Potrebbero piacerti anche

- Deadly Weapon Cover Letter For RedemptionDocumento2 pagineDeadly Weapon Cover Letter For Redemptiondouglas jones95% (40)

- Tax RemediesDocumento14 pagineTax RemediesCha100% (3)

- Tax Remedies NotesDocumento16 pagineTax Remedies Notescristiepearl100% (6)

- Tax Remedies Quiz ReyesDocumento4 pagineTax Remedies Quiz ReyesMary Therese Gabrielle Estioko100% (2)

- Tax Reviewer - EstateDocumento6 pagineTax Reviewer - EstateNicole Autriz100% (1)

- in Re Union CarbideDocumento2 paginein Re Union Carbidepja_14Nessuna valutazione finora

- I. Remedies of The GovernmentDocumento12 pagineI. Remedies of The GovernmentJunivenReyUmadhayNessuna valutazione finora

- TAX REMEDIES NotesDocumento6 pagineTAX REMEDIES NotesLemuel Angelo M. Eleccion100% (2)

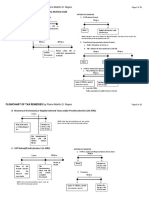

- Flowchart of Tax Remedies I. Remedies UnDocumento12 pagineFlowchart of Tax Remedies I. Remedies UnKevin Ken Sison Ganchero100% (2)

- Assessment Process FlowchartDocumento4 pagineAssessment Process FlowchartMaria Reylan GarciaNessuna valutazione finora

- Shaffer Vs HeitnerDocumento5 pagineShaffer Vs Heitnerpja_14Nessuna valutazione finora

- Barrios Vs Go ThongDocumento1 paginaBarrios Vs Go Thongpja_14Nessuna valutazione finora

- Searches and SeizuresDocumento47 pagineSearches and SeizuresDanielle AngelaNessuna valutazione finora

- Robidoux Et Al V Wacker Family Trust Et Al - Document No. 10Documento2 pagineRobidoux Et Al V Wacker Family Trust Et Al - Document No. 10Justia.comNessuna valutazione finora

- Taxation - 8 Tax Remedies Under NIRCDocumento34 pagineTaxation - 8 Tax Remedies Under NIRCcmv mendoza100% (3)

- Chapter 1 Tax 2Documento5 pagineChapter 1 Tax 2Hazel Jane EsclamadaNessuna valutazione finora

- Revised Corporation Code - SummaryDocumento34 pagineRevised Corporation Code - SummaryAldrin ZolinaNessuna valutazione finora

- Tax 2 (Remedies & CTA Jurisdiction)Documento13 pagineTax 2 (Remedies & CTA Jurisdiction)Monice RiveraNessuna valutazione finora

- Tax Remedies Flowchart (Revised)Documento6 pagineTax Remedies Flowchart (Revised)GersonGamas0% (1)

- Tax Remedies Principles and CasesDocumento75 pagineTax Remedies Principles and CasesGeorge PandaNessuna valutazione finora

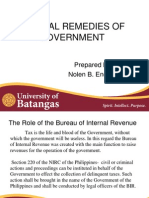

- Administrative Remedies of The GovernmentDocumento5 pagineAdministrative Remedies of The GovernmentrobbyNessuna valutazione finora

- Tax Flowchart Remedies (Tokie)Documento9 pagineTax Flowchart Remedies (Tokie)Tokie TokiNessuna valutazione finora

- Income Taxation Reviewer - San BedaDocumento128 pagineIncome Taxation Reviewer - San BedaJennybabe Peta100% (8)

- Gross Estate ReviewerDocumento8 pagineGross Estate ReviewerCharles RiveraNessuna valutazione finora

- TAX REMEDIES by Sababan Reviewer 2008 EdDocumento11 pagineTAX REMEDIES by Sababan Reviewer 2008 Edolaydyosa95% (20)

- Tax Reviewer (Mfp-2)Documento13 pagineTax Reviewer (Mfp-2)Mikaela Pamatmat100% (1)

- Powers and Duties of The BIRDocumento7 paginePowers and Duties of The BIROliveros DMNessuna valutazione finora

- Motion To Cancel and Reset Hearing: Regional Trial CourtDocumento2 pagineMotion To Cancel and Reset Hearing: Regional Trial Courtattymel100% (1)

