Potrebbero piacerti anche

- Tax Exemption Certificate RequestDocumento1 paginaTax Exemption Certificate RequestJannyManlaNessuna valutazione finora

- C. 7-9Documento14 pagineC. 7-9Christine Joy PrestozaNessuna valutazione finora

- 141.protesting BIR Assessments - dds.04.29.2010Documento2 pagine141.protesting BIR Assessments - dds.04.29.2010Arnold ApduaNessuna valutazione finora

- Bir RulingDocumento4 pagineBir Rulingdranreb ursabiaNessuna valutazione finora

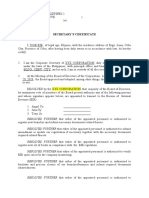

- Sample Board ResolutionDocumento11 pagineSample Board ResolutiongannwongNessuna valutazione finora

- Protesting The Deficiency Tax AssessmentDocumento2 pagineProtesting The Deficiency Tax AssessmentbutowskiNessuna valutazione finora

- ActDocumento2 pagineActJeffrey Garcia IlaganNessuna valutazione finora

- BIR Accreditation For CPAsDocumento1 paginaBIR Accreditation For CPAsECMH ACCOUNTING AND CONSULTANCY SERVICESNessuna valutazione finora

- TSL - Notice of Annual General MeetingDocumento2 pagineTSL - Notice of Annual General MeetingBusiness Daily Zimbabwe100% (1)

- DXDD Radio Station Franchise Tax StatusDocumento2 pagineDXDD Radio Station Franchise Tax StatuslhemnavalNessuna valutazione finora

- Secretary's Certificate of No Dispute TemplateDocumento1 paginaSecretary's Certificate of No Dispute TemplateJimi Solomon100% (1)

- Overview of Handling BIR Tax Audit in The PhilippinesDocumento3 pagineOverview of Handling BIR Tax Audit in The PhilippinesMarietta Fragata Ramiterre100% (2)

- RR 2-98Documento136 pagineRR 2-98hizelaryaNessuna valutazione finora

- Annual Meeting Minutes SummaryDocumento16 pagineAnnual Meeting Minutes SummaryMaureen Derial Panta100% (1)

- Letter Request - Tax ExemptionDocumento1 paginaLetter Request - Tax ExemptionJuan Frivaldo100% (10)

- Notice of Decision - TemplateDocumento2 pagineNotice of Decision - TemplateAmylene MedinaNessuna valutazione finora

- Goldland Property Corp Requests Certified Plan CopiesDocumento4 pagineGoldland Property Corp Requests Certified Plan CopiesJoshua Edward LaqueNessuna valutazione finora

- Compromise of BIR Tax LiabilityDocumento2 pagineCompromise of BIR Tax LiabilityIssaRoxas100% (2)

- Materials For How To Handle BIR Audit Common Issues - 2021 Sept 21Documento71 pagineMaterials For How To Handle BIR Audit Common Issues - 2021 Sept 21cool_peach100% (1)

- Requirements For Increase of Capital StocksDocumento3 pagineRequirements For Increase of Capital StocksNarciso Reyes Jr.0% (1)

- PH TAX FILER RELATED PARTY TRANSACTIONSDocumento3 paginePH TAX FILER RELATED PARTY TRANSACTIONSErica Caliuag0% (1)

- LISS AGATOK HOA Seeks Tax ExemptionDocumento2 pagineLISS AGATOK HOA Seeks Tax ExemptionfileksNessuna valutazione finora

- Sworn Statement - LOOSELEAF BOOK OF ACCTSDocumento2 pagineSworn Statement - LOOSELEAF BOOK OF ACCTSMagdalena Tupalar100% (1)

- Sworn Statement For Loose Leaf PTUDocumento1 paginaSworn Statement For Loose Leaf PTUKeith Pagurayan100% (1)

- Process For Application To Use LooseleafDocumento1 paginaProcess For Application To Use LooseleafFrancis MartinNessuna valutazione finora

