Potrebbero piacerti anche

- Closing EntriesDocumento14 pagineClosing EntriesAlbert Moreno100% (1)

- The Circular Flow of Economic Activity (Autosaved)Documento19 pagineThe Circular Flow of Economic Activity (Autosaved)LittleagleNessuna valutazione finora

- Castro Company ZABALLADocumento11 pagineCastro Company ZABALLAHelping Five (H5)Nessuna valutazione finora

- Lesson5-Bsa 2BDocumento8 pagineLesson5-Bsa 2BEdraelyn MonatoNessuna valutazione finora

- Assignment 3Documento8 pagineAssignment 3jhouvanNessuna valutazione finora

- General Instructions: Prepare The Journal and Adjusting Entries) OF ABC ELECTRONIC REPAIR SERVICES FOR THE Month of December 2019Documento3 pagineGeneral Instructions: Prepare The Journal and Adjusting Entries) OF ABC ELECTRONIC REPAIR SERVICES FOR THE Month of December 2019Daniella Mae ElipNessuna valutazione finora

- Financing Takeovers & External Forces Affecting GovernanceDocumento2 pagineFinancing Takeovers & External Forces Affecting GovernanceLeoson0% (1)

- Far Prelims Week 1Documento3 pagineFar Prelims Week 1hat dawgNessuna valutazione finora

- Quiz 2 Cost AccountingDocumento1 paginaQuiz 2 Cost AccountingRocel DomingoNessuna valutazione finora

- Welfare and Justice For All - Economic LifeDocumento10 pagineWelfare and Justice For All - Economic LifeLeeNessuna valutazione finora

- Final Assignment No 3 Acctg 121Documento4 pagineFinal Assignment No 3 Acctg 121Pler WiezNessuna valutazione finora

- Valuation of Contributions of PartnersDocumento3 pagineValuation of Contributions of Partnersfinn mertensNessuna valutazione finora

- Microeconomics Spoken PoetryDocumento2 pagineMicroeconomics Spoken PoetryChris AnnNessuna valutazione finora

- Advantage and Disadvantages of Business OrganizationDocumento3 pagineAdvantage and Disadvantages of Business OrganizationJustine VeralloNessuna valutazione finora

- Tempest Marketing Statement of Financial PositionDocumento8 pagineTempest Marketing Statement of Financial PositionJay Mark Marcial JosolNessuna valutazione finora

- Account Titles and Its ElementsDocumento3 pagineAccount Titles and Its ElementsJeb PampliegaNessuna valutazione finora

- Books of Accounts & Double-Entry SystemDocumento16 pagineBooks of Accounts & Double-Entry SystemBLANKNessuna valutazione finora

- Account TitlesDocumento4 pagineAccount TitlesErin Jane FerreriaNessuna valutazione finora

- Getalado, Jericho M.Documento18 pagineGetalado, Jericho M.Ruth Getalado0% (1)

- Leila Durkin An Architect Opened An Office On May 1Documento1 paginaLeila Durkin An Architect Opened An Office On May 1M Bilal SaleemNessuna valutazione finora

- Castro-Merchandising 20211124 0001Documento2 pagineCastro-Merchandising 20211124 0001Chelsea TengcoNessuna valutazione finora

- Liabilities Amount CalculationDocumento6 pagineLiabilities Amount CalculationRoel Cababao50% (2)

- Managerial Costs KeyDocumento7 pagineManagerial Costs KeyJane VillanuevaNessuna valutazione finora

- Managerial Economics ReviewerDocumento6 pagineManagerial Economics Reviewermary grace cornelioNessuna valutazione finora

- 03 Quiz 1 AubDocumento3 pagine03 Quiz 1 Aubken dahunanNessuna valutazione finora

- SAP B1 Fundamentals AccountingDocumento33 pagineSAP B1 Fundamentals AccountingJosef SamoranosNessuna valutazione finora

- Managerial Economics ReviewerDocumento26 pagineManagerial Economics ReviewerAlyssa Faith NiangarNessuna valutazione finora

- Resultay T-AccountsDocumento1 paginaResultay T-AccountsMackenzie Heart ObienNessuna valutazione finora

- Notes in Business Law by Fidelito Soriano PDF 16Documento2 pagineNotes in Business Law by Fidelito Soriano PDF 16Getty Reagan Dy0% (2)

- FUNDACC1 - Reviewer (Theories)Documento12 pagineFUNDACC1 - Reviewer (Theories)MelvsNessuna valutazione finora

