Potrebbero piacerti anche

- Jibo Question BankDocumento43 pagineJibo Question Bankjyottsna27% (15)

- Banking and SPCL Divina NotesDocumento27 pagineBanking and SPCL Divina NotesPrincess Janine SyNessuna valutazione finora

- CHAPTER 13 Solved Problems PDFDocumento8 pagineCHAPTER 13 Solved Problems PDF7100507100% (2)

- GM CropsDocumento17 pagineGM CropsShankho BaghNessuna valutazione finora

- Ans Quiz 1Documento13 pagineAns Quiz 1Jazzy Mercado100% (2)

- Hybrid Rice Breeding & Seed ProductionDocumento41 pagineHybrid Rice Breeding & Seed ProductionAsep Anti-mageNessuna valutazione finora

- Housing Finance: (Home Loan Schemes)Documento41 pagineHousing Finance: (Home Loan Schemes)Shriram LeleNessuna valutazione finora

- Pesticide CalculationDocumento24 paginePesticide CalculationJonas BalahadiaNessuna valutazione finora

- Overview of Agricultural MarketingDocumento61 pagineOverview of Agricultural MarketingGedionNessuna valutazione finora

- Agricultural Sciences Mushroom Cultivation (AGA - 453) B.Sc. (Hons.), B.Sc. Integrated MBADocumento5 pagineAgricultural Sciences Mushroom Cultivation (AGA - 453) B.Sc. (Hons.), B.Sc. Integrated MBAMahendra paudel PaudelNessuna valutazione finora

- SEED Study Materiyal-1Documento24 pagineSEED Study Materiyal-1Sridhar Sridhar100% (1)

- Presentation 1Documento20 paginePresentation 1yogitNessuna valutazione finora

- Negative Impacts of Green RevolutionDocumento2 pagineNegative Impacts of Green RevolutionFelix SimsungNessuna valutazione finora

- Best Out of Waste Competition 2021.1629524991Documento1 paginaBest Out of Waste Competition 2021.1629524991Wolf BHÃĪNessuna valutazione finora

- Guidelines For Data Record (Wheat)Documento2 pagineGuidelines For Data Record (Wheat)Muhammad Boota SarwarNessuna valutazione finora

- Effect of Seed Storage Period in Ambient Condition On Seed Quality of Common Bean (Phaseolus Vulgaris L.) Varieties at Haramaya, Eastern EthiopiaDocumento9 pagineEffect of Seed Storage Period in Ambient Condition On Seed Quality of Common Bean (Phaseolus Vulgaris L.) Varieties at Haramaya, Eastern EthiopiaPremier PublishersNessuna valutazione finora

- Assignment On: Cultivation Practices of BajraDocumento26 pagineAssignment On: Cultivation Practices of BajraAbhishek kumarNessuna valutazione finora

- Genetic Improvement of MushroomsDocumento17 pagineGenetic Improvement of MushroomsMeenuNessuna valutazione finora

- Management of Viral Diseases in ChillisDocumento16 pagineManagement of Viral Diseases in ChillisBalaraju DesuNessuna valutazione finora

- Extension NotesDocumento12 pagineExtension Notesfruitfulluft100% (2)

- Cropping System and Patterns PDFDocumento171 pagineCropping System and Patterns PDF..Nessuna valutazione finora

- Problems of Agricultural Marketing in IndiaDocumento5 pagineProblems of Agricultural Marketing in IndiaHariraj SNessuna valutazione finora

- Agriculture PDF Download 92 - Compressed 1Documento9 pagineAgriculture PDF Download 92 - Compressed 1Sachin KumarNessuna valutazione finora

- Constraints in Agricultural MarketingDocumento36 pagineConstraints in Agricultural MarketingKIRUTHIKANessuna valutazione finora

- ALL 17 LECTURES Weed MNGT NotesDocumento121 pagineALL 17 LECTURES Weed MNGT Notesshubham100% (1)

- TSEGA ThesisDocumento61 pagineTSEGA ThesisAboma MekonnenNessuna valutazione finora

- Tools For Hybrid Seed Production (RS)Documento3 pagineTools For Hybrid Seed Production (RS)yudhvir100% (1)

- Integrated Farming System PrinciplesDocumento7 pagineIntegrated Farming System PrinciplessaumikdebNessuna valutazione finora

- HORT 111 Fundamentals of Horticulture Credit Hours: 2 (1+1)Documento13 pagineHORT 111 Fundamentals of Horticulture Credit Hours: 2 (1+1)AnuragNessuna valutazione finora

- Problematic Soils PDFDocumento84 pagineProblematic Soils PDFRY4NNessuna valutazione finora

- Pest and Diseases of CacaoDocumento39 paginePest and Diseases of CacaoVimarce CuliNessuna valutazione finora