- Protest Letter Against 2012 Tax AssessmentDocumento4 pagineProtest Letter Against 2012 Tax AssessmentPatrice Noelle Ramirez90% (10)

- Revenue Memorandum Order 26-2010Documento2 pagineRevenue Memorandum Order 26-2010Jayvee OlayresNessuna valutazione finora

- Dividend declaration compliance requirementsDocumento28 pagineDividend declaration compliance requirementsSarahNessuna valutazione finora

- Letter of Protest VAT MisdeclarationDocumento1 paginaLetter of Protest VAT MisdeclarationmrgroupofcompaniesNessuna valutazione finora

- Increase Capital Stock CertificateDocumento8 pagineIncrease Capital Stock CertificateSydney Cagatin100% (4)

- Kemp Coop Minutes For Cert of Good StandingDocumento7 pagineKemp Coop Minutes For Cert of Good StandingJf LarongNessuna valutazione finora

- Minutes of Meeting of Directors SpecialDocumento1 paginaMinutes of Meeting of Directors SpecialStephen HaldenNessuna valutazione finora

- Secretary CertificateDocumento2 pagineSecretary Certificatemikayz30100% (2)

- Partner's resolution authorizes bank account closureDocumento1 paginaPartner's resolution authorizes bank account closurePatrio Jr SeñeresNessuna valutazione finora

- ProtestLetter TICIDocumento4 pagineProtestLetter TICIdbircs100% (4)

- BIR Ruling on Informer's RewardDocumento4 pagineBIR Ruling on Informer's RewardAnonymous fnlSh4KHIgNessuna valutazione finora

- Affidavit of Non-Holding of Non Holding of Annual MeetingDocumento1 paginaAffidavit of Non-Holding of Non Holding of Annual MeetingJvsticeNick100% (1)

- Revised Application Process for Philippine NGO CertificationDocumento3 pagineRevised Application Process for Philippine NGO CertificationOmar Jayson Siao Vallejera73% (11)

- FREE Online Tax Return Audit Before FilingDocumento49 pagineFREE Online Tax Return Audit Before FilingIamangel10100% (17)

- Secretary Certificate Required by BIRDocumento2 pagineSecretary Certificate Required by BIRJulia100% (1)

- SEC Form Form For Appointment of OfficersDocumento1 paginaSEC Form Form For Appointment of Officersperrybc427100% (1)

- Corporate Board Resolution - Mr. Abdel Aziz DimapunongDocumento2 pagineCorporate Board Resolution - Mr. Abdel Aziz DimapunongMark VernonNessuna valutazione finora

- Secretary's Certificate for Board Resolution on International Business EndorsementDocumento2 pagineSecretary's Certificate for Board Resolution on International Business EndorsementTina UyNessuna valutazione finora

- SEC Cover SheetDocumento1 paginaSEC Cover SheetAya PulidoNessuna valutazione finora

- Rmo 12 2013 List of Unused Expired Orssiscis Annex D Docxdocx PDF FreeDocumento2 pagineRmo 12 2013 List of Unused Expired Orssiscis Annex D Docxdocx PDF FreeShitake Mitsuki100% (1)

- Secretary CertificateDocumento1 paginaSecretary CertificateStewart Paul Torre100% (1)

- Request For ReinvestigationDocumento9 pagineRequest For Reinvestigationjoel raz93% (15)

- Employee resignation affidavitDocumento3 pagineEmployee resignation affidavitJasmin MiroyNessuna valutazione finora

- Asiapro MDC Opinion, Re DO 174Documento4 pagineAsiapro MDC Opinion, Re DO 174Jay TanNessuna valutazione finora

- Accounting Services ContractDocumento4 pagineAccounting Services ContractDv Accounting100% (1)

- Notice of Preventive SuspensionDocumento1 paginaNotice of Preventive Suspensionmigz_ortaliza100% (1)