- Accounting for Merchandising Businesses Inventory SystemsDocumento15 pagineAccounting for Merchandising Businesses Inventory SystemsAple Balisi100% (1)

- FAR Chapter 1 Problem 2Documento1 paginaFAR Chapter 1 Problem 2jelou ubagNessuna valutazione finora

- Quiz on Powers of a CorporationDocumento3 pagineQuiz on Powers of a CorporationJanrey RomanNessuna valutazione finora

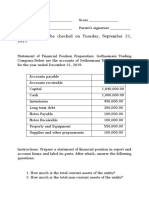

- Answer This To Be Checked On Tuesday, September 21, 2021Documento2 pagineAnswer This To Be Checked On Tuesday, September 21, 2021Teresa Mae OrquiaNessuna valutazione finora

- Common practice in Philippines financial reportingDocumento2 pagineCommon practice in Philippines financial reportingKaren CaelNessuna valutazione finora

- Module For ACC 206 Understanding ExpensesDocumento12 pagineModule For ACC 206 Understanding ExpensesMerecci Angela De ChavezNessuna valutazione finora

- Accounting For Partnership and CorporationDocumento19 pagineAccounting For Partnership and CorporationJoelyn Grace MontajesNessuna valutazione finora

- Adjusting Entry - PrepaymentsDocumento19 pagineAdjusting Entry - PrepaymentsShayne Aldrae CacaldaNessuna valutazione finora

- Salvacion CapistranoDocumento14 pagineSalvacion CapistranoHazel Ann DuermeNessuna valutazione finora

- GUINTO - Activity 1 - Loans and Impairment ReceivableDocumento4 pagineGUINTO - Activity 1 - Loans and Impairment ReceivableGUINTO, DAN FRANCIS B.Nessuna valutazione finora

- Cindy Lota - Activity No. 3 - Statement of Financial PositionDocumento6 pagineCindy Lota - Activity No. 3 - Statement of Financial PositionCindy LotaNessuna valutazione finora

- Bart MDocumento3 pagineBart MSteph Borinaga0% (1)

- CF04 Part 3 - Petty Cash FundDocumento51 pagineCF04 Part 3 - Petty Cash FundABMAYALADANO ,ErvinNessuna valutazione finora

- College of Management: Capiz State UniversityDocumento4 pagineCollege of Management: Capiz State UniversityDave IsoyNessuna valutazione finora

- Pleting The Accounting CycleDocumento65 paginePleting The Accounting Cycleyow jing peiNessuna valutazione finora

- Financial Records of a Law PartnershipDocumento78 pagineFinancial Records of a Law PartnershipAndrea Beverly TanNessuna valutazione finora

- Merchandising CompaniesDocumento8 pagineMerchandising Companiesmagdy kamelNessuna valutazione finora

- Quiz SolutionDocumento3 pagineQuiz SolutionKim Patrick VictoriaNessuna valutazione finora

- Managerial Economics in The 21st CenturyDocumento14 pagineManagerial Economics in The 21st CenturyMaevel CantigaNessuna valutazione finora

- Short Case ActivitiesDocumento2 pagineShort Case ActivitiesRaff LesiaaNessuna valutazione finora

- Bam 040 Sas Period 1Documento57 pagineBam 040 Sas Period 1Lily KyuNessuna valutazione finora

- Income and Tax Calculation for Individuals, Corporations and Business EntitiesDocumento24 pagineIncome and Tax Calculation for Individuals, Corporations and Business EntitiesCharity Lumactod AlangcasNessuna valutazione finora

- 3 Great Greek Triumvirate in PhilosophyDocumento23 pagine3 Great Greek Triumvirate in PhilosophyPrecious CativoNessuna valutazione finora

- The CaseDocumento7 pagineThe CaseJeth J LungayNessuna valutazione finora

- 5th Activity Reyes Laundry ShopDocumento17 pagine5th Activity Reyes Laundry Shoprain suansing100% (1)

- 00 CookingDocumento7 pagine00 CookingEllaquer EvardoneNessuna valutazione finora

- Problem 12 Accounting PDFDocumento3 pagineProblem 12 Accounting PDFErika RepedroNessuna valutazione finora

- Accounting Problem 16Documento1 paginaAccounting Problem 16sabbyveraNessuna valutazione finora

- Assignment 1.7Documento5 pagineAssignment 1.7AIRA BERMIDONessuna valutazione finora

- Koster Keunen Beekeeping Webinar PresentationDocumento15 pagineKoster Keunen Beekeeping Webinar PresentationKOUASSI SylvainNessuna valutazione finora

