Potrebbero piacerti anche

- Reichard MaschinenDocumento23 pagineReichard MaschinenAliefiah AZNessuna valutazione finora

- This Study Resource Was: Teaching NoteDocumento8 pagineThis Study Resource Was: Teaching NoteSuci NurlaeliNessuna valutazione finora

- Case ReichardDocumento23 pagineCase ReichardDesiSelviaNessuna valutazione finora

- Reichard Maschinen, GMBHDocumento4 pagineReichard Maschinen, GMBHJeevesNessuna valutazione finora

- Reichard QDocumento4 pagineReichard QN ParamitaNessuna valutazione finora

- Precision WorldwideDocumento5 paginePrecision WorldwideKing PuentespinaNessuna valutazione finora

- Precision WorldwideDocumento9 paginePrecision WorldwidePedro José ZapataNessuna valutazione finora

- Group 6 - Baldwin Bicycle (Final)Documento12 pagineGroup 6 - Baldwin Bicycle (Final)Sarjeet Kaushik100% (1)

- EC2101 Practice Problems 8 SolutionDocumento3 pagineEC2101 Practice Problems 8 Solutiongravity_coreNessuna valutazione finora

- Case Analysis I American Chemical CorporationDocumento13 pagineCase Analysis I American Chemical CorporationamuakaNessuna valutazione finora

- Worldwide Paper Company: Case Solution Company BackgroundDocumento4 pagineWorldwide Paper Company: Case Solution Company BackgroundJauhari WicaksonoNessuna valutazione finora

- A Case Analysis: Baldwin Bicycle CompanyDocumento12 pagineA Case Analysis: Baldwin Bicycle CompanySamrat KaushikNessuna valutazione finora

- Sol Wellington Chemicals DivisionDocumento3 pagineSol Wellington Chemicals DivisionRahul Goyal100% (1)

- Buckeye Bank CaseDocumento7 pagineBuckeye Bank CasePulkit Mathur0% (2)

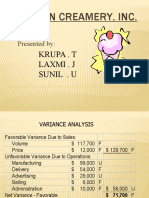

- Boston CreameryDocumento11 pagineBoston CreameryJelline Gaza100% (3)

- Baldwin Bicycle CompanyDocumento5 pagineBaldwin Bicycle CompanyPremal Gangar0% (1)

- Case 3 - Ocean Carriers Case PreparationDocumento1 paginaCase 3 - Ocean Carriers Case PreparationinsanomonkeyNessuna valutazione finora

- Boston Creamery CaseDocumento9 pagineBoston Creamery Caselion_heart3001100% (1)

- Ectn - XLS: InstructorDocumento12 pagineEctn - XLS: Instructorcamr2015100% (1)

- MANAC II - Morrissey Forgings CaseDocumento8 pagineMANAC II - Morrissey Forgings CaseKaran Oberoi100% (1)

- Group 7 - Morrissey ForgingsDocumento10 pagineGroup 7 - Morrissey ForgingsVishal AgarwalNessuna valutazione finora

- BALDWIN Case BarnaliDocumento39 pagineBALDWIN Case BarnaliVinay PottiNessuna valutazione finora

- Acova RadiateursDocumento10 pagineAcova RadiateursAnandNessuna valutazione finora

- Precision Worldwide, Inc.Documento3 paginePrecision Worldwide, Inc.karan_w3Nessuna valutazione finora

- Skyview ManorDocumento8 pagineSkyview ManorPhuong Bogrand100% (2)

- Tashtego SolutionDocumento8 pagineTashtego Solutionsathyanl90Nessuna valutazione finora

- Valuing ProjectsDocumento5 pagineValuing ProjectsAjay SinghNessuna valutazione finora

- Sealed Air Corporation's Leveraged RecapitalizationDocumento7 pagineSealed Air Corporation's Leveraged RecapitalizationKumarNessuna valutazione finora

- O.M Scott and Sons Case SummaryDocumento2 pagineO.M Scott and Sons Case SummarySUSHMITA SHUBHAMNessuna valutazione finora

- Tijuana Bronze MachiningDocumento19 pagineTijuana Bronze MachiningHari Haran43% (7)

- Baldwin Bicycle Company - Final Assignment - Group F - 20210728Documento4 pagineBaldwin Bicycle Company - Final Assignment - Group F - 20210728ApoorvaNessuna valutazione finora

