Potrebbero piacerti anche

- Aarushi VerdictDocumento273 pagineAarushi VerdictOutlookMagazine88% (8)

- SAVANT FrameworkDocumento41 pagineSAVANT FrameworkAkhilesh Kumar100% (1)

- Types of Stamps and Some Concepts of Stamp DutyDocumento5 pagineTypes of Stamps and Some Concepts of Stamp DutyNikhil Kasat100% (3)

- ThesisDocumento44 pagineThesisjagritiNessuna valutazione finora

- Chillers, Fcu'S & Ahu'S: Yasser El Kabany 35366866 010-9977779 35366266Documento31 pagineChillers, Fcu'S & Ahu'S: Yasser El Kabany 35366866 010-9977779 35366266mostafaabdelrazikNessuna valutazione finora

- Corporate Social ResponsibilityDocumento5 pagineCorporate Social Responsibilitypranavmenon19Nessuna valutazione finora

- Blended Finance Draft 1 HFHDHDocumento8 pagineBlended Finance Draft 1 HFHDHPriyanshu RanjanNessuna valutazione finora

- Essay - Interplay Between CSR & GSTDocumento8 pagineEssay - Interplay Between CSR & GSTAkanksha BohraNessuna valutazione finora

- 2 Percent India CSR ReportDocumento4 pagine2 Percent India CSR ReportAditi SinghNessuna valutazione finora

- India:: India's New Corporate Social Responsibility Requirements - Beware of The PitfallsDocumento2 pagineIndia:: India's New Corporate Social Responsibility Requirements - Beware of The PitfallsdvbadvarNessuna valutazione finora

- Assessment of Charitable Trust and InstitutionDocumento52 pagineAssessment of Charitable Trust and InstitutionAnonymous JJhHAdY5HzNessuna valutazione finora

- 12 - Chapter 4Documento31 pagine12 - Chapter 4Suraj DubeyNessuna valutazione finora

- CSR ICAI Guidelines FAQ'sDocumento21 pagineCSR ICAI Guidelines FAQ'ssmsuvagiaNessuna valutazione finora

- CAclubindia News - CSR - Auditors' Responsibility To Qualify in Audit ReportDocumento2 pagineCAclubindia News - CSR - Auditors' Responsibility To Qualify in Audit ReportMahaveer DhelariyaNessuna valutazione finora

- Essay - Interplay Between CSR & GSTDocumento8 pagineEssay - Interplay Between CSR & GSTAkanksha BohraNessuna valutazione finora

- Corporate Social ResponsiblityDocumento19 pagineCorporate Social ResponsiblityAakashNessuna valutazione finora

- Types of Organizations Revised Corporation CodeDocumento11 pagineTypes of Organizations Revised Corporation CodeNadie LrdNessuna valutazione finora

- Norms: Direct Tax Code For NposDocumento6 pagineNorms: Direct Tax Code For NposmahamayaviNessuna valutazione finora

- Term Paper - LLCDocumento9 pagineTerm Paper - LLCapi-115328034Nessuna valutazione finora

- L3C How ToDocumento4 pagineL3C How ToAvant Garland FixxNessuna valutazione finora

- CSR Policy 2014Documento3 pagineCSR Policy 2014Ankush RawatNessuna valutazione finora

- CSR Policy PDFDocumento12 pagineCSR Policy PDFAkanksha DhandareNessuna valutazione finora

- Law Important QuestionsDocumento30 pagineLaw Important QuestionsSudarshan TakNessuna valutazione finora

- Amendments in Company LawDocumento37 pagineAmendments in Company LawAbhishek PareekNessuna valutazione finora

- CSR As Per Companies Act, 2013Documento7 pagineCSR As Per Companies Act, 2013Meghna S NedumpurathuNessuna valutazione finora

- Tax Deductions Under Section 80 GGBDocumento8 pagineTax Deductions Under Section 80 GGBAnamika VatsaNessuna valutazione finora

- CSR-Profit Calculation-CompaniesDocumento3 pagineCSR-Profit Calculation-Companiescanamanagrawal11Nessuna valutazione finora

- Chap 018Documento40 pagineChap 018DimaNessuna valutazione finora

- Federal Income Taxation of LLC Members - Morris, Manning & Martin, LLPDocumento8 pagineFederal Income Taxation of LLC Members - Morris, Manning & Martin, LLPLen PageNessuna valutazione finora