- Board Review For AgricultureDocumento123 pagineBoard Review For Agriculturejonnadz100% (6)

- SugarcaneDocumento12 pagineSugarcaneGanpat Lal SharmaNessuna valutazione finora

- Farming Systems and LIvelihoods Analysis ModuleDocumento71 pagineFarming Systems and LIvelihoods Analysis ModuleRedi Sirbaro100% (1)

- 3.0 Market Analysis, Marketing Channels, Marketing Costs and Margins Market IntermediariesDocumento25 pagine3.0 Market Analysis, Marketing Channels, Marketing Costs and Margins Market IntermediariesOliver TalipNessuna valutazione finora

- Agronomy of Seed Production and Agroclimatic ZonesDocumento46 pagineAgronomy of Seed Production and Agroclimatic ZonesnabiNessuna valutazione finora

- AgricultureDocumento15 pagineAgriculturehafiz ghulam shabirNessuna valutazione finora

- Farming System Lecture NotesDocumento51 pagineFarming System Lecture Noteskamalie122Nessuna valutazione finora

- Farming System Note Final 31 Aug 018Documento88 pagineFarming System Note Final 31 Aug 018Dikshya NiraulaNessuna valutazione finora

- ECON-242 16 JuneDocumento2 pagineECON-242 16 Junevaibhav1004Nessuna valutazione finora

- Biotechnology / Molecular Techniques in Seed Health ManagementDocumento6 pagineBiotechnology / Molecular Techniques in Seed Health ManagementMadhwendra pathak100% (1)

- Plant Disease DiagnosisDocumento16 paginePlant Disease DiagnosisVictor Garcia Jimenez100% (1)

- Maharashtra Krishi Paryatan Vistar Yojana 2012Documento11 pagineMaharashtra Krishi Paryatan Vistar Yojana 2012Chetan V Baraskar100% (1)

- Double Production in Groundnut With Phosphatic BiofertilizersDocumento7 pagineDouble Production in Groundnut With Phosphatic BiofertilizersIJRASETPublicationsNessuna valutazione finora

- Crop MorphologyDocumento108 pagineCrop MorphologyRyan Calderon0% (1)

- Vegetable Based Cropping SystemDocumento4 pagineVegetable Based Cropping SystemRubi100% (1)

- Farm Management Chap 3Documento62 pagineFarm Management Chap 3gedisha katolaNessuna valutazione finora

- Hybrid Rice Breeding ManualDocumento194 pagineHybrid Rice Breeding ManualrafiqqaisNessuna valutazione finora

- Cultural and Mechanical Method PDFDocumento4 pagineCultural and Mechanical Method PDFDr Vijay LaxmiNessuna valutazione finora

- Biological Aspects of Post Harvest Handling: Joel Solomo BalindanDocumento96 pagineBiological Aspects of Post Harvest Handling: Joel Solomo BalindanPETER PAUL ESTILLERNessuna valutazione finora

- Maturity Indices IDocumento37 pagineMaturity Indices IHebilstone SyniaNessuna valutazione finora

- CHapter 3 Marketing of Agricultural CommoditiesDocumento28 pagineCHapter 3 Marketing of Agricultural CommoditiesEliyas Ebrahim Aman100% (1)

- Agricultural MarketingDocumento65 pagineAgricultural MarketingMyx Magullado100% (1)

- Development of A Value Added Amla ProductDocumento4 pagineDevelopment of A Value Added Amla Productscience worldNessuna valutazione finora

- Economics and Agricultural EconomicsDocumento28 pagineEconomics and Agricultural EconomicsM Hossain AliNessuna valutazione finora

- Aext191 PDFDocumento74 pagineAext191 PDFNIDHINessuna valutazione finora

- EXTN-123 Practical Manual (Agri)Documento57 pagineEXTN-123 Practical Manual (Agri)Aniket Sawant OfficialNessuna valutazione finora

- Practical Manual ON: Agronomy of Major Cereal and Pulses AGRO-5217Documento26 paginePractical Manual ON: Agronomy of Major Cereal and Pulses AGRO-5217Tejindarjit Kaur Gill Bahga100% (2)

- Theories of Demand For MoneyDocumento15 pagineTheories of Demand For MoneykamilbismaNessuna valutazione finora

- Presentation On Plant LayoutDocumento20 paginePresentation On Plant LayoutSahil NayyarNessuna valutazione finora

- Disadvantages of Tissue CultureDocumento1 paginaDisadvantages of Tissue CultureDante SallicopNessuna valutazione finora

- Production Technology of RiceDocumento3 pagineProduction Technology of RicebutterfilyNessuna valutazione finora