- Unitron CorporationDocumento7 pagineUnitron CorporationERika PratiwiNessuna valutazione finora

- BSB Vs Sky TelevisionDocumento4 pagineBSB Vs Sky TelevisionPrabir AcharyaNessuna valutazione finora

- Baldwin Bicycle Company - Group8Documento8 pagineBaldwin Bicycle Company - Group8Satyendra ShuklaNessuna valutazione finora

- Lockheed Tristar ProjectDocumento1 paginaLockheed Tristar ProjectDurgaprasad VelamalaNessuna valutazione finora

- TashtegoDocumento5 pagineTashtegoMike PermataNessuna valutazione finora

- Case 5Documento12 pagineCase 5JIAXUAN WANGNessuna valutazione finora

- Baldwin Bicycle CaseDocumento10 pagineBaldwin Bicycle CaseAli Zaigham AghaNessuna valutazione finora

- Case 4 - Victoria ChemicalsDocumento18 pagineCase 4 - Victoria ChemicalsYale Brendan CatabayNessuna valutazione finora

- Sun Brewing Case ExhibitsDocumento26 pagineSun Brewing Case ExhibitsShshankNessuna valutazione finora

- Hampton Machine Tool CompanyDocumento6 pagineHampton Machine Tool CompanyClaudia Torres50% (2)

- Case Ocean CarriersDocumento2 pagineCase Ocean CarriersMorsal SarwarzadehNessuna valutazione finora

- Cadillac Cody CaseDocumento13 pagineCadillac Cody CaseKiran CheriyanNessuna valutazione finora

- Case SolutionDocumento20 pagineCase SolutionKhurram Sadiq (Father Name:Muhammad Sadiq)Nessuna valutazione finora

- EX 1 - WilkersonDocumento8 pagineEX 1 - WilkersonDror PazNessuna valutazione finora

- Dakota Office ProductsDocumento11 pagineDakota Office ProductsShibani Shankar RayNessuna valutazione finora

- Merrimack Tractors and MowersDocumento10 pagineMerrimack Tractors and MowersAtul Bhatia0% (1)

- UnitronDocumento9 pagineUnitronIvan Naufal PriadyNessuna valutazione finora

- Reichard Maschinen, GMBHDocumento23 pagineReichard Maschinen, GMBHSasisomWilaiwanNessuna valutazione finora

- Industrial Grinders NVDocumento6 pagineIndustrial Grinders NVCarrie Stevens100% (1)

- Industrial Grinders N VDocumento9 pagineIndustrial Grinders N Vapi-250891173100% (3)

- Industrial Grinders N VDocumento9 pagineIndustrial Grinders N VJuan Manuel RamirezNessuna valutazione finora

- Reichard Maschinen, GMBHDocumento4 pagineReichard Maschinen, GMBHSasisomWilaiwanNessuna valutazione finora

- Case Study-Precision WorldwideDocumento7 pagineCase Study-Precision WorldwideJustin Doh100% (3)

- 11 05 12 2022 Industrial Grinder ConclusionDocumento9 pagine11 05 12 2022 Industrial Grinder ConclusionPragathi SundarNessuna valutazione finora

- Sandvick Stainless Welding Products (S 236 Eng 2006)Documento27 pagineSandvick Stainless Welding Products (S 236 Eng 2006)Anonymous yQ7SQrNessuna valutazione finora

- 5.1 - Raymond Monroe - SFSADocumento8 pagine5.1 - Raymond Monroe - SFSAAnonymous iztPUhIiNessuna valutazione finora

- New Developments in Gear HobbingDocumento8 pagineNew Developments in Gear HobbingpongerkeNessuna valutazione finora

- Welding Gas P-8173Documento6 pagineWelding Gas P-8173kapurrrnNessuna valutazione finora

- Precision Worldwide, Inc. Case StudyDocumento3 paginePrecision Worldwide, Inc. Case Studytico6020% (1)

- 3Documento1 pagina3Joane ColipanoNessuna valutazione finora

- Script For EconomicsDocumento5 pagineScript For EconomicsDen mark RamirezNessuna valutazione finora

- Term Paper International EconomicsDocumento5 pagineTerm Paper International Economicsafmzkbysdbblih100% (1)

- PreviewPDF PDFDocumento2 paginePreviewPDF PDFLing TanNessuna valutazione finora