- (Insert DD Month YYYY) : Re: DividendsDocumento3 pagine(Insert DD Month YYYY) : Re: Dividendssanjeev parajuliNessuna valutazione finora

- 0205 - Pragati - Verma - Assignment - 2 - Pragati VermaDocumento6 pagine0205 - Pragati - Verma - Assignment - 2 - Pragati VermaAKSHAT SINGHNessuna valutazione finora

- Firb Advisory Faqs (Firms, Atir, and Abr)Documento10 pagineFirb Advisory Faqs (Firms, Atir, and Abr)Asam Marie FernandezNessuna valutazione finora

- Unit - 5 Study Material ACGDocumento16 pagineUnit - 5 Study Material ACGAbhijeet UpadhyayNessuna valutazione finora

- Corporate Social Responsibility (CSR) Policy: Page 1 of 12Documento12 pagineCorporate Social Responsibility (CSR) Policy: Page 1 of 12Shubham Jain ModiNessuna valutazione finora

- Corporate Social ResponsibilityDocumento8 pagineCorporate Social Responsibilityvishad srivastavaNessuna valutazione finora

- Chapter 7 - Introduction To Nonprofit AccountingDocumento16 pagineChapter 7 - Introduction To Nonprofit AccountingSuzanne SenadreNessuna valutazione finora

- CSR Footnotes2Documento5 pagineCSR Footnotes2Priyadarshan NairNessuna valutazione finora

- Grant: Tax Deductibility Tax Deduction at Source Hop, Skip and Ouch! CSR Compatibility TableDocumento4 pagineGrant: Tax Deductibility Tax Deduction at Source Hop, Skip and Ouch! CSR Compatibility TablePoltu GhoshNessuna valutazione finora

- One Person CompanyDocumento73 pagineOne Person Companyraajsekhar020Nessuna valutazione finora

- What Is The Difference Between An LLC & LLPDocumento7 pagineWhat Is The Difference Between An LLC & LLPAlok MishraNessuna valutazione finora

- ApplicabilityDocumento4 pagineApplicabilityvasantharaoNessuna valutazione finora

- 2-2018ed-EDITION-CHAPTER 1Documento31 pagine2-2018ed-EDITION-CHAPTER 1Joebet Balbin BonifacioNessuna valutazione finora

- Taxation Law: TopicDocumento9 pagineTaxation Law: TopicPritam MuhuriNessuna valutazione finora

- Patna University IMPORTANT THEORY QUESTION TAXATION 2023Documento49 paginePatna University IMPORTANT THEORY QUESTION TAXATION 2023satishksatish777Nessuna valutazione finora

- Declaration and Payment of Dividend-Compliance RequirementsDocumento8 pagineDeclaration and Payment of Dividend-Compliance RequirementsSherin BabuNessuna valutazione finora

- Corporate Social ResponsibilityDocumento24 pagineCorporate Social ResponsibilityNaveen MettaNessuna valutazione finora

- CH 16Documento36 pagineCH 16DrellyNessuna valutazione finora

- Appeals Court Deals "Rollovers As Business Start-Ups" (ROBS) A Blow As A Business Financing StrategyDocumento7 pagineAppeals Court Deals "Rollovers As Business Start-Ups" (ROBS) A Blow As A Business Financing StrategyPriyanka DargadNessuna valutazione finora

- Companies Registered Under The Section 8 of Companies ActDocumento7 pagineCompanies Registered Under The Section 8 of Companies ActGriffith Biju John (GBJ)Nessuna valutazione finora

- Limited Liability Partnership Act, 2008 and Its UniquenessDocumento7 pagineLimited Liability Partnership Act, 2008 and Its UniquenessYazhini UmaNessuna valutazione finora

- Accounting and Reporting For Private Not-For-Profit EntitiesDocumento42 pagineAccounting and Reporting For Private Not-For-Profit EntitiesJordan YoungNessuna valutazione finora

- Master of Business Administration - MBA Semester 3 Subject Code - MF0012 Subject Name - Taxation Management 4 Credits (Book ID: B1210) Assignment Set-1 (60 Marks)Documento10 pagineMaster of Business Administration - MBA Semester 3 Subject Code - MF0012 Subject Name - Taxation Management 4 Credits (Book ID: B1210) Assignment Set-1 (60 Marks)balakalasNessuna valutazione finora

- Can NGO Founder Draw A SalaryDocumento2 pagineCan NGO Founder Draw A SalaryBibhu Prasad SahuNessuna valutazione finora

