Potrebbero piacerti anche

- Summary of Heather Brilliant & Elizabeth Collins's Why Moats MatterDa EverandSummary of Heather Brilliant & Elizabeth Collins's Why Moats MatterNessuna valutazione finora

- Cost & Managerial Accounting II EssentialsDa EverandCost & Managerial Accounting II EssentialsValutazione: 4 su 5 stelle4/5 (1)

- KFC Mission and ObjectivesDocumento30 pagineKFC Mission and ObjectivesSmriti ThapaNessuna valutazione finora

- BarrierDocumento5 pagineBarrierMa Jean Baluyo CastanedaNessuna valutazione finora

- Dwnload Full Corporate Finance The Core 4th Edition Berk Solutions Manual PDFDocumento36 pagineDwnload Full Corporate Finance The Core 4th Edition Berk Solutions Manual PDFdesidapawangl100% (16)

- KFCDocumento8 pagineKFCsadaffadasNessuna valutazione finora

- Green Zebra Finance Case StudyDocumento23 pagineGreen Zebra Finance Case StudyJessie Franz100% (10)

- Revised HD Equity Research ReportDocumento18 pagineRevised HD Equity Research Reportapi-312977476Nessuna valutazione finora

- Dwnload Full Corporate Finance 3rd Edition Berk Solutions Manual PDFDocumento26 pagineDwnload Full Corporate Finance 3rd Edition Berk Solutions Manual PDFlief.tanrec.culjd100% (10)

- Full Download Corporate Finance 3rd Edition Berk Solutions ManualDocumento35 pagineFull Download Corporate Finance 3rd Edition Berk Solutions Manualetalibelmi2100% (24)

- Solutions Manual To Accompany Corporate Finance The Core 2nd Edition 9780132153683Documento38 pagineSolutions Manual To Accompany Corporate Finance The Core 2nd Edition 9780132153683verawarnerq5cl100% (13)

- Solutions Manual To Accompany Corporate Finance The Core 2nd Edition 9780132153683Documento38 pagineSolutions Manual To Accompany Corporate Finance The Core 2nd Edition 9780132153683auntyprosperim1ru100% (15)

- Part 1: Multiple Choice 2 Points Each /140 Points 5 Points Deduction For Every 5 Items Answered IncorectlyDocumento22 paginePart 1: Multiple Choice 2 Points Each /140 Points 5 Points Deduction For Every 5 Items Answered IncorectlyDanna Karen MallariNessuna valutazione finora

- Full Download Corporate Finance The Core 3rd Edition Berk Solutions ManualDocumento35 pagineFull Download Corporate Finance The Core 3rd Edition Berk Solutions Manualslodgeghidinc100% (32)

- Dwnload Full Corporate Finance The Core 3rd Edition Berk Solutions Manual PDFDocumento22 pagineDwnload Full Corporate Finance The Core 3rd Edition Berk Solutions Manual PDFdesidapawangl100% (14)

- Management Accounting p2Documento26 pagineManagement Accounting p2Abegail DazoNessuna valutazione finora

- Solutions Manual Fundamentals of Corporate Finance (Asia Global EditionDocumento15 pagineSolutions Manual Fundamentals of Corporate Finance (Asia Global EditionKinglam Tse100% (1)

- CPK CaseDocumento12 pagineCPK Casejohncaleb100% (5)

- JollibeeDocumento12 pagineJollibeePankaj Sahu67% (3)

- Financial ManagementDocumento9 pagineFinancial ManagementRabbaniya Aisyah Firdauzy100% (1)

- Chapter 3 Solution ManualDocumento14 pagineChapter 3 Solution ManualAhmed FathelbabNessuna valutazione finora

- Fae3e SM ch04 060914Documento23 pagineFae3e SM ch04 060914JarkeeNessuna valutazione finora

- ISP583 Assesment 2 - Individual AssignmentDocumento14 pagineISP583 Assesment 2 - Individual AssignmentBella LeeNessuna valutazione finora

- GCC 2021 Investor Presentation 1Documento32 pagineGCC 2021 Investor Presentation 1artsan3Nessuna valutazione finora

- Auction of Burger King ADocumento6 pagineAuction of Burger King ASanjeet Walia0% (2)

- IIM RANCHI Nestle and Alcon Mergers, Acquisitions and Corporate RestructuringDocumento9 pagineIIM RANCHI Nestle and Alcon Mergers, Acquisitions and Corporate RestructuringAnkur Saurabh100% (2)

- What Are The Advantages and Disadvantages of GoingDocumento2 pagineWhat Are The Advantages and Disadvantages of GoingGenevieve AbuyonNessuna valutazione finora

- Mergers and AcquistionsDocumento29 pagineMergers and AcquistionsAli HussainNessuna valutazione finora

- Optimize capital budgeting decisions with NPV analysisDocumento15 pagineOptimize capital budgeting decisions with NPV analysisBrenda JohnsonNessuna valutazione finora