- Written Statement and Objections On Behalf of Defendant in Injunction SuitDocumento22 pagineWritten Statement and Objections On Behalf of Defendant in Injunction SuitSridhara babu. N - ಶ್ರೀಧರ ಬಾಬು. ಎನ್87% (45)

- VAT ReviewerDocumento11 pagineVAT ReviewerMarianne AgunoyNessuna valutazione finora

- Strict Construction of Penal and Taxing StatutesDocumento17 pagineStrict Construction of Penal and Taxing StatutesUdit Bhatia67% (3)

- REMEDIES OF THE TAXPAYER and GOVERNMENTDocumento7 pagineREMEDIES OF THE TAXPAYER and GOVERNMENTChrisMartinNessuna valutazione finora

- Tax Remedies QuizzerDocumento3 pagineTax Remedies QuizzerCharrie Grace Pablo29% (7)

- Taxation - 7 Tax Remedies Under LGCDocumento3 pagineTaxation - 7 Tax Remedies Under LGCcmv mendozaNessuna valutazione finora

- Pre-Board - Business Law 2016Documento11 paginePre-Board - Business Law 2016Kenneth Bryan Tegerero TegioNessuna valutazione finora

- Tax Remedies ReviewerDocumento9 pagineTax Remedies ReviewerheirarchyNessuna valutazione finora

- Tax2 - Local Taxation ReviewerDocumento4 pagineTax2 - Local Taxation Reviewercardeguzman89% (9)

- Securities Regulation Code. QuestionsDocumento3 pagineSecurities Regulation Code. QuestionsIELTS100% (1)

- Charter Insurance Vs MV National HonorDocumento2 pagineCharter Insurance Vs MV National Honorpja_14100% (1)

- Securities Regulation Code Reviewer ComrevDocumento7 pagineSecurities Regulation Code Reviewer ComrevNiel Edar Balleza100% (1)

- Tax Judicial Remedies of GovernmentDocumento34 pagineTax Judicial Remedies of GovernmentNoullen Banuelos100% (5)

- CHAP 1 GEN. PRIN 7th PDFDocumento87 pagineCHAP 1 GEN. PRIN 7th PDFJericho Luis100% (9)

- Estacion Vs BernardoDocumento1 paginaEstacion Vs Bernardopja_14100% (1)

- Bar Examination Questionnaire For Civil LawDocumento6 pagineBar Examination Questionnaire For Civil LawAnonymous 1YK61WEPqNNessuna valutazione finora

- Foreign Tax CreditDocumento2 pagineForeign Tax CreditSophiaFrancescaEspinosaNessuna valutazione finora

- David V AgbayDocumento19 pagineDavid V AgbayEmary GutierrezNessuna valutazione finora

- Final Tax ExamDocumento10 pagineFinal Tax ExamGerald RojasNessuna valutazione finora

- Donor's Tax and Foreign Tax Credit (Presentation Slides)Documento5 pagineDonor's Tax and Foreign Tax Credit (Presentation Slides)Kez100% (1)

- Module 4 - Value Added TaxDocumento16 pagineModule 4 - Value Added Taxanon_455551365Nessuna valutazione finora

- Flowchart of Tax RemediesDocumento3 pagineFlowchart of Tax RemediesPetrovich Tamag50% (4)

- Tax Rev GenPrinciplesDocumento8 pagineTax Rev GenPrinciplesAngela AngelesNessuna valutazione finora

- Part 1 - Nature of International LawDocumento27 paginePart 1 - Nature of International LawRyan Leocario100% (2)

- People vs. Ortega, G.R. No. 116736, July 24, 1997, 276 SCRA 166Documento2 paginePeople vs. Ortega, G.R. No. 116736, July 24, 1997, 276 SCRA 166Teoti Navarro Reyes100% (3)

- Far Eastern Vs CA and PpaDocumento1 paginaFar Eastern Vs CA and Ppapja_14Nessuna valutazione finora

- RemediesDocumento45 pagineRemediesCzarina100% (1)

- Yaptinchay Vs Del RosarioDocumento1 paginaYaptinchay Vs Del Rosariopja_14Nessuna valutazione finora

- Quicknotes Taxation by Atty Jack de VeraDocumento215 pagineQuicknotes Taxation by Atty Jack de VeraGene Kenneth Paragas100% (1)