- Previleges of Small CompaniesDocumento9 paginePrevileges of Small CompaniesRahul ShahNessuna valutazione finora

- BL ProjectDocumento6 pagineBL Projectsarathat7Nessuna valutazione finora

- CSR AssignmentDocumento7 pagineCSR AssignmentNiharikac1995Nessuna valutazione finora

- LLPCollegeDocumento25 pagineLLPCollegeKeshavNessuna valutazione finora

- Acw 1000 Assigment 2Documento8 pagineAcw 1000 Assigment 2KooKie KeeNessuna valutazione finora

- LLP Tech MemoDocumento4 pagineLLP Tech MemoGroup ShareNessuna valutazione finora

- Sem 5 TaxDocumento22 pagineSem 5 TaxPalash JainNessuna valutazione finora

- Study Guide For Close CorporationsDocumento25 pagineStudy Guide For Close CorporationsPetrinaNessuna valutazione finora

- A034 Gopika A058 MayankDocumento8 pagineA034 Gopika A058 Mayankgopika mundraNessuna valutazione finora

- ACCT2201me: ACCT2201 Tutorial 1 Solutions - PDF Tutorial 1 SolutionsDocumento5 pagineACCT2201me: ACCT2201 Tutorial 1 Solutions - PDF Tutorial 1 SolutionsNatalie Laurent SiaNessuna valutazione finora

- Income Declaration Scheme Rules, 2016: Form 1Documento9 pagineIncome Declaration Scheme Rules, 2016: Form 1Nikhil KasatNessuna valutazione finora

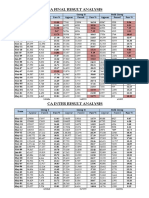

- CA Result AnalysisDocumento1 paginaCA Result AnalysisNikhil KasatNessuna valutazione finora

- Black Money BillDocumento30 pagineBlack Money BillNikhil KasatNessuna valutazione finora

- Hedging With Financial DerivativesDocumento30 pagineHedging With Financial DerivativesNikhil KasatNessuna valutazione finora

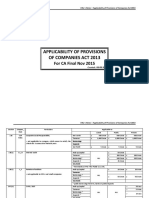

- ApplicabiliTY of ProvisionsDocumento3 pagineApplicabiliTY of ProvisionsNikhil KasatNessuna valutazione finora

- Agricultural Income: Agricultural Income: - As Per Sec 10 (1) Agricultural Income Earned by TheDocumento9 pagineAgricultural Income: Agricultural Income: - As Per Sec 10 (1) Agricultural Income Earned by TheNikhil KasatNessuna valutazione finora

- Curriculum VitaeDocumento13 pagineCurriculum VitaeNikhil KasatNessuna valutazione finora

- CA Final Writing Professional Ethics AnswersDocumento2 pagineCA Final Writing Professional Ethics AnswersNikhil KasatNessuna valutazione finora

- Defamation Under Common LawDocumento6 pagineDefamation Under Common LawNikhil KasatNessuna valutazione finora

- Fees Calculation For Increase in Authorised Share Capital Form SH 7, Only For GujaratDocumento10 pagineFees Calculation For Increase in Authorised Share Capital Form SH 7, Only For GujaratNikhil KasatNessuna valutazione finora

- August Month CompliancesDocumento1 paginaAugust Month CompliancesNikhil KasatNessuna valutazione finora

- Cusoms Valuation MaterialDocumento8 pagineCusoms Valuation MaterialNikhil KasatNessuna valutazione finora

- Privileges To Small CompaniesDocumento2 paginePrivileges To Small CompaniesNikhil KasatNessuna valutazione finora

- SN Vertical Due Dates Particular Consequence of Non ComplianceDocumento1 paginaSN Vertical Due Dates Particular Consequence of Non ComplianceNikhil KasatNessuna valutazione finora

- Shipping - Documents - Lpg01Documento30 pagineShipping - Documents - Lpg01Romandon RomandonNessuna valutazione finora

- 10.4324 9781003172246 PreviewpdfDocumento76 pagine10.4324 9781003172246 Previewpdfnenelindelwa274Nessuna valutazione finora

- Notice - Carte Pci - Msi - Pc54g-Bt - 2Documento46 pagineNotice - Carte Pci - Msi - Pc54g-Bt - 2Lionnel de MarquayNessuna valutazione finora