- General Mills' Acquisition of PillsburyDocumento14 pagineGeneral Mills' Acquisition of Pillsburyswapnil tyagiNessuna valutazione finora

- Chapter One: Introducing The Firm and Its Goals: QuestionsDocumento4 pagineChapter One: Introducing The Firm and Its Goals: QuestionsRavineahNessuna valutazione finora

- 3 Case Study Brunswick Distribution IncDocumento18 pagine3 Case Study Brunswick Distribution Incapi-313247205100% (1)

- Netflix Equity Debt Convertible Investment Banking Pitch BookDocumento15 pagineNetflix Equity Debt Convertible Investment Banking Pitch BookphuNessuna valutazione finora

- COBFSDS - Group 1 - Jollibee Case StudyDocumento7 pagineCOBFSDS - Group 1 - Jollibee Case Studylyniel siclotNessuna valutazione finora

- Dokumen - Tips CPK CaseDocumento11 pagineDokumen - Tips CPK CaseHarke Revo Leonard PoliiNessuna valutazione finora

- Fundamental Financial Analysis and ReportingDocumento6 pagineFundamental Financial Analysis and Reportinggilli1trNessuna valutazione finora

- Exhibit 4-5 Chan Audio Company: Current RatioDocumento35 pagineExhibit 4-5 Chan Audio Company: Current Ratiofokica840% (1)

- Unit 33 - Small Business EnterpriseDocumento14 pagineUnit 33 - Small Business EnterpriseNayeem H Khan94% (16)

- Financial Analysis and Valuation PICAVET ValentinDocumento26 pagineFinancial Analysis and Valuation PICAVET ValentinValentin PicavetNessuna valutazione finora

- Analysis of Financial Statements 1-10-19Documento28 pagineAnalysis of Financial Statements 1-10-19Shehzad QureshiNessuna valutazione finora

- Jollibee Case - Global StrategyDocumento27 pagineJollibee Case - Global StrategyJedidiah Danae AlvarezNessuna valutazione finora

- Dominos PizzaDocumento32 pagineDominos Pizzaapi-555390406Nessuna valutazione finora

- Financial Engineering Playbook Explains Value Creation TechniquesDocumento18 pagineFinancial Engineering Playbook Explains Value Creation TechniquesAyush AggarwalNessuna valutazione finora

- Resource ArchiveDocumento109 pagineResource ArchivemshadzNessuna valutazione finora

- Jefferies Presentation 06-24-2015Documento28 pagineJefferies Presentation 06-24-2015Ankur MittalNessuna valutazione finora

- BBBY Case ExerciseDocumento7 pagineBBBY Case ExerciseSue McGinnisNessuna valutazione finora

- Case Analysis Kuok 5-2Documento28 pagineCase Analysis Kuok 5-2Levi Lazareno Eugenio89% (9)

- Leveraged Buyouts Explained: Types, Process and ExamplesDocumento24 pagineLeveraged Buyouts Explained: Types, Process and ExamplesNIDHI SAROANessuna valutazione finora

- Credit Analysis and Commercial Lending: November 8, 2011, DUFEDocumento11 pagineCredit Analysis and Commercial Lending: November 8, 2011, DUFEHạnh LêNessuna valutazione finora

- Coors SolutionDocumento4 pagineCoors Solutiongoratim100% (1)

- Questions For Critical Thinking 1Documento6 pagineQuestions For Critical Thinking 1chilltime100% (2)

- McDonalds Competitive Analysis PresentationDocumento58 pagineMcDonalds Competitive Analysis PresentationTalha Muhammad100% (1)

- Greenwald Class Notes 5 - Liz Claiborne & Valuing GrowthDocumento17 pagineGreenwald Class Notes 5 - Liz Claiborne & Valuing GrowthJohn Aldridge Chew100% (2)

- Chap 011Documento21 pagineChap 011kianhuei50% (2)

- Target Case GuidelinesDocumento2 pagineTarget Case Guidelinesdktravels85Nessuna valutazione finora

- Linear Technology Dividend Policy and Shareholder ValueDocumento4 pagineLinear Technology Dividend Policy and Shareholder ValueAmrinder SinghNessuna valutazione finora

- HR Om11 Ism ch02Documento7 pagineHR Om11 Ism ch02143mc14Nessuna valutazione finora

- The Well-Timed Strategy (Review and Analysis of Navarro's Book)Da EverandThe Well-Timed Strategy (Review and Analysis of Navarro's Book)Nessuna valutazione finora

- Lean Distribution: Applying Lean Manufacturing to Distribution, Logistics, and Supply ChainDa EverandLean Distribution: Applying Lean Manufacturing to Distribution, Logistics, and Supply ChainValutazione: 2.5 su 5 stelle2.5/5 (2)

- Venture Capital Valuation, + Website: Case Studies and MethodologyDa EverandVenture Capital Valuation, + Website: Case Studies and MethodologyNessuna valutazione finora