- 2008business HorizonsDocumento10 pagine2008business HorizonsNishtha KaushikNessuna valutazione finora

- Chapter 2 Macro SolutionDocumento12 pagineChapter 2 Macro Solutionsaurabhsaurs100% (1)

- Micro EconomicsDocumento42 pagineMicro EconomicsSomeone100% (1)

- The Common Forms of Debt Restructuring: Asset SwapDocumento5 pagineThe Common Forms of Debt Restructuring: Asset SwapJonathan VidarNessuna valutazione finora

- Anheuser Busch and Harbin Brewery Group of ChinaDocumento17 pagineAnheuser Busch and Harbin Brewery Group of Chinapooja87Nessuna valutazione finora

- Hutchison Whampoa Capital Structure DecisionDocumento11 pagineHutchison Whampoa Capital Structure DecisionUtsav DubeyNessuna valutazione finora

- HSBC Who Is The BossDocumento7 pagineHSBC Who Is The BossT FaizNessuna valutazione finora

- Financial Accounting and Reporting EllioDocumento181 pagineFinancial Accounting and Reporting EllioThủy Thiều Thị HồngNessuna valutazione finora

- Kebede Kassa First Draft CommentedDocumento73 pagineKebede Kassa First Draft CommentedBereketNessuna valutazione finora

- Group 2 Housing Development and ManagementDocumento29 pagineGroup 2 Housing Development and ManagementTumwesigye AllanNessuna valutazione finora

- Business EnterpriseDocumento4 pagineBusiness EnterpriseJhon JhonNessuna valutazione finora

- ACTBAS1 - Lesson 2 (Statement of Financial Position)Documento47 pagineACTBAS1 - Lesson 2 (Statement of Financial Position)AyniNuydaNessuna valutazione finora

- Mobile Services: Your Account Summary This Month'S ChargesDocumento8 pagineMobile Services: Your Account Summary This Month'S ChargesVenkatram PailaNessuna valutazione finora

- ENGINEERING DESIGN GUILDLINES Plant Cost Estimating Rev1.2webDocumento23 pagineENGINEERING DESIGN GUILDLINES Plant Cost Estimating Rev1.2webfoxmancementNessuna valutazione finora

- BBMF2023Documento7 pagineBBMF2023Yi Lin ChiamNessuna valutazione finora

- KOICA Annual Report 2017Documento63 pagineKOICA Annual Report 2017hoang khieuNessuna valutazione finora

- Assessment of Cash Management in NIBDocumento48 pagineAssessment of Cash Management in NIBEfrem Wondale100% (1)

- Question P8-1A: Cafu SADocumento29 pagineQuestion P8-1A: Cafu SAMashari Saputra100% (1)

- Efficient solid waste management in TelanganaDocumento5 pagineEfficient solid waste management in TelanganaManvika UdiNessuna valutazione finora

- Full Cost Accounting: Dela Cruz, Roma Elaine Aguila, Jean Ira Bucad, RoceloDocumento72 pagineFull Cost Accounting: Dela Cruz, Roma Elaine Aguila, Jean Ira Bucad, RoceloJean Ira Gasgonia Aguila100% (1)

- Accounting Textbook Solutions - 68Documento19 pagineAccounting Textbook Solutions - 68acc-expertNessuna valutazione finora

- Week 7 Class Exercises (Answers)Documento4 pagineWeek 7 Class Exercises (Answers)Chinhoong OngNessuna valutazione finora

- Improve Your Business Handbook 1986Documento136 pagineImprove Your Business Handbook 1986ZerotheoryNessuna valutazione finora

- Osabadell: Deposits in Your AccountsDocumento7 pagineOsabadell: Deposits in Your Accounts张灿Nessuna valutazione finora

- Reverse LogisticDocumento8 pagineReverse LogisticĐức Tiến LêNessuna valutazione finora

- Saudi Arabia Report 2018 PDFDocumento9 pagineSaudi Arabia Report 2018 PDFSandy SiregarNessuna valutazione finora

- Tugas Problem Set 2Documento3 pagineTugas Problem Set 2Nur Rahmi PitaNessuna valutazione finora

- Pritesh S Pingale Bank StatementDocumento8 paginePritesh S Pingale Bank StatementDnyaneshwar WaghmareNessuna valutazione finora

- 1550588772875-Harsha InternshipDocumento19 pagine1550588772875-Harsha InternshipRuchika JainNessuna valutazione finora