alyssa Fabella ReyesNessuna valutazione finora

- Chattel MortgageDocumento16 pagineChattel MortgageLe Obm SizzlingNessuna valutazione finora

- Chattel MortageDocumento11 pagineChattel MortageAmie Jane MirandaNessuna valutazione finora

- 7b CREDIT TRANS Chattel MortgagerDocumento29 pagine7b CREDIT TRANS Chattel MortgagerarielramadaNessuna valutazione finora

- Notes On Chattel Mortgage LawDocumento6 pagineNotes On Chattel Mortgage LawJaneNessuna valutazione finora

- Notes On Chattel Mortgage LawDocumento6 pagineNotes On Chattel Mortgage Lawjedyljamacauno100% (4)

- Guide to the Chattel Mortgage LawDocumento9 pagineGuide to the Chattel Mortgage Lawkazuke1103Nessuna valutazione finora

- Case: Filipinas Marble Corp. vs. Intermediate Appellate Court, 142 SCRA 180 (1986) .) andDocumento8 pagineCase: Filipinas Marble Corp. vs. Intermediate Appellate Court, 142 SCRA 180 (1986) .) andesmeralda de guzmanNessuna valutazione finora

- CHATTEL MORTGAGE (Articles 2140 To 2141)Documento7 pagineCHATTEL MORTGAGE (Articles 2140 To 2141)Beya AmaroNessuna valutazione finora

- Chattel Mortgage LawDocumento6 pagineChattel Mortgage LawAnonymous X5ud3UNessuna valutazione finora

- Manner of Recording Chattel MortgageDocumento14 pagineManner of Recording Chattel MortgageJuris PoetNessuna valutazione finora

- Chattel MortgageDocumento2 pagineChattel MortgageHyj Pestillos LascoNessuna valutazione finora

- Chattel MortgageDocumento13 pagineChattel MortgageEdward BatallerNessuna valutazione finora

- Law On Chattel MortgageDocumento17 pagineLaw On Chattel MortgageRojohn ValenzuelaNessuna valutazione finora

- A. Pactum Commisorium, Cite Specific Civil Code ProvisionDocumento4 pagineA. Pactum Commisorium, Cite Specific Civil Code ProvisionEmmanuel YrreverreNessuna valutazione finora

- Chattel Mortgage-Ppt - RFBT 3Documento22 pagineChattel Mortgage-Ppt - RFBT 316 Dela Cerna, RonaldNessuna valutazione finora

- The Chattel Mortgage Law GuideDocumento6 pagineThe Chattel Mortgage Law GuideArriane Hapon100% (1)

- Chattel Mortgage LawDocumento9 pagineChattel Mortgage LawJeffy EmanoNessuna valutazione finora

- Chattel Mortgage: What Is A Chattel?Documento8 pagineChattel Mortgage: What Is A Chattel?Erica Dela CruzNessuna valutazione finora

- Essential elements of chattel mortgages in the PhilippinesDocumento9 pagineEssential elements of chattel mortgages in the PhilippinesMingNessuna valutazione finora

- Chattel MortgageDocumento7 pagineChattel MortgageAya BeltranNessuna valutazione finora

- Oblicon Module 5Documento6 pagineOblicon Module 5Jenjen ArutaNessuna valutazione finora

- ObliCon FinalDocumento18 pagineObliCon Finalemdi19Nessuna valutazione finora

- Business LawDocumento114 pagineBusiness LawMira Kristel Caringal PasadasNessuna valutazione finora

- Sales CA5Documento12 pagineSales CA5Angel CabanNessuna valutazione finora

- The Recto LawDocumento12 pagineThe Recto LawBrian MannNessuna valutazione finora

- Credit TransactionsDocumento10 pagineCredit Transactionskero keropiNessuna valutazione finora

- Antichresis ReviewerDocumento6 pagineAntichresis Reviewersushisupergirl14100% (1)

- Title 6 - Law On SalesDocumento10 pagineTitle 6 - Law On SalesmrstudymodeNessuna valutazione finora

- CIV2 Tip SheetDocumento23 pagineCIV2 Tip Sheetdenbar15Nessuna valutazione finora

- Land Titles and Deeds NotesDocumento5 pagineLand Titles and Deeds NotesWillow SapphireNessuna valutazione finora

- Legal Aspects in Hospitality and Tourism ActivityDocumento11 pagineLegal Aspects in Hospitality and Tourism ActivityKrisha Mary CascolanNessuna valutazione finora

- Real Estate MortgageDocumento5 pagineReal Estate MortgageEbot Gempis100% (1)

- Notes in Questions and Answers Form On TDocumento8 pagineNotes in Questions and Answers Form On Tshailesh latkarNessuna valutazione finora

- Chapter VI Obli ConDocumento8 pagineChapter VI Obli ConderekNessuna valutazione finora

- Credit Cases - Rem, CHM, AchDocumento18 pagineCredit Cases - Rem, CHM, AchJose MasarateNessuna valutazione finora

- Pledge Real Estate Mortgage Chattel MortgageDocumento25 paginePledge Real Estate Mortgage Chattel MortgagePotie RhymeszNessuna valutazione finora