- No Pending Intra-Corporate Disputes CertificateDocumento1 paginaNo Pending Intra-Corporate Disputes Certificatemyrahj100% (4)

- BIR's Tax Ruling Process ExplainedDocumento3 pagineBIR's Tax Ruling Process ExplainedConnieAllanaMacapagaoNessuna valutazione finora

- BOARD RESOLUTION Appropriation of REDocumento2 pagineBOARD RESOLUTION Appropriation of REFamily FriendsNessuna valutazione finora

- Termination Letter TagalogDocumento8 pagineTermination Letter TagalogGerry MalgapoNessuna valutazione finora

- Company Sponsored Training AgreementDocumento4 pagineCompany Sponsored Training AgreementCrisCulminasNessuna valutazione finora

- BIR RulingDocumento3 pagineBIR RulingyakyakxxNessuna valutazione finora

- Bir Ruling On RetirementDocumento5 pagineBir Ruling On Retirementjerome barcoNessuna valutazione finora

- Tax Exemptions On Retirement PlansDocumento3 pagineTax Exemptions On Retirement PlansVola AriNessuna valutazione finora

- P&A - Taxation of Retirement BenefitsDocumento2 pagineP&A - Taxation of Retirement BenefitsCkey ArNessuna valutazione finora

- 2010 RMO 44-2010 eLA Rules eLA PDFDocumento3 pagine2010 RMO 44-2010 eLA Rules eLA PDFedong the greatNessuna valutazione finora

- Revenue Regulations No. 10-2020 PDFDocumento10 pagineRevenue Regulations No. 10-2020 PDFCharina Marie CaduaNessuna valutazione finora

- CBK Power RulingDocumento6 pagineCBK Power Rulingbishopblue0622Nessuna valutazione finora

- SEC Ruling On Fractional SharesDocumento2 pagineSEC Ruling On Fractional Sharesbishopblue0622Nessuna valutazione finora

- Kalookan Revenue Code PDFDocumento293 pagineKalookan Revenue Code PDFbishopblue0622100% (1)

- BIR Ruling DST On Loan and Security DocsDocumento8 pagineBIR Ruling DST On Loan and Security Docsbishopblue0622Nessuna valutazione finora

- Fulltext RMC No 86-2014Documento2 pagineFulltext RMC No 86-2014Gedan TanNessuna valutazione finora

- BIR Regs On OCWsDocumento4 pagineBIR Regs On OCWsbishopblue0622Nessuna valutazione finora

- BIR Regs On Condo CorporationsDocumento8 pagineBIR Regs On Condo Corporationsbishopblue0622Nessuna valutazione finora

- 11 TH Bipartite ALL INDIA NATIONALIZED BANKS OFFICERS FEDERATION'presentation To CLC CLCDocumento344 pagine11 TH Bipartite ALL INDIA NATIONALIZED BANKS OFFICERS FEDERATION'presentation To CLC CLCAnonymous 4yXWpDNessuna valutazione finora

- Stakeholder Engagement Plan SEP GAMBIA FISCAL MANAGEMENT DEVELOPMENT PROJECT P166695Documento103 pagineStakeholder Engagement Plan SEP GAMBIA FISCAL MANAGEMENT DEVELOPMENT PROJECT P166695Ali ZilbermanNessuna valutazione finora

- 5th CPC (Report, Vol II) PDFDocumento829 pagine5th CPC (Report, Vol II) PDFAdv. Sreedevi S100% (1)

- Navpen-Navv@nic - in 180022056 - 0: of ToDocumento25 pagineNavpen-Navv@nic - in 180022056 - 0: of ToPankaj TiwariNessuna valutazione finora

- Income Under The Head Salaries: (Section 15 - 17)Documento55 pagineIncome Under The Head Salaries: (Section 15 - 17)leela naga janaki rajitha attiliNessuna valutazione finora

- Prog: Bscac Level: 2.2: Year: 2016Documento137 pagineProg: Bscac Level: 2.2: Year: 2016Zic Zac100% (1)