- Local Government TaxationDocumento7 pagineLocal Government TaxationCeresjudicataNessuna valutazione finora

- Diego Vs CastilloDocumento3 pagineDiego Vs CastilloCamilleBenjaminRemorozaNessuna valutazione finora

- Government of The United States of America v. Hon. Guillermo PurgananDocumento1 paginaGovernment of The United States of America v. Hon. Guillermo Purgananpja_14Nessuna valutazione finora

- Republic Act No. 9298 - Philippine Accountancy Act OF 2004: Reference: Sirug, Red. Notes From Handouts On Auditing TheoryDocumento12 pagineRepublic Act No. 9298 - Philippine Accountancy Act OF 2004: Reference: Sirug, Red. Notes From Handouts On Auditing TheoryAlex OngNessuna valutazione finora

- Chapter 18 - Tax Remedies: Multiple Choice - Theory 1Documento12 pagineChapter 18 - Tax Remedies: Multiple Choice - Theory 1Emmanuel PenullarNessuna valutazione finora

- Dealings in Property: Lesson 12Documento18 pagineDealings in Property: Lesson 12lcNessuna valutazione finora

- Tax Review Q and A Quiz 1 and 2 FinalsDocumento19 pagineTax Review Q and A Quiz 1 and 2 FinalsAngel Xavier CalejaNessuna valutazione finora

- Examination QuestionsDocumento16 pagineExamination QuestionsAly Concepcion100% (1)

- Vargas Vs LangcayDocumento2 pagineVargas Vs Langcaypja_14Nessuna valutazione finora

- Mnemonics in Taxation Law - GarciaDocumento82 pagineMnemonics in Taxation Law - Garciadavaounion100% (2)

- Tax 2 Notes Finals 4Documento36 pagineTax 2 Notes Finals 4Boom ManuelNessuna valutazione finora

- Lapanday Vs AngalaDocumento1 paginaLapanday Vs Angalapja_14Nessuna valutazione finora

- Topic 1 Preferential TaxationDocumento15 pagineTopic 1 Preferential TaxationRoMe LynNessuna valutazione finora

- Powers of The BIRDocumento11 paginePowers of The BIRmartina lopez100% (1)

- Taxation Reviewer FAPDocumento85 pagineTaxation Reviewer FAPReyrhye RopaNessuna valutazione finora

- Tax RemediesDocumento13 pagineTax RemediesYan MoretzNessuna valutazione finora

- Tax Remedies Under The NIRCDocumento37 pagineTax Remedies Under The NIRCkath100% (1)

- Schmitz Transport Vs Transport VentureDocumento2 pagineSchmitz Transport Vs Transport Venturepja_14Nessuna valutazione finora

- Simeon Mahipus Vs PeopleDocumento1 paginaSimeon Mahipus Vs PeopleCristineNessuna valutazione finora

- Chapter 8 Regular Income Tax - Exclusion From Gross IncomeDocumento2 pagineChapter 8 Regular Income Tax - Exclusion From Gross IncomeJason MablesNessuna valutazione finora

- Vat On Importation: Presumptive Input TaxDocumento13 pagineVat On Importation: Presumptive Input TaxNerish PlazaNessuna valutazione finora

- Taxation KeyDocumento12 pagineTaxation KeyRerereNessuna valutazione finora

- A. Individuals:: 1. Citizens of The PhilippinesDocumento5 pagineA. Individuals:: 1. Citizens of The PhilippinesRaymond FaeldoñaNessuna valutazione finora

- Remedies of The TaxpayerDocumento6 pagineRemedies of The Taxpayereds billNessuna valutazione finora

- Concept of Assessment Requisites For A Valid Assessment: 10 Years After DiscoveryDocumento5 pagineConcept of Assessment Requisites For A Valid Assessment: 10 Years After DiscoveryJD BarcellanoNessuna valutazione finora

- in Re Estate of Ferdinand Marcos - Human RightsDocumento6 paginein Re Estate of Ferdinand Marcos - Human Rightspja_14Nessuna valutazione finora

- Margate Vs RabacalDocumento2 pagineMargate Vs Rabacalpja_14Nessuna valutazione finora

- Cui Vs PiccioDocumento1 paginaCui Vs Picciopja_14Nessuna valutazione finora

- Inter Orient Vs NLRCDocumento4 pagineInter Orient Vs NLRCpja_14Nessuna valutazione finora