- REGULATORY FRAMEWORK FOR CREDIT TRANSACTIONSDocumento18 pagineREGULATORY FRAMEWORK FOR CREDIT TRANSACTIONSJames CantorneNessuna valutazione finora

- Understanding Real Estate MortgagesDocumento4 pagineUnderstanding Real Estate MortgagesPark Min YeonNessuna valutazione finora

- Maceda LawDocumento8 pagineMaceda LawJeffrey L. OntangcoNessuna valutazione finora

- Rights and Remedies in Property Installment SalesDocumento5 pagineRights and Remedies in Property Installment Saleslehsem20006985Nessuna valutazione finora

- GPG SOC BFR PhilippinesDocumento12 pagineGPG SOC BFR PhilippinesdtcbscribdNessuna valutazione finora

- Article 1381Documento19 pagineArticle 1381Name ToomNessuna valutazione finora

- Guide to Philippine Chattel Mortgage LawDocumento5 pagineGuide to Philippine Chattel Mortgage LawApril Roween AranzaNessuna valutazione finora

- Real Estate MortgageDocumento9 pagineReal Estate MortgageApril Roween AranzaNessuna valutazione finora

- Chattel MortgageDocumento9 pagineChattel MortgageMa. Louise Aviso0% (1)

- Chapter 7 - Extinguishment of SaleDocumento5 pagineChapter 7 - Extinguishment of SaleYounanymous DecisionNessuna valutazione finora

- Sales Case DigestsDocumento10 pagineSales Case DigestsJenine QuiambaoNessuna valutazione finora

- Filinvest Credit Corporation Vs CA 178 Scra 188Documento4 pagineFilinvest Credit Corporation Vs CA 178 Scra 188Jenine QuiambaoNessuna valutazione finora

- Ale Ept 2Documento12 pagineAle Ept 2Threes SeeNessuna valutazione finora

- Fort Bonifacio Development Corporation vs. Yllas Lending CorporationDocumento20 pagineFort Bonifacio Development Corporation vs. Yllas Lending CorporationAmerigo VespucciNessuna valutazione finora

- BANKING LAWS Additional Supreme Court Doctrines On Real Estate Mortgage 01Documento18 pagineBANKING LAWS Additional Supreme Court Doctrines On Real Estate Mortgage 01RaineNessuna valutazione finora

- Void ContractsDocumento13 pagineVoid ContractsDon YcayNessuna valutazione finora

- SalesDocumento31 pagineSalesDenise VillanuevaNessuna valutazione finora

- Simple Guide for Drafting of Civil Suits in IndiaDa EverandSimple Guide for Drafting of Civil Suits in IndiaValutazione: 4.5 su 5 stelle4.5/5 (4)

- Dishonour of Cheques in India: A Guide along with Model Drafts of Notices and ComplaintDa EverandDishonour of Cheques in India: A Guide along with Model Drafts of Notices and ComplaintValutazione: 4 su 5 stelle4/5 (1)

- Convention on International Interests in Mobile Equipment - Cape Town TreatyDa EverandConvention on International Interests in Mobile Equipment - Cape Town TreatyNessuna valutazione finora

- COUNTER-AFFIDAVIT Denies Tax Evasion AllegationsDocumento3 pagineCOUNTER-AFFIDAVIT Denies Tax Evasion AllegationsBethyl PorrasNessuna valutazione finora

- Presidential Decree NoDocumento2 paginePresidential Decree NoBethyl PorrasNessuna valutazione finora

- UST GN 2011 - Criminal Law PreliminariesDocumento11 pagineUST GN 2011 - Criminal Law PreliminariesGhostNessuna valutazione finora

- UST Golden Notes 2011 - SalesDocumento51 pagineUST Golden Notes 2011 - SalesBethyl Porras80% (5)

- CRIMINAL LAW 1 REVIEWER Padilla Cases and Notes Ortega NotesDocumento110 pagineCRIMINAL LAW 1 REVIEWER Padilla Cases and Notes Ortega NotesrockaholicnepsNessuna valutazione finora

- Protection of the Wounded, Sick and ShipwreckedDocumento40 pagineProtection of the Wounded, Sick and ShipwreckedBethyl Porras100% (1)

- Ateneo Central Bar Operations 2007 Civil Law Summer ReviewerDocumento15 pagineAteneo Central Bar Operations 2007 Civil Law Summer ReviewerMiGay Tan-Pelaez85% (13)

- Loc Gov ReviewerDocumento47 pagineLoc Gov ReviewerSuiNessuna valutazione finora

- Quotes From Well Known PeopleDocumento27 pagineQuotes From Well Known PeopleBethyl PorrasNessuna valutazione finora

- Provides Other Sercives Where Pharmaceutical Service Is RequiredDocumento5 pagineProvides Other Sercives Where Pharmaceutical Service Is RequiredZyra100% (1)

- MAS ClearSight Corporate ProfileDocumento36 pagineMAS ClearSight Corporate Profilemaycol romeoNessuna valutazione finora

- 2015-Dec Secret Service Report From The House Oversight CommitteeDocumento438 pagine2015-Dec Secret Service Report From The House Oversight CommitteeZenger NewsNessuna valutazione finora