- Central Government Supply Estimates 2009-10 Supplementary Budgetary InformationDocumento255 pagineCentral Government Supply Estimates 2009-10 Supplementary Budgetary InformationokfnNessuna valutazione finora

- G.R. No. 174173 March 7, 2012 MA. MELISSA A. GALANG, Petitioner, JULIA MALASUGUI, RespondentDocumento21 pagineG.R. No. 174173 March 7, 2012 MA. MELISSA A. GALANG, Petitioner, JULIA MALASUGUI, RespondentJoseph Santos GacayanNessuna valutazione finora

- Accounting For Governmental and Nonprofit Entities 17th Edition Reck Test BankDocumento51 pagineAccounting For Governmental and Nonprofit Entities 17th Edition Reck Test Bankjenatryphenaotni100% (27)

- UPJN Accounting ManualDocumento245 pagineUPJN Accounting ManualAnsu YadavNessuna valutazione finora

- Retiree Entitled to Monthly Pension for LifeDocumento2 pagineRetiree Entitled to Monthly Pension for LifeEarvin Joseph BaraceNessuna valutazione finora

- Risk Managemennt Chapter 1Documento35 pagineRisk Managemennt Chapter 1Tilahun GirmaNessuna valutazione finora

- Florendo v. Philam PlansDocumento1 paginaFlorendo v. Philam PlansJohney Doe50% (2)

- Spouse Visa Checklist 2021Documento11 pagineSpouse Visa Checklist 2021Isadora Sobredo100% (1)

- Towers Watson Attraction and Retention What Employees Value MostDocumento7 pagineTowers Watson Attraction and Retention What Employees Value MostPatricia CruzNessuna valutazione finora

- Compensation and Its Application in EthiopiaDocumento61 pagineCompensation and Its Application in EthiopiaAlemseged Sisai100% (2)

- Goodyear Philippines Inc. vs. AngusDocumento1 paginaGoodyear Philippines Inc. vs. AngusAnn MarieNessuna valutazione finora

- Group Exercises IFRS For SMEs - 2012Documento14 pagineGroup Exercises IFRS For SMEs - 2012lorenbeatulalianNessuna valutazione finora

- Financing Social Protection: SwedenDocumento28 pagineFinancing Social Protection: SwedenSorina LeagunNessuna valutazione finora

- Dokument BiHDocumento204 pagineDokument BiHccuccaNessuna valutazione finora

- Caterino v. Barry, 1st Cir. (1993)Documento37 pagineCaterino v. Barry, 1st Cir. (1993)Scribd Government DocsNessuna valutazione finora

- Maven Minds Budget Brief 2022Documento24 pagineMaven Minds Budget Brief 2022Salman AhmedNessuna valutazione finora

- FAR - Post-Employement Employee BenefitsDocumento5 pagineFAR - Post-Employement Employee BenefitsJohn Mahatma Agripa100% (1)

- Printable Social Security Disability ApplicationDocumento7 paginePrintable Social Security Disability ApplicationDom Hilliard50% (2)

- 3 Ethics and Social Responsibility For An EntrepreneurDocumento2 pagine3 Ethics and Social Responsibility For An EntrepreneurZia Zobel100% (1)

- (Namfisa Act) Namibia Financial Institutions Supervisory Authority Act 3 of 2001Documento16 pagine(Namfisa Act) Namibia Financial Institutions Supervisory Authority Act 3 of 2001André Le RouxNessuna valutazione finora

- PAL Vs HassaramDocumento10 paginePAL Vs HassaramCherry BepitelNessuna valutazione finora

- CFA Level 1 (Book-B)Documento170 pagineCFA Level 1 (Book-B)butabutt100% (1)

- Unit-8: Indirect Compensation: Employee Benefits PlansDocumento45 pagineUnit-8: Indirect Compensation: Employee Benefits PlansHuma SikandarNessuna valutazione finora