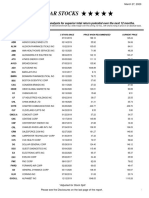

- Five Star StocksDocumento5 pagineFive Star StocksJeff SturgeonNessuna valutazione finora

- Chapter-1-Marketing-ChannelDocumento43 pagineChapter-1-Marketing-ChannelSrushti GadgeNessuna valutazione finora

- Cost Management Processes and TechniquesDocumento16 pagineCost Management Processes and Techniquespriyanshu shrivastavaNessuna valutazione finora

- MCQs - Secondary MarketsDocumento8 pagineMCQs - Secondary Marketskazi A.R RafiNessuna valutazione finora

- RBI Master Circular on Risk Management and Inter-Bank DealingsDocumento95 pagineRBI Master Circular on Risk Management and Inter-Bank DealingsBathina Srinivasa RaoNessuna valutazione finora

- Bank and NBFC - MehalDocumento38 pagineBank and NBFC - Mehalsushrut pawaskarNessuna valutazione finora

- World Co. Supply Chain Management AssignmentDocumento1 paginaWorld Co. Supply Chain Management AssignmentmirrorNessuna valutazione finora

- Solved Question Rhodes CorporationDocumento4 pagineSolved Question Rhodes CorporationBilalTariqNessuna valutazione finora

- Adjusted Present ValueDocumento14 pagineAdjusted Present ValueGoGoJoJo100% (1)

- Capital Market InstrumentsDocumento33 pagineCapital Market InstrumentsMayankTayal100% (1)

- 1033. ტურიზმის-მარკეტინგი-სოფო-თევდორაძეDocumento120 pagine1033. ტურიზმის-მარკეტინგი-სოფო-თევდორაძეAnton SinatashviliNessuna valutazione finora

- FD Course OutlineDocumento8 pagineFD Course OutlineSudip ThakurNessuna valutazione finora

- Paper - Iii Commerce: Note: Attempt All The Questions. Each Question Carries Two (2) MarksDocumento26 paginePaper - Iii Commerce: Note: Attempt All The Questions. Each Question Carries Two (2) MarksashaNessuna valutazione finora

- Hotel Ms DiantiDocumento2 pagineHotel Ms DiantiUsman BisnisNessuna valutazione finora

- Supply Chain Management PPT Final EditedDocumento17 pagineSupply Chain Management PPT Final Editedimran khanNessuna valutazione finora

- Kieso17e ch13 Solutions ManualDocumento89 pagineKieso17e ch13 Solutions ManualMoheeb HaddadNessuna valutazione finora

- Ramo 1-2000Documento526 pagineRamo 1-2000Mary graceNessuna valutazione finora

- Accounting Terminology GuideDocumento125 pagineAccounting Terminology GuideRam Cherry VMNessuna valutazione finora

- Valuation of The Deal Between Vedanta and CairnDocumento8 pagineValuation of The Deal Between Vedanta and Cairndnss_007Nessuna valutazione finora

- Chapter 04 Test Bank - Static - Version1Documento45 pagineChapter 04 Test Bank - Static - Version1mahasalehl200Nessuna valutazione finora

- Findings: Mutual FundDocumento4 pagineFindings: Mutual FundAbdulRahman ElhamNessuna valutazione finora

- Corporate Level StrategyDocumento33 pagineCorporate Level StrategyDave NamakhwaNessuna valutazione finora

- Guide To Original Issue Discount (OID) Instruments: Publication 1212Documento17 pagineGuide To Original Issue Discount (OID) Instruments: Publication 1212ChaseF31ckzwhrNessuna valutazione finora

- Business Combination - TheoriesDocumento11 pagineBusiness Combination - TheoriesMILLARE, Teddy Glo B.Nessuna valutazione finora

- Module 4 Key Vocabulary - English For Business and Entrepreneurship Summer 2023Documento7 pagineModule 4 Key Vocabulary - English For Business and Entrepreneurship Summer 2023Yamir VelazcoNessuna valutazione finora

- Week 4 Topic 1 Aqad and Sources of FundsDocumento41 pagineWeek 4 Topic 1 Aqad and Sources of Funds2 Ashlih Al TsabatNessuna valutazione finora

- Igcse Business Studies Workbook AnswersDocumento51 pagineIgcse Business Studies Workbook AnswersMateo VegnaduzziNessuna valutazione finora

- Mergers & Acquisitions: Aldovino, Hansley Eud, Rizza Mae Magana, Geselle Rodil, Via NicoleDocumento27 pagineMergers & Acquisitions: Aldovino, Hansley Eud, Rizza Mae Magana, Geselle Rodil, Via NicoleRizza Mae EudNessuna valutazione finora

- Five Keys To Investing SuccessDocumento12 pagineFive Keys To Investing Successr.jeyashankar9550Nessuna valutazione finora

- Examination: Subject ST7 - General Insurance: Reserving and Capital Modelling Specialist TechnicalDocumento5 pagineExamination: Subject ST7 - General Insurance: Reserving and Capital Modelling Specialist Technicaldickson phiriNessuna valutazione finora