- Loans & Advances: Procedure & Sanction of LoanDocumento23 pagineLoans & Advances: Procedure & Sanction of LoanPallavi SinghNessuna valutazione finora

- Chapter 3 (Lending)Documento13 pagineChapter 3 (Lending)Mohammad Minhaz Hossain RiyadNessuna valutazione finora

- World's Most Exemplary Women Leaders in Business, 2023 by Worlds LeadersDocumento60 pagineWorld's Most Exemplary Women Leaders in Business, 2023 by Worlds LeadersWorlds Leaders MagazineNessuna valutazione finora

- PassbookstmtDocumento3 paginePassbookstmtDebabrata GhoshNessuna valutazione finora

- AmBank - Card ApplicationDocumento15 pagineAmBank - Card ApplicationOre MacheNessuna valutazione finora

- Trust Bank LTD Internship ReportDocumento47 pagineTrust Bank LTD Internship ReportMd Manajer RoshidNessuna valutazione finora

- Finmgt3 Syllabus 17 18Documento11 pagineFinmgt3 Syllabus 17 18Wilson0% (1)

- BSP Circular 1132, Series of 2021Documento7 pagineBSP Circular 1132, Series of 2021JSTNessuna valutazione finora

- Release #2 UPDATED 29/3/2020 FAQ - Additional Measures To Assist Borrowers/Customers Affected by The COVID-19 OutbreakDocumento6 pagineRelease #2 UPDATED 29/3/2020 FAQ - Additional Measures To Assist Borrowers/Customers Affected by The COVID-19 OutbreakCheah Eu LeeNessuna valutazione finora

- Introduction To Financial Management 2Documento11 pagineIntroduction To Financial Management 2Jiro SukehiroNessuna valutazione finora

- Export Packing CreditDocumento3 pagineExport Packing CreditshashidharrajuNessuna valutazione finora

- European Leveraged Finance Funding Structures Transformed September 2014Documento30 pagineEuropean Leveraged Finance Funding Structures Transformed September 2014bharathaNessuna valutazione finora

- Company TEEDocumento11 pagineCompany TEEJahnaviSinghNessuna valutazione finora

- Ortega v. CACH, LLCDocumento14 pagineOrtega v. CACH, LLCKenneth SandersNessuna valutazione finora

- Basel Committee On Banking Supervision: SCO Scope and DefinitionsDocumento10 pagineBasel Committee On Banking Supervision: SCO Scope and Definitionssh_chandraNessuna valutazione finora

- Agriculture Term Loan - 795/860/891: NF-546 NF-983Documento3 pagineAgriculture Term Loan - 795/860/891: NF-546 NF-983Santosh KumarNessuna valutazione finora

- 1.1 Historical BackgroundDocumento14 pagine1.1 Historical BackgroundAnik AlamNessuna valutazione finora

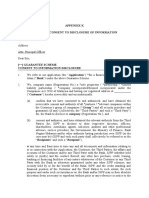

- Letter of Consent To Disclosure of Information 1Documento3 pagineLetter of Consent To Disclosure of Information 1Hazwani IsmailNessuna valutazione finora

- University of Rizal System: Unit I - Central Bank and Its Functions and Operations Module 1-Philippine Financial SystemDocumento22 pagineUniversity of Rizal System: Unit I - Central Bank and Its Functions and Operations Module 1-Philippine Financial SystemFitz Clark LobarbioNessuna valutazione finora

- Ratio Problems 2Documento7 pagineRatio Problems 2Vivek Mathi100% (1)

- Statutory Audit of Bank Branches (Certain Aspects)Documento43 pagineStatutory Audit of Bank Branches (Certain Aspects)Nivedita SharmaNessuna valutazione finora

- Remitance Sonali BankDocumento100 pagineRemitance Sonali BankGolpo Mahmud0% (2)

- Mini Project 2 Report Mba 2nd Semester 2Documento51 pagineMini Project 2 Report Mba 2nd Semester 2Saurav KumarNessuna valutazione finora

- 7 8 BuenaventuraDocumento4 pagine7 8 BuenaventuraAnonnNessuna valutazione finora

- How To Credit Score With Predictive Analytics: WhitepaperDocumento7 pagineHow To Credit Score With Predictive Analytics: WhitepapernguyenhaquanNessuna valutazione finora

- Application FormDocumento8 pagineApplication FormManoj KumarNessuna valutazione finora

- Credit Scoring For Microfinance Using Behavioral Data in Emerging MarketsDocumento25 pagineCredit Scoring For Microfinance Using Behavioral Data in Emerging MarketsCésar Anderson HNNessuna valutazione finora

- Co-Lending Policy Dated 04022021Documento11 pagineCo-Lending Policy Dated 04022021patruni sureshkumarNessuna valutazione finora