- Ifm 8 & 9Documento2 pagineIfm 8 & 9Ranan AlaghaNessuna valutazione finora

- Unit Test 11 PDFDocumento1 paginaUnit Test 11 PDFYONessuna valutazione finora

- Business Enterprise Simulation Quarter 3 - Module 2 - Lesson 1: Analyzing The MarketDocumento13 pagineBusiness Enterprise Simulation Quarter 3 - Module 2 - Lesson 1: Analyzing The MarketJtm GarciaNessuna valutazione finora

- Specpro.09.Salazar vs. Court of First Instance of Laguna and Rivera, 64 Phil. 785 (1937)Documento12 pagineSpecpro.09.Salazar vs. Court of First Instance of Laguna and Rivera, 64 Phil. 785 (1937)John Paul VillaflorNessuna valutazione finora

- Gandhi An Exemplary LeaderDocumento3 pagineGandhi An Exemplary LeaderpatcynNessuna valutazione finora

- HDFC Bank Summer Internship Project: Presented By:-Kandarp SinghDocumento12 pagineHDFC Bank Summer Internship Project: Presented By:-Kandarp Singhkandarp_singh_1Nessuna valutazione finora

- Pte Links N TipsDocumento48 paginePte Links N TipsKuljinder VirdiNessuna valutazione finora

- Glories of Srimad Bhagavatam - Bhaktivedanta VidyapithaDocumento7 pagineGlories of Srimad Bhagavatam - Bhaktivedanta VidyapithaPrajot NairNessuna valutazione finora

- C1 Level ExamDocumento2 pagineC1 Level ExamEZ English WorkshopNessuna valutazione finora

- People v. Bandojo, JR., G.R. No. 234161, October 17, 2018Documento21 paginePeople v. Bandojo, JR., G.R. No. 234161, October 17, 2018Olga Pleños ManingoNessuna valutazione finora

- Philippine National Development Goals Vis-A-Vis The Theories and Concepts of Public Administration and Their Applications.Documento2 paginePhilippine National Development Goals Vis-A-Vis The Theories and Concepts of Public Administration and Their Applications.Christian LeijNessuna valutazione finora

- Philippine ConstitutionDocumento17 paginePhilippine ConstitutionLovelyn B. OliverosNessuna valutazione finora

- Insura CoDocumento151 pagineInsura CoSiyuan SunNessuna valutazione finora

- Printed by SYSUSER: Dial Toll Free 1912 For Bill & Supply ComplaintsDocumento1 paginaPrinted by SYSUSER: Dial Toll Free 1912 For Bill & Supply ComplaintsRISHABH YADAVNessuna valutazione finora

- FRA - Project - NHPC - Group2 - R05Documento29 pagineFRA - Project - NHPC - Group2 - R05DHANEESH KNessuna valutazione finora

- The Engraves of Macau by A. Borget and L. Benett in Stella Blandy's Les Épreuves de Norbert en Chine' (1883)Documento8 pagineThe Engraves of Macau by A. Borget and L. Benett in Stella Blandy's Les Épreuves de Norbert en Chine' (1883)Ivo CarneiroNessuna valutazione finora

- GOUP GO of 8 May 2013 For EM SchoolsDocumento8 pagineGOUP GO of 8 May 2013 For EM SchoolsDevendra DamleNessuna valutazione finora

- Jurnal AJISDocumento16 pagineJurnal AJISElsa AugusttenNessuna valutazione finora

- Literature ReviewDocumento11 pagineLiterature ReviewGaurav Badlani71% (7)

- Jonathan Bishop's Election Address For The Pontypridd Constituency in GE2019Documento1 paginaJonathan Bishop's Election Address For The Pontypridd Constituency in GE2019Councillor Jonathan BishopNessuna valutazione finora

- General Concepts and Principles of ObligationsDocumento61 pagineGeneral Concepts and Principles of ObligationsJoAiza DiazNessuna valutazione finora

- Susan Rose's Legal Threat To Myself and The Save Ardmore CoalitionDocumento2 pagineSusan Rose's Legal Threat To Myself and The Save Ardmore CoalitionDouglas MuthNessuna valutazione finora

- Reading Comprehension TextDocumento2 pagineReading Comprehension TextMelanie Valeria Gualotuña GancinoNessuna valutazione finora

- 4-Cortina-Conill - 2016-Ethics of VulnerabilityDocumento21 pagine4-Cortina-Conill - 2016-Ethics of VulnerabilityJuan ApcarianNessuna valutazione finora