- Effect of Non-Compliance with Formalities on Extra-Judicial SettlementsDocumento3 pagineEffect of Non-Compliance with Formalities on Extra-Judicial SettlementsBon HartNessuna valutazione finora

- Draft Contract To SMDCDocumento3 pagineDraft Contract To SMDCKrisna MacabentaNessuna valutazione finora

- Ever Electrical MFG V Ever Electrical UnionDocumento3 pagineEver Electrical MFG V Ever Electrical UnionKaren PascalNessuna valutazione finora

- Arco Metal Products Co., Inc., Et Al. vs. Samahan NG Mga Manggagawa Sa Arco Metal NAFLUDocumento1 paginaArco Metal Products Co., Inc., Et Al. vs. Samahan NG Mga Manggagawa Sa Arco Metal NAFLUAnn MarieNessuna valutazione finora

- Gold Torts Fall 2015Documento37 pagineGold Torts Fall 2015Amy PujaraNessuna valutazione finora

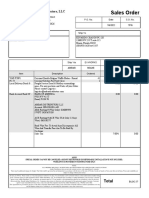

- Sales Order: Ambar Distributors, LLCDocumento1 paginaSales Order: Ambar Distributors, LLCEduardo ChaconNessuna valutazione finora

- Foz Vs PeopleDocumento4 pagineFoz Vs PeopleBeboy100% (1)

- Transpo UploadDocumento3 pagineTranspo UploadJuan Carlo CastanedaNessuna valutazione finora

- IPAF-MEWP Buying A Pre-OwnedDocumento2 pagineIPAF-MEWP Buying A Pre-OwnedLyle KorytarNessuna valutazione finora

- 1024.41 - Loss Mitigation Procedures.: Official InterpretationDocumento12 pagine1024.41 - Loss Mitigation Procedures.: Official InterpretationJohn LongNessuna valutazione finora

- Picart v. Smith (CD)Documento1 paginaPicart v. Smith (CD)christine jimenezNessuna valutazione finora

- GO (P) No 213-2015-Fin Dated 05-06-2015Documento3 pagineGO (P) No 213-2015-Fin Dated 05-06-2015sunil777tvpmNessuna valutazione finora

- The Commission On AuditDocumento5 pagineThe Commission On AuditJunDagz100% (1)

- The West Bengal Apartment Ownership Act, 1972Documento6 pagineThe West Bengal Apartment Ownership Act, 1972Debanjan SettNessuna valutazione finora

- Northwest Airlines v. Chiong-Case DigestDocumento2 pagineNorthwest Airlines v. Chiong-Case DigestLourdes LescanoNessuna valutazione finora

- What Is The Difference Between Legal Terms Appeal and Revision - Tilak MargDocumento3 pagineWhat Is The Difference Between Legal Terms Appeal and Revision - Tilak MarggauravNessuna valutazione finora

- Freecia Delhi GSTDocumento3 pagineFreecia Delhi GSTBlinc MediaNessuna valutazione finora

- Essential Religious Practices - Indian Constitutional Law and PhilosophyDocumento33 pagineEssential Religious Practices - Indian Constitutional Law and PhilosophyJajju RaoNessuna valutazione finora

- Step by Step Registration Procedure For Yatra - 2021Documento9 pagineStep by Step Registration Procedure For Yatra - 2021amareshscribdNessuna valutazione finora

- Legal Opinion Case No.112 Legal Expert: Wachira Maina National Lawyer: John B. KimwanganaDocumento21 pagineLegal Opinion Case No.112 Legal Expert: Wachira Maina National Lawyer: John B. Kimwanganajonas msigalaNessuna valutazione finora

- Answer With CounterclaimDocumento8 pagineAnswer With CounterclaimChris MortelNessuna valutazione finora

- 6 Joy A Gimeno Complainant Vs Atty Paul Centillas Zaide Respondent PDFDocumento3 pagine6 Joy A Gimeno Complainant Vs Atty Paul Centillas Zaide Respondent PDFPatricia Ann Erika TorrefielNessuna valutazione finora

- Compensation Dispute at Western Institute of TechnologyDocumento5 pagineCompensation Dispute at Western Institute of TechnologyVINCENTREY BERNARDONessuna valutazione finora

- The Dogmatic Structure of Criminal Liability in The General Part of The Draft Israeli Penal Code - A Comparison With German Law - Claus RoxinDocumento23 pagineThe Dogmatic Structure of Criminal Liability in The General Part of The Draft Israeli Penal Code - A Comparison With German Law - Claus RoxinivanpfNessuna valutazione finora

- Adidas v. Sears Trademark Complaint Stripes PDFDocumento21 pagineAdidas v. Sears Trademark Complaint Stripes PDFMark JaffeNessuna valutazione finora

- QCS 2010 Section 19 Part 1 General Plumbing RequirementsDocumento5 pagineQCS 2010 Section 19 Part 1 General Plumbing Requirementsbryanpastor106Nessuna valutazione finora

- Servsafe AlcoholDocumento1 paginaServsafe Alcoholapi-546481769Nessuna valutazione finora