- I. Title: Global Cities II. Learning Objectives:: York, London, TokyoDocumento3 pagineI. Title: Global Cities II. Learning Objectives:: York, London, TokyoTam Gerald CalzadoNessuna valutazione finora

- Cost Accounting Procedure For Spoiled GoodsDocumento3 pagineCost Accounting Procedure For Spoiled GoodszachNessuna valutazione finora

- InvoicehhhhDocumento1 paginaInvoicehhhhAravind RNessuna valutazione finora

- Faisal, Napitupulu and Chariri (2019) Corporate Social and Environmental Responsibility Disclosure in Indonesian Companies Symbolic or SubstantiveDocumento20 pagineFaisal, Napitupulu and Chariri (2019) Corporate Social and Environmental Responsibility Disclosure in Indonesian Companies Symbolic or SubstantiveMuhamad Arif RohmanNessuna valutazione finora

- Economics Perfectly Competitive MarketDocumento25 pagineEconomics Perfectly Competitive MarketEsha DivNessuna valutazione finora

- Steel Asia 9.28.23Documento1 paginaSteel Asia 9.28.23Kate PerezNessuna valutazione finora

- Overhead Analysis QuestionsDocumento9 pagineOverhead Analysis QuestionsKiri chrisNessuna valutazione finora

- Indian Institute of Technology: Bank Copy Session:2010-2011 (SPRING)Documento2 pagineIndian Institute of Technology: Bank Copy Session:2010-2011 (SPRING)Maheshchandra PatilNessuna valutazione finora

- Salary Slip FTMO Nov-2021Documento1 paginaSalary Slip FTMO Nov-2021Ahsan Bin AsimNessuna valutazione finora

- Legal Register TemplateDocumento1 paginaLegal Register TemplateMohd Zubaidi Bin OthmanNessuna valutazione finora

- Chapter Twelve QuestionsDocumento3 pagineChapter Twelve QuestionsabguyNessuna valutazione finora

- 1009-Article Text-1731-1-10-20171225 PDFDocumento6 pagine1009-Article Text-1731-1-10-20171225 PDFPursottam SarafNessuna valutazione finora

- Peri Up Flex Core ComponentsDocumento50 paginePeri Up Flex Core ComponentsDavid BourcetNessuna valutazione finora

- Property Ownership AccessionDocumento134 pagineProperty Ownership AccessionCharmaine AlcachupasNessuna valutazione finora

- Solar Energy Trends and Enabling TechnologiesDocumento10 pagineSolar Energy Trends and Enabling TechnologiesRendy SetiadyNessuna valutazione finora

- Investment Climate Brochure - Ethiopia PDFDocumento32 pagineInvestment Climate Brochure - Ethiopia PDFR100% (1)

- Varroc Final ReportDocumento43 pagineVarroc Final ReportKamlakar AvhadNessuna valutazione finora

- Anna University Question PaperDocumento5 pagineAnna University Question PaperSukesh R100% (1)

- FPEF ED 2017 Lo Res Pagination 002Documento136 pagineFPEF ED 2017 Lo Res Pagination 002klapperdopNessuna valutazione finora

- Challenges and Opportunities For Regional Integration in AfricaDocumento14 pagineChallenges and Opportunities For Regional Integration in AfricaBOUAKKAZ NAOUALNessuna valutazione finora

- Analysis On KFC in ChinaDocumento9 pagineAnalysis On KFC in ChinaNicko HawinataNessuna valutazione finora

- I. Balance Sheet DEC 31ST, 2014 DEC 31ST, 2015Documento1 paginaI. Balance Sheet DEC 31ST, 2014 DEC 31ST, 2015WawerudasNessuna valutazione finora

- Human Capital and Economic Growth - Robert J BarroDocumento18 pagineHuman Capital and Economic Growth - Robert J BarroWalter Weber GimenezNessuna valutazione finora

- Gauteng Department of Education Provincial Examination: MARKS: 150 TIME: 2 HoursDocumento12 pagineGauteng Department of Education Provincial Examination: MARKS: 150 TIME: 2 HoursKillNessuna valutazione finora

- Randstad Salary Guide Engineering Web PDFDocumento28 pagineRandstad Salary Guide Engineering Web PDFMer HavatNessuna valutazione finora

- Top 500 Taxpayers in The Philippines 2011Documento10 pagineTop 500 Taxpayers in The Philippines 2011Mykiru IsyuseroNessuna valutazione finora