- Yangco Vs LasernaDocumento5 pagineYangco Vs Lasernapja_14Nessuna valutazione finora

- Sulpicio Lines Vs CursoDocumento1 paginaSulpicio Lines Vs Cursopja_14Nessuna valutazione finora

- Valenzuela Hardwood Vs CADocumento1 paginaValenzuela Hardwood Vs CApja_14Nessuna valutazione finora

- Yek Tong vs. American President Lines, Inc.Documento1 paginaYek Tong vs. American President Lines, Inc.pja_14Nessuna valutazione finora

- Sison Vs Boa and FergusonDocumento1 paginaSison Vs Boa and Fergusonpja_14Nessuna valutazione finora

- Neelkanth Writ Jurisdiction: A Comparative Study: EnglandDocumento48 pagineNeelkanth Writ Jurisdiction: A Comparative Study: EnglandNOONEUNKNOWNNessuna valutazione finora

- Statement of BHRPC On The Terror Attack On MumbaiDocumento2 pagineStatement of BHRPC On The Terror Attack On MumbaiOliullah Laskar100% (1)

- Nunavuumi Iqkaqtuijikkut La Cour de Justice Du NunavutDocumento11 pagineNunavuumi Iqkaqtuijikkut La Cour de Justice Du NunavutNunatsiaqNewsNessuna valutazione finora

- Julie Maxton PDFDocumento13 pagineJulie Maxton PDFElaine TanNessuna valutazione finora

- Bible Baptist Church Case DigestDocumento1 paginaBible Baptist Church Case DigestMyles RubioNessuna valutazione finora

- SQAO CasesDocumento48 pagineSQAO CasesjohanyarraNessuna valutazione finora

- Trump Motion - E Jean Carroll V Donald J Trump MEMORANDUM of LAW I 49Documento19 pagineTrump Motion - E Jean Carroll V Donald J Trump MEMORANDUM of LAW I 49Law&CrimeNessuna valutazione finora

- Carpio vs. Daroja 180 Scra 1Documento3 pagineCarpio vs. Daroja 180 Scra 1MykaNessuna valutazione finora

- Magtajas vs. PryceDocumento3 pagineMagtajas vs. PryceRoyce PedemonteNessuna valutazione finora

- Republic Vs Rosemoor Mining and Development Corporation - GR 149927 - March 30, 2004Documento9 pagineRepublic Vs Rosemoor Mining and Development Corporation - GR 149927 - March 30, 2004BerniceAnneAseñas-ElmacoNessuna valutazione finora

- Chua Yek Hong vs. Intermediate Appellate Court, 166 SCRA 183, No. L-74811 September 30, 1988Documento10 pagineChua Yek Hong vs. Intermediate Appellate Court, 166 SCRA 183, No. L-74811 September 30, 1988Marl Dela ROsaNessuna valutazione finora

- Appendix Declaration of Intent To Undergo A TB Test: Surname As Stated in The Border-Crossing DocumentDocumento2 pagineAppendix Declaration of Intent To Undergo A TB Test: Surname As Stated in The Border-Crossing DocumentSheikh NasiruddinNessuna valutazione finora

- SALES - Laforteza and de ApeDocumento3 pagineSALES - Laforteza and de ApeMariaAyraCelinaBatacanNessuna valutazione finora

- Difference Between Transfer and PromotionDocumento3 pagineDifference Between Transfer and PromotionLizCruz-Kim100% (1)

- Roberto R David Vs Judge Carmelita S. Gutierrez-FrueldaDocumento2 pagineRoberto R David Vs Judge Carmelita S. Gutierrez-FrueldaArthur John GarratonNessuna valutazione finora

- 1-Maintenance - by SMT YJ Padmasree PDFDocumento22 pagine1-Maintenance - by SMT YJ Padmasree PDFAniketh kuNessuna valutazione finora

- United States v. Richard Irizarry, 11th Cir. (2016)Documento10 pagineUnited States v. Richard Irizarry, 11th Cir. (2016)Scribd Government DocsNessuna valutazione finora

- Vda. de Villanueva vs. JuicoDocumento6 pagineVda. de Villanueva vs. JuicoGalilee RomasantaNessuna valutazione finora

- Villanueva V NiteDocumento11 pagineVillanueva V NiteHeidiNessuna